EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

529 plans were created in 1996 to give families a tax-advantaged way to save for college. Roth IRAs were created a year later to give people another tax-advantaged way to save for retirement. Along the way, some parents began using Roth IRAs as a college savings tool. And now, starting in 2024, extra funds in a 529 plan can be rolled over to a Roth IRA for the same beneficiary. Here’s how the two options compare in a few key areas.

Contribution rules

529 plan: Anyone can open a 529 account. In 2024, individuals can contribute up to $18,000 ($36,000 for married couples) without triggering gift tax implications. And under a special accelerated gifting rule unique to 529 plans, individuals can make a lump sum contribution in 2024 up to $90,000 ($180,000 for married couples) with no gift tax implications if they elect to spread the gift over five years. Lifetime contribution limits for 529 plans are high — most plans have lifetime limits of $350,000 and up (limits vary by state).

Roth IRA: Not everyone can contribute to a Roth IRA. In 2024, single filers must have a modified adjusted gross income (MAGI) of $146,000 or less and joint filers must have a MAGI of $230,000 or less. (A partial contribution is allowed for single filers with a MAGI between $146,000 and $161,000, and joint filers with a MAGI between $230,000 and $240,000.) In 2024, the annual contribution limit is $7,000 ($8,000 for people age 50 and older).

Tax benefits

529 plan: Earnings in a 529 account accumulate tax-deferred and are tax-free when withdrawn if funds are used to pay the beneficiary’s qualified education expenses, a broad term that includes tuition, fees, housing, food, and books. States generally follow this tax treatment, and some states may offer a tax deduction for 529 contributions. If funds in a 529 account are used for a non-qualified expense, the earnings portion of the withdrawal is subject to income tax and a 10% federal penalty.

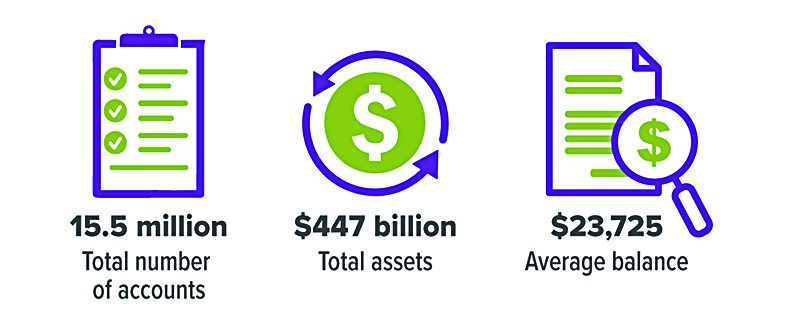

529 Plan Snapshot (2023)

Source: ISS Market Intelligence, 529 Market Highlights Q4 2023

Roth IRA: Earnings in a Roth IRA also accumulate tax-deferred and are tax-free if a distribution is qualified. A distribution is qualified if a five-year holding period is met and the distribution is made: (1) after age 59½, (2) due to a qualifying disability, (3) to pay certain first-time home buyer expenses, or (4) to your beneficiary after your death. If your distribution isn’t qualified, the earnings portion of the withdrawal is subject to income tax and, if you’re younger than 59½, a 10% early withdrawal penalty (unless an exception applies). One exception to this penalty is when the withdrawal is used to pay college expenses.

So, your age is key. Once you’ve met both the age 59½ and five-year holding requirements, money withdrawn from your Roth IRA to pay college expenses is tax-free. But even though withdrawing funds before age 59½ for college expenses won’t trigger an early withdrawal penalty, you may owe income tax on the earnings. (Nonqualified distributions draw out contributions first and earnings last, so you could withdraw up to the amount of your contributions and not owe income tax.)

Investment options and flexibility

529 plan: You’re limited to the investment options offered by the 529 plan. Plans typically offer a range of static and age-based portfolios (where the underlying investments automatically become more conservative as the beneficiary gets closer to college) with varying levels of risk, fees, and management goals. If you’re unhappy with the investment performance of the options you’ve chosen, you can change the investment options on your current contributions only twice per year, per federal law.

Roth IRA: With a Roth IRA, you generally can choose from a wide range of investments, and you can typically buy and sell investments whenever you like (usually incurring transaction costs and fees), so they offer a lot of flexibility.

There are generally fees and expenses associated with investing in a 529 plan, as well as the risk that investments may lose money or not perform well enough to cover college costs as anticipated. The tax implications of a 529 plan can vary from state to state and should be discussed with a legal and/or tax professional. States offering their own 529 plans may provide their residents and taxpayers with exclusive advantages and benefits, which may include financial aid, scholarship funds, and protection from creditors. Before investing in a 529 plan, consider the investment objectives, risks, charges, expenses, investment options, underlying investments, and the investment company, which are available in the official disclosure statement and applicable prospectuses. Contact your financial professional to obtain a copy.