EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

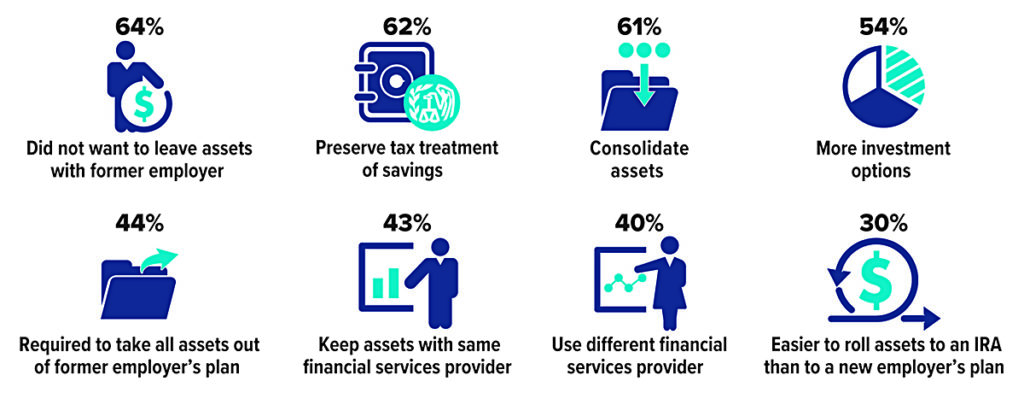

Reasons to Roll

When you leave your job or retire, you have an opportunity to manage your funds in an employer-sponsored retirement plan such as a 401(k), 403(b), or government 457(b) plan. Depending on the situation, you generally have four options.* The approach that typically gives you the most control over the funds is to transfer some or all of the assets to an IRA through a rollover.

Three out of five households who owned traditional IRAs in 2022 had executed at least one IRA rollover from an employer-sponsored retirement plan. These were the top reasons for the most recent rollover.

*Other options may include leaving assets in the former employer’s plan, transferring assets to a new employer-sponsored plan, or withdrawing the money.

Source: Investment Company Institute, 2023 (multiple responses allowed)

Yours, Mine, and Ours: Financial Tips for Blended Families

Combining finances can be complicated for any couple, but the challenges become more complex the second time around, especially when children are involved. Here are some ideas to consider if you are already part of a blended family or looking forward to combining households sometime soon.

Be Clear and Comprehensive

It’s important to reveal all assets, income, and debts, and discuss how these should be treated in your combined family. A prenuptial agreement may seem unromantic, but it could prevent acrimony and misunderstanding if the marriage ends through divorce or the death of a spouse. If you don’t want a legal agreement, have an open and honest discussion, and lay all your cards on the table. It’s not too late to clarify the situation after you’ve tied the knot.

One of the most fundamental issues is where you and your new spouse will live. It might be more convenient — and perhaps better financially — to move into a residence that one of you already owns. But couples in a second marriage often report that moving into a new home gives them a feeling of a fresh start, which could have value that can’t be measured financially.1

Create a blueprint for short-term and long-term finances. Do you plan to combine bank accounts or keep separate accounts, perhaps with a joint account to pay shared expenses? To what accounts will each of your salaries be deposited? Will one spouse help pay off the other spouse’s debts such as student loans, auto loans, and credit cards? Research suggests that remarried couples are generally happier when they pool resources, but there are many variations in how that might be carried out.2

Consider the Kids

Discuss how you plan to handle financial responsibility for children from previous marriages versus any children you have together. Are they going to be “your kids, my kids, and our kids,” or are they all “our kids”? Being a stepparent and/or a divorced parent can be complex emotionally, and there are no easy answers. But there are some not-so-complex financial questions you should address up front.

Be clear about alimony payments, child support, and other financial responsibilities. For example, what is each spouse’s intention and/or legal obligation to pay college tuition costs for children from a previous marriage? Are there assets that one spouse wants to reserve for the benefit of his or her children? Is the other spouse willing to waive rights to those assets?

Communicating and planning with an ex-spouse is essential if you share custody of children. Along with responsibilities for everyday expenses, be sure you understand and agree on other financial issues, such as who will claim the child as a beneficiary on tax returns, and who is the “custodial parent” for purposes of financial aid applications. A beneficiary deduction may be more valuable for a parent with higher earnings, but a custodial parent with lower earnings may enable a student to qualify for more financial aid.

Update Wills and Beneficiary Forms

Be sure that your will and all beneficiary forms reflect your new situation and current wishes. A will can designate heirs and facilitate distribution of assets when an estate goes through the probate process. However, the assets in most pension plans, qualified retirement accounts, and life insurance policies convey directly to the people named on the beneficiary forms — even if they are different from those named in your will — and are not subject to probate. By law, your current spouse is the beneficiary of an ERISA-governed retirement account such as a 401(k) plan. If you want to designate an ex-spouse or children from a previous marriage as account beneficiaries, you must obtain a notarized waiver from your current spouse.

