EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

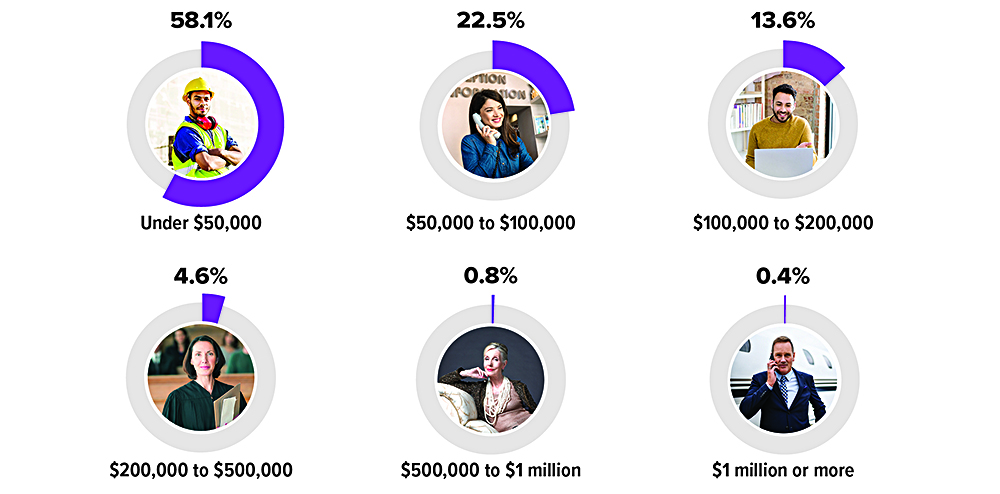

Where Does Your Income Fit?

The IRS processed more than 164 million individual income tax returns for tax year 2020 (most recent full-year data). Almost three out of five returns showed an adjusted gross income (AGI) under $50,000, while a little over 1% showed an AGI of $500,000 or more.

Source: Internal Revenue Service, 2022

Time for a Spring Cleanup: Organizing Your Financial Records

The arrival of spring is always a good time to dust off the cobwebs that have built up in your home during the winter. It’s also a good time to clean out and organize your financial records so you can quickly locate something if you need it.

Keep Only What You Need

If you keep paperwork because you “might need it someday,” your home office and file cabinets are likely overflowing and cluttered with nonessential documents. One key to organizing your financial records is to keep only what you absolutely need for as long as you need it.

Tax records. Keep all personal tax records for three years after filing your return or two years after the taxes were paid, whichever is later. (Different rules apply to business taxes.) If you underreported gross income by more than 25% (not a wise decision), keep the records for six years, and for seven years if you claimed a deduction for worthless securities or bad debt. It might be helpful to keep your actual tax returns, W-2 forms, and other income statements until you begin receiving Social Security benefits.

Financial statements. You generally have 60 days to dispute charges with banks and credit cards, so you could discard statements after two months. If you receive an annual statement, throw out monthly statements once you receive the annual statement. If your statements include tax information (e.g., you use credit-card statements to track deductions), follow the guidelines for tax records.

Retirement account statements. Keep quarterly statements until you receive your annual statement; keep annual statements until you close the account. Keep records of nondeductible IRA contributions indefinitely to prove you paid taxes on the funds.

Real estate and investment records. Keep at least until you sell the asset. If the sale is reported on your tax return, follow the rules for tax records. Utility bills can be discarded once the next bill is received showing the previous paid bill, unless you deduct utilities, such as for a home office.

Loan documents. Keep documents and proof of payment until the loan is paid off. After that, keep proof of final payment.

Insurance policies. Keep policy and payment documents as long as the policy is in force.

Auto records. Keep registration and title information until the car is sold. If you deduct auto expenses, keep mileage logs and receipts with your tax records. You might keep maintenance records for reference and to document services to a new buyer.

Medical records. Keep records indefinitely for surgeries, major illnesses, lab tests, and vaccinations. Keep payment records until you have proof of a zero balance. If you deduct medical expenses, keep receipts with your tax records.

These are general guidelines, and your personal circumstances may warrant keeping these documents for shorter or longer periods of time.

Securely Store Your Records

You can choose to keep hard copies of your financial records or store them digitally. You usually do not need to keep hard copies of documents and records that can be found online or duplicated elsewhere. Important documents such as birth certificates and other proof of identity should be stored in a safe place, such as a fire-resistant file cabinet or safe-deposit box. You can save or scan other documents on your computer, or store them on a portable drive, or use a cloud storage service that encrypts your uploaded information and stores it remotely.

An easy way to prevent documents from piling up is to remember the phrase “out with the old, in with the new.” For example, if you still receive paper copies of financial records, discard your old records as soon as you receive the new ones (using the aforementioned guidelines). Make sure to dispose of them properly by shredding documents that contain sensitive personal information, Social Security numbers, or financial account numbers. Finally, review your records regularly to make sure that your filing system remains organized.

.

Are You Eligible for Any of These College-Related Federal Tax Benefits?

College students and parents deserve all the help they can get when paying for college or repaying student loans. If you’re in this situation, here are three federal tax benefits that might help put a few more dollars back in your pocket.

