EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

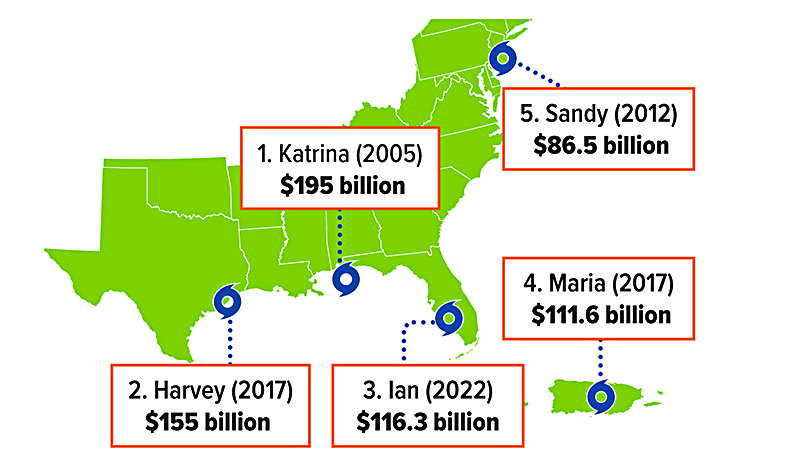

With wildfires in Maui, Hurricane Idalia in Florida, and the heat wave that blanketed the South, Midwest, and Great Plains, 2023 was a record-setting year for extreme weather in the United States. In fact, last year the U.S. saw more weather and climate-related disasters that cost over $1 billion than ever before. 1

As a result of these extreme weather events, many insurance companies have begun to raise rates, restrict coverage, or stop selling policies in high-risk areas. This has left homeowners in a precarious situation when it comes to home insurance, as many are now faced with higher premiums, lower home values, and the possibility of the nonrenewal of their policies.

If you live in an area that is susceptible to extreme weather events, you’ll want to be prepared for the possible disruption of your home insurance coverage. The key is to act quickly so that you can manage your financial risk and help make sure that your home is protected.

Handling a nonrenewal

Depending on the state you live in, if your insurer chooses not to renew your coverage, they generally have 30 to 60 days to send you a notice of nonrenewal. Your first step should be to contact your insurer and ask why your policy wasn’t renewed. They may reverse their decision and renew your policy if the reason for nonrenewal can be fixed, such as by installing a fire alarm system or fortifying a roof.

If that doesn’t work, you should begin shopping for new coverage as soon as possible. Start by contacting your insurance agent or broker or your state’s insurance department to find out which licensed insurance companies are still selling policies in your area. You can also try using the various online comparison tools that will allow you to compare rates and coverage amongst different insurers. Finally, ask for recommendations for insurers from friends, neighbors, and coworkers who live nearby.

Consider high-risk home insurance

If your home is deemed to be at high risk due to its geographic area, you may want to look for an insurance company that specializes in high-risk home insurance.

High-risk policies often have significant exclusions and policy limits and are more expensive than traditional home insurance policies. However, they can provide coverage to a home that might otherwise be uninsurable.

Use a FAIR plan as a last resort

If you have trouble obtaining standard home insurance coverage, you may be eligible to obtain coverage under your state’s Fair Access to Insurance Requirements (FAIR) plan. Many states offer homeowners access to some type of FAIR plan.2

FAIR plans are often referred to as “last resort” plans, since homeowners who obtain insurance through a FAIR plan are usually not eligible for standard home insurance coverage due to their home being located in a high-risk area. Coverage under a FAIR plan is more expensive than standard home insurance and is fairly limited — it usually only provides basic dwelling coverage, although some states may offer other coverage options for things like personal belongings or additional structures. In addition, most states require you to show proof that you have been denied coverage before you can apply for a FAIR plan.

Avoid expensive force-placed insurance

If you have a mortgage, your lender will require your home to be properly insured. If you lose your home insurance coverage or your coverage is deemed insufficient, your lender will purchase home insurance for you and charge you for it. These types of policies are referred to as “force-placed insurance” and are designed to protect lenders, not homeowners. They usually only provide limited coverage, such as coverage for the amount due on the loan or replacement coverage if the structure is lost.

Force-placed insurance policies are typically much more expensive than traditional home insurance, with the premiums being paid upfront by your lender and added on to your monthly mortgage payment. Your lender is required to give you notice before it charges you for force-placed insurance. In addition, you have the right to have the force-placed insurance removed once you obtain proper home insurance coverage on your own.

1) NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters, 2023

2) National Association of Insurance Commissioners, 2023

2) National Association of Insurance Commissioners, 2023

United States infographic map concept with space for your copy.

Source: NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters, 2023