Blending families can be challenging on many levels. Financial matters may be easier to deal with than personal aspects as long as you take appropriate steps to identify the issues and agree on your shared financial goals.

1–2) American Psychological Association, August 23, 2019 (most current information available)

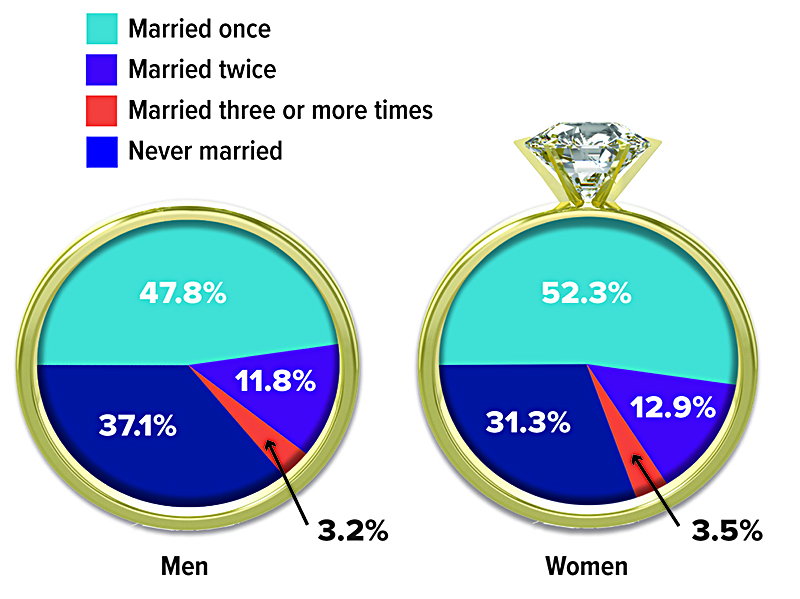

I Do, I Do

Roughly two out of three Americans ages 15 and older have been married at least once, and substantial number have been married more than once.

Source: U.S. Census Bureau, 2022 (2021 data)

How Taxes Impact Your Retirement-Income Strategy

Retirees face several unique challenges when managing their income, particularly when it comes to taxes. From understanding how taxes relate to Social Security and Medicare to determining when to tap taxable and tax-advantaged accounts, individuals must juggle a complicated mix of factors.

Social Security and Medicare

People are sometimes surprised to learn that a portion of Social Security income becomes federally taxable when combined income exceeds $25,000 for single taxpayers and $32,000 for married couples filing jointly. The taxable portion is up to 85% of benefits, depending on income and filing status.1

In addition, the amount retirees pay in Medicare premiums each year is based on the modified adjusted gross income (MAGI) from two years earlier. In other words, the cost retirees pay for Medicare in 2023 is based on the MAGI reported on their 2021 returns.

Taxable, Tax-Deferred, or Tax-Free?

Maintaining a mix of taxable, tax-deferred, and tax-free accounts offers flexibility in managing income each year. However, determining when and how to tap each type of account and asset can be tricky. Consider the following points:

Taxable accounts. Income from most dividends and fixed-income investments and gains from the sale of securities held 12 months or less are generally taxed at federal rates as high as 37%. By contrast, qualified dividends and gains from the sale of securities held longer than 12 months are generally taxed at lower capital gains rates, which max out at 20%.

Tax-deferred accounts. Distributions from traditional IRAs, traditional work-sponsored plans, and annuities are also generally subject to federal income tax. On the other hand, company stock held in a qualified work-sponsored plan is typically treated differently. Provided certain rules are followed, a portion of the stock’s value is generally taxed at the capital gains rate, no matter when it’s sold; however, if the stock is rolled into a traditional IRA, it loses this special tax treatment.2

Tax-free accounts. Qualified distributions from Roth accounts and Health Savings Accounts (HSAs) are tax-free and therefore will not affect Social Security taxability and Medicare premiums. Moreover, some types of fixed-income investments offer tax-free income at the federal and/or state levels. 3

The Impact of RMDs

One income-management strategy retirees often follow is to tap taxable accounts in the earlier years of retirement in order to allow the other accounts to continue benefiting from tax-deferred growth. However, traditional IRAs and workplace plans cannot grow indefinitely. Account holders must begin taking minimum distributions after they reach age 73 (for those who reach age 72 after December 31, 2022). Depending on an account’s total value, an RMD could bump an individual or couple into a higher tax bracket. (RMDs are not required from Roth IRAs and, beginning in 2024, work-based plan Roth accounts during the primary account holder’s lifetime.)

