EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

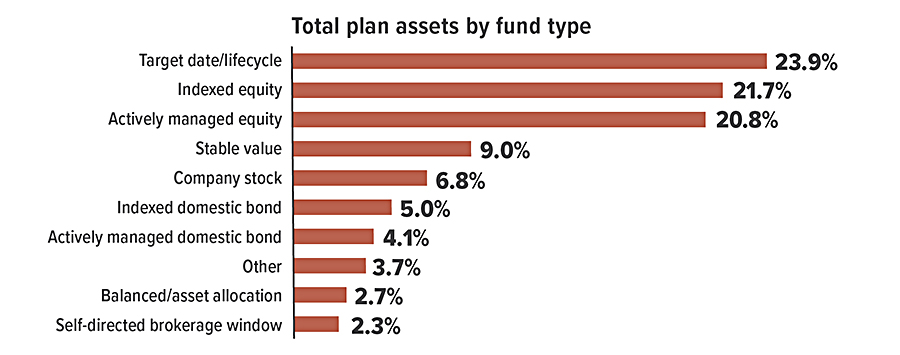

How Are 401(k) Plan Participants Investing Their Money?

Created in 1996, National 401(k) Day has historically been celebrated on the Friday following Labor Day to shine a spotlight on this important employee benefit. Since the late 1990s, plans have evolved substantially, and most participants can now choose from a diverse variety of investments. The chart below shows how 401(k) and profit-sharing funds were invested in 2020.

Source: Plan Sponsor Council of America, 2021

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

Mutual funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

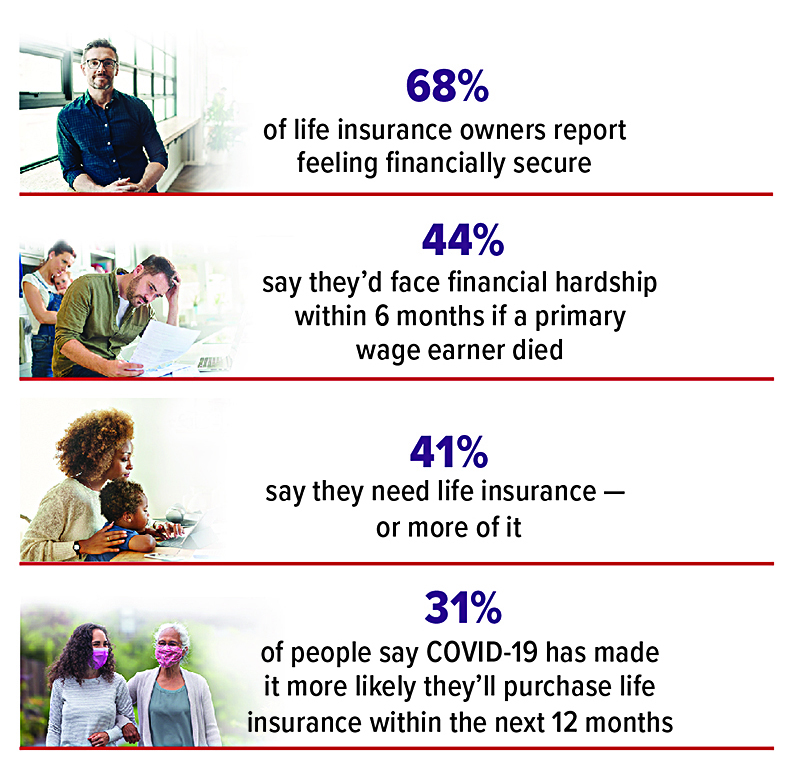

How Much Life Insurance Do You Need?

Throughout your life, your financial needs will change and life insurance can help you meet some of those needs. But how much life insurance do you need? There are a number of approaches to help determine how much life insurance you should have. Here are three of those methods.

Family Needs Approach

With this approach, you divide your family’s financial needs into three main categories:

- Immediate needs at death, such as cash needed for estate taxes and settlement costs, credit-card and other debts including a mortgage (unless you choose to include mortgage payments as part of ongoing family expenses), and an emergency fund for unexpected costs

- Ongoing income needs for expenses such as food, clothing, shelter, and transportation, which will vary in amount and duration, depending on a number of factors, such as your spouse’s age, your children’s ages, your surviving spouse’s income, your debt, and whether you’ll provide funds for your surviving spouse’s retirement

- Special funding needs, such as college, charitable bequests, funding a buy/sell agreement, or business succession planning

Once you determine the total amount of your family’s financial needs, subtract that total from the available assets your family could use to help defray some or all of these expenses. The difference, if any, represents an amount that the life insurance proceeds, and the income from future investment of those proceeds, might cover.

