EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

Used with care, the Roth IRA may help serve several objectives at once — like a multipurpose tool in your financial-planning toolbox.

Retirement

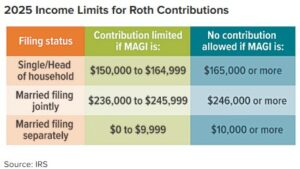

First and foremost, a Roth IRA is designed to provide tax-free income in retirement. If your modified adjusted gross income (MAGI) falls within certain limits, you can contribute up to $7,000 ($8,000 for those age 50 or older) in earned income to a Roth IRA in 2024 and 2025. Although Roth IRA contributions are not tax-deductible, qualified withdrawals are tax-free. A qualified withdrawal is one made after the account has been held for at least five years and the account owner reaches age 59½, becomes disabled, or dies. Nonqualified withdrawals of earnings are subject to ordinary income taxes and a 10% penalty, unless an exception applies.

Emergency savings

Because contributions to a Roth IRA are made on an after-tax basis, they can be withdrawn at any time — which means, in a money crunch, you could withdraw just your Roth contributions (not the earnings) free of taxes and penalties. In addition, account holders may withdraw up to $1,000 in earnings each year to cover emergency expenses.1

Teachable moments

A Roth IRA can also be an ideal way to introduce a working teen to long-term investing. Minors can contribute to a Roth IRA as long as they have earned income and a parent or other adult opens a custodial account in their name. Alternatively, an adult can contribute to a Roth IRA within a custodial account on a child’s behalf, as long as the total amount doesn’t exceed the child’s total wages for the year.

College and first home

Roth IRA earnings can be withdrawn penalty-free to provide funds for college and the purchase of a first home.

College. Roth IRA funds can help pay for certain undergraduate and graduate costs for yourself or a qualified family member. Expenses include tuition, housing and food (if the student attends at least half time), fees, books, supplies, and required equipment not covered by other tax-free sources, such as scholarships or employer education benefits. An advantage of using a Roth IRA to help pay for college is that assets held in retirement accounts are excluded from the government’s financial-aid formula. (A related point: up to $35,000 in 529 plan assets that are not used to pay for college may be rolled over to a Roth IRA for the same beneficiary, provided certain rules are followed.)

First home purchase. Up to $10,000 (lifetime limit) can be used for qualified expenses associated with a first-time home purchase. You are considered a first-time home buyer if you haven’t owned or had interest in a home during the previous two years. Funds may be used for acquisition, construction, or reconstruction of a principal residence and must be used within 120 days of the distribution. If the account has been held for at least five years, the distribution will be income tax-free as well.

Estate planning

Roth IRAs are not subject to the age-based required minimum distribution rules that apply to non-Roth retirement accounts during your lifetime. For this reason, if you don’t need your Roth IRA funds, they can continue to accumulate. After your death, the tax-free income benefit continues to apply to your beneficiaries (however, the value of your Roth IRA will be assessed for federal and possibly state estate tax purposes).

Proceed with caution

Although it’s generally best to avoid tapping money earmarked for retirement early, the Roth IRA can help serve multiple needs — if used wisely.

The tax implications of a 529 savings plan should be discussed with your legal and/or tax professional because they can vary from state to state. Also be aware that most states offer their own 529 plans, which may provide advantages and benefits exclusively for their residents and taxpayers. These other state benefits may include financial aid, scholarship funds, and protection from creditors. Before investing in a 529 savings plan, please consider the investment objectives, risks, charges, and expenses carefully. The official disclosure statements and applicable prospectuses, which contain this and other information about the investment options, underlying investments, and investment company, can be obtained by contacting your financial professional. You should read these materials carefully before investing.

1) Due to ordering rules, Roth IRA contributions will always be distributed before earnings.