Don’t Forget State Taxes

State taxes are also a factor. Currently, seven states impose no income taxes, while New Hampshire taxes dividend and interest income and Washington taxes the capital gains of high earners. Twelve states tax at least a portion of a retiree’s Social Security benefits.

Eye on Washington

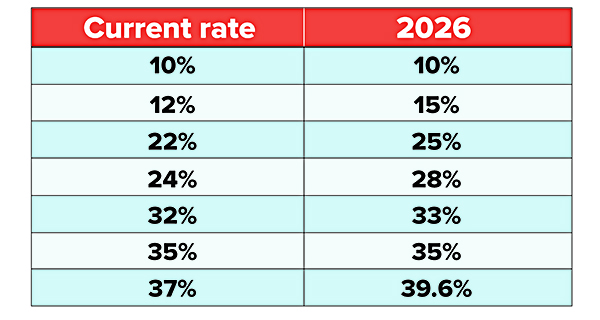

Finally, both current and future retirees will want to monitor congressional actions over the next few years. That’s because today’s historically low marginal tax rates are scheduled to revert to higher levels in 2026, unless legislation is enacted (see table).

Help is Available

Putting together a retirement-income strategy that strives to manage taxes is a complex task indeed. Investors may want to seek the help of a qualified tax or financial professional before making any final decisions.4

Tax Rates Scheduled to Rise

Unless legislation is enacted, federal marginal income tax rates are scheduled to rise in 2026.

1) Combined income is the sum of adjusted gross income, tax-exempt interest, and 50% of any Social Security benefits received.

2) Distributions from tax-deferred accounts and annuities prior to age 59½ are subject to a 10% penalty, unless an exception applies.

3) A qualified distribution from a Roth account is one that is made after the account has been held for at least five years and the account holder reaches age 59½, dies, or becomes disabled. A distribution from an HSA is qualified provided it is used to pay for covered medical expenses (see IRS publication 502). Nonqualified distributions will be subject to regular income taxes and penalties.

4) There is no guarantee that working with a financial professional will improve investment results.

A Mortgage Recast Is an Alternative to Refinancing

If you would like to reduce your monthly mortgage payment without having to refinance, then you may want to explore a mortgage recast. When you recast your mortgage, you put money toward the principal balance of your current home loan. Your mortgage lender then recalculates (reamortizes) your loan based on your new, lower balance, which reduces your monthly payment. Your interest rate and the number of years remaining on your loan stay the same. Here are three scenarios where a mortgage recast might be especially appealing.

- You have extra cash on hand, perhaps from a bonus or an inheritance. It’s sitting in a low-yield account.

- You are close to retirement or retired. You want to keep your home but lower your monthly expenses.

- You bought a new home with a smaller down payment than you intended because your old home is still on the market. But once your old home sells, the proceeds can be applied to your new mortgage through a recast.

Refinancing your mortgage may be a better option if your goal is to pay off your loan faster by shortening the term, or if you want to lower your interest rate or obtain cash. But if your objective is simply to lower your monthly payment and save on interest charges, then recasting your mortgage may be appropriate. Recasting is generally simpler and less expensive than refinancing because you’re keeping the same mortgage instead of applying for a new one. It doesn’t require an extensive application, a credit check, a new appraisal, or closing costs, though you typically will need to pay a processing fee.

Check with Your Lender

Not all mortgage lenders offer recasts, and some types of loans, including FHA, VA, USDA, and certain jumbo loans are not eligible for recasting. If you do qualify for a recast, your lender will give you more details about the process.

You may be able to recast once you’ve increased your equity by making extra payments or by paying a lump sum toward your mortgage balance. Minimums vary, but the additional principal required may be as little as $5,000. Of course, the more you put toward your principal, the lower your future monthly mortgage payment. If you are currently paying principal mortgage insurance (PMI), putting a lump sum toward your mortgage may help erase that, further lowering your monthly payment.

One drawback of a mortgage recast is that it could tie up money you might need later for other purposes. To access your equity in the future, you may need to refinance, take out a home equity loan, or even sell your home.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through DAI Securities, LLC, Member FINRA/SIPC. Financial Planning, Wealth Management and Tax Services offered through EagleStone Tax & Wealth. DAI Securities and EagleStone are not affiliated entities.

Financial Planning, Investment & Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax & Accounting services provided through EagleStone Tax & Accounting Services.

This communication is strictly intended for individuals residing in the state(s) of CO, DC, FL, KS, KY, MD, MA, NY, NC and VA. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2023.