Income Replacement Calculation

This method is based on the premise that family income earners should buy enough life insurance to replace the loss of income due to an untimely death. Under this approach, the amount of life insurance you should consider is based on the value of the income that you can expect to earn during your lifetime, taking into account such factors as inflation and anticipated salary increases, as well as the interest that the lump-sum life insurance proceeds may generate.

Estate Preservation and Liquidity Needs Approach

This method attempts to calculate the amount of life insurance needed to settle your estate. Settlement costs may include estate taxes and funeral, legal, and accounting expenses. The goal is to preserve the value of your estate at the level prior to your death and to avoid an unwanted sale of assets to pay for any of these estate settlement expenses. This approach takes into consideration the amount of life insurance you may want in order to maintain the current value of your estate for your family, while providing the cash needed to cover death expenses and taxes.

Unfortunately, many people underestimate their life insurance needs. Often, the purchase of life insurance is based solely on its cost instead of the benefit it might provide. By the same token, it’s possible to have more life insurance than you need. September is Life Insurance Awareness Month, a good time to review your life insurance to help ensure that it matches your current and projected needs.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. Any guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company. Optional benefits are available for an additional cost and are subject to contractual terms, conditions, and limitations.

Source: 2022 Insurance Barometer Study, Life Happens and LIMRA

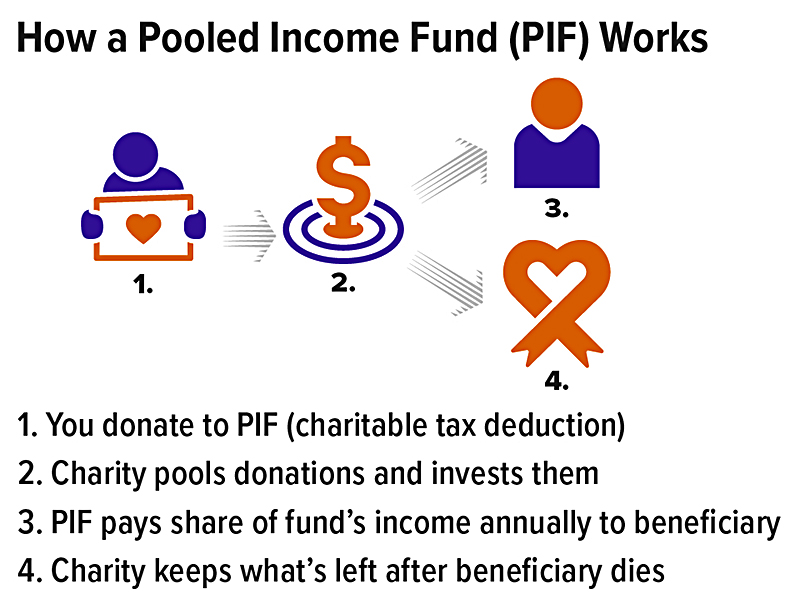

Pooled Income Fund: A Charitable Gift That Provides Income to You

A pooled income fund is a trust with both charitable and noncharitable beneficiaries. It is established and run by a public charity, not by you. The charity “pools” the irrevocable contributions of many people, invests the money, and then distributes to you (or your designated beneficiary) a periodic income payment (usually quarterly or annually) for life, prorated to match your contribution to the fund. When you die or your designated beneficiary dies, your remaining share in the fund passes to the charity.

Charitable Deduction

If you itemize deductions, you receive an immediate federal income tax charitable deduction for the present value of the remainder interest that will pass to charity. Your deduction is limited to 50% or 30% of your adjusted gross income (AGI), depending on the type of property contributed. Amounts disallowed because of the AGI limitations can be carried over for up to five years, subject to the AGI limitations in the carryover years. The transfer of the remainder interest to charity would also qualify for the federal gift tax or estate tax charitable deduction.

The amount of the income tax deduction is generally based on the fair market value of the property contributed to the pooled income fund, the beneficiary or beneficiaries’ age(s), and the fund’s highest rate of return in the last three taxable years.

Noncharitable Income Interest

Trust payments can last for the life or lives of one or more noncharitable beneficiaries. For example, you could name yourself, yourself and your spouse, or even someone else as the noncharitable beneficiary.

If you retain a noncharitable interest, the pooled income fund interest will be included in your gross estate for federal estate tax purposes. If your spouse receives the noncharitable interest as your survivor, that interest should qualify for the estate tax marital deduction (and the balance should qualify for the estate tax charitable deduction).

If you transfer a noncharitable interest to someone else while you are alive, you may have made a gift or generation-skipping transfer (GST) to that person of the income interest. (A GST is a transfer to a person two or more generations younger than you.) A portion of the gift may qualify for the annual gift tax exclusion, but not for the GST tax annual exclusion. A transfer to your spouse would generally qualify for the gift tax marital deduction. You may also have a federal gift and estate tax applicable exclusion amount or a GST tax exemption to shelter any transfer from tax.

Donors generally have limited choices in investment strategy. The amount of income received by the noncharitable beneficiary is not guaranteed; it may increase or decrease depending on the performance of the fund. If the investments in the fund perform poorly and the actual income earned by the fund declines, the charity is prohibited from invading the principal to increase the payment to the noncharitable beneficiary.

Income distributed to the noncharitable beneficiary is usually taxable at ordinary income tax rates. It may also be subject to the 3.8% net investment income tax.

Other Considerations

One of the biggest advantages of choosing a pooled income fund over a charitable remainder unitrust or charitable remainder annuity trust is that you avoid the hassle and cost of establishing your own trust. Another advantage is that if the property you are donating to charity is relatively small, a pooled income fund makes the most of your assets by commingling them with the property of others. The fund can then use the increased assets to diversify among investments, thus helping reduce your investment risk. Also, the large size of the fund (compared to your own charitable trust) may translate into lower operating costs and more experienced management. By contrast, it may not be economically feasible for you to establish a charitable trust with a small investment. Even if you do, it may be impossible for the trustee to spread this money over a variety of investments. (Diversification does not guarantee a profit or protect against investment loss.)

In general, you can donate any type of property to a pooled income fund that the charity is willing to accept. A noncash donation will generally cause the 30% AGI limitation to apply to your charitable deduction. A fund cannot accept or hold tax-exempt securities.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

Building Financial Resilience

Inflation, roller-coaster markets, global events, and life circumstances can test anyone’s fortitude. You may not feel ready to handle these pressure-filled times and might worry about the potential effects on your financial well-being. Fortunately, you can take steps to build the resilience you need to help handle the turbulence and hopefully emerge even stronger.

Focus on the Foundation

Developing a new budget or reviewing an existing one may help reduce stress by reminding you that you still have control over many aspects of your personal finances. A budget outlines your income and expenses and shows how much money is coming in compared to how much money is going out. If you find that you are spending more than you realized, you can make adjustments.

An important companion to a budget is an emergency fund. When an unexpected expense comes up, you can use your emergency reserves to cover it, instead of dipping into long-term savings or racking up costly credit-card debt that could throw your budget off track at a time you can least afford it. Consider starting an emergency fund and build it up over time.

Stress-test Your Portfolio

When you’re investing for retirement or another financial goal, assessing the potential impact of various scenarios may help you prepare for unexpected events. This may be done using computer simulations to analyze how your portfolio might perform. Doing this at regular intervals may help take some of the emotion out of decision-making during stressful times, helping you address gaps and opportunities.

There is no assurance that a simulation will be accurate. Because of the many variables involved, you should not rely on simulations without realizing their limitations. All investing involves risk, and there is no assurance that any financial strategy will be successful.

Prepare for the Future

Of course, you’re never going to be prepared for every financial scenario. But developing a written financial strategy and reviewing it periodically may help you thoughtfully navigate life’s twists and turns. It documents and organizes the pieces of your financial picture, helping you stay focused on the future as you weather the current storms.

Building financial resilience is an ongoing process, and it’s never too late to start. Becoming better positioned for downturns can help you feel more confident that you can handle whatever challenges come your way.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Prepared by Broadridge Advisor Solutions Copyright 2022.