American Opportunity Credit

The American Opportunity tax credit is worth up to $2,500 per student per year for qualified tuition and fees (not room and board) for the first four years of college. It is calculated as 100% of the first $2,000 of qualified tuition and fees plus 25% of the next $2,000 of such expenses.

There are two main eligibility restrictions: the student must be enrolled in college at least half-time, and the parents’ modified adjusted gross income (MAGI) must be below a certain level. To claim a $2,500 tax credit in 2023, single filers must have a MAGI of $80,000 or less, and joint filers must have a MAGI of $160,000 or less. A partial credit is available for single filers with a MAGI between $80,000 and $90,000, and joint filers with a MAGI between $160,000 and $180,000. The same limits applied in 2022 (and would be used when completing your 2022 federal tax return).

One key advantage of the American Opportunity credit is that it can be claimed for multiple students on a single tax return in the same year, provided each student qualifies independently. For example, if Mom and Dad have twins in college and meet the credit’s requirements for each child, they can claim a total credit of $5,000 ($2,500 per child).

Lifetime Learning Credit

The Lifetime Learning credit is worth up to $2,000 for qualified tuition and fees for courses taken throughout one’s lifetime to acquire or improve job skills. It’s broader than the American Opportunity credit — students enrolled less than half-time as well as graduate students are eligible. The Lifetime Learning credit is calculated as 20% of the first $10,000 of qualified tuition and fees (room and board expenses aren’t eligible).

Income eligibility limits for the Lifetime Learning credit are the same as the American Opportunity credit. In 2023, a full $2,000 tax credit is available for single filers with a MAGI of $80,000 or less, and joint filers with a MAGI of $160,000 or less. A partial credit is available for single filers with a MAGI between $80,000 and $90,000, and joint filers with a MAGI between $160,000 and $180,000. The same limits applied in 2022.

One disadvantage of the Lifetime Learning credit is that it is limited to a total of $2,000 per tax return per year, regardless of the number of students in a family who may qualify in a given year. So, in the previous example, Mom and Dad would be able to take a total Lifetime Learning credit of $2,000, not $4,000. Two other points to keep in mind: (1) the American Opportunity credit and the Lifetime Learning credit can’t be taken in the same year for the same student; and (2) the expenses used to qualify for either credit can’t be the same expenses used to qualify for tax-free distributions from a 529 plan or a Coverdell education savings account.

Student Loan Interest Deduction

Undergraduate and graduate borrowers can deduct up to $2,500 of interest paid on qualified federal and private student loans during the year if income limits are met. In 2023, a full $2,500 deduction is available for single filers with a MAGI of $75,000 or less, and joint filers with a MAGI of $155,000 or less. A partial deduction is available for single filers with a MAGI between $75,000 and $90,000, and joint filers with a MAGI between $155,000 and $185,000. In 2022, the income limits were slightly lower: a full deduction was available for single filers with a MAGI of $70,000 or less, and joint filers with a MAGI of $140,000 or less; a partial deduction was available for single filers with a MAGI between $70,000 and $85,000, and joint filers with a MAGI between $140,000 and $170,000. The 2022 limits would be used when completing your 2022 federal income tax return.

If you paid at least $600 in student loan interest during the year, your loan servicer should send you a Form 1098-E showing how much you paid. If you don’t receive a 1098-E, you can still claim the deduction. You just need to call your loan servicer or log in to your online account to find the amount of interest you paid.

50 and Older? Here's Your Chance to Catch Up on Retirement Saving

If you are age 50 or older and still working, you have a valuable opportunity to super-charge your retirement savings while managing your income tax liability. Catch-up contributions offer the chance to invest amounts over and above the standard annual limits in IRAs and workplace retirement plans.

2023 Limits

In 2023, the IRA catch-up limit is an additional $1,000 over the standard annual amount of $6,500. Participants in 401(k), 403(b), and government 457(b) plans can contribute an extra $7,500 over the standard limit of $22,500. For SIMPLE plans, the catch-up amount is $3,500 over the standard limit of $15,500.1

Tax Benefits

Contributions to traditional workplace plans are made on a pre-tax basis, which reduces the amount of income subject to current taxes. Contributions to traditional IRAs may be deductible, depending on certain circumstances.

If you are not covered by a retirement plan at work, your traditional IRA contributions are fully tax deductible. If you are covered by a workplace plan, you may deduct the full amount if your adjusted gross income is $73,000 or less as a single taxpayer or $116,000 or less if you’re married and file jointly. If you are not covered by a workplace plan but your spouse is, you are eligible for a full deduction if you file jointly and your income is $218,000 or less.2

Contributions to Roth accounts do not offer immediate tax benefits, but qualified distributions are tax-free at the federal, and possibly state, level. A qualified distribution is one made after the account has been held for five years and the account owner reaches age 59½, dies, or becomes disabled.

Distributions from traditional accounts prior to age 59½ and nonqualified distributions from Roth accounts are subject to ordinary income taxes and a 10% penalty, unless an exception applies.

Still Time for 2022 Contribution

If you qualify, you can make a deductible IRA contribution for 2022 up until the tax filing deadline on April 18, 2023. The total contribution limit for someone age 50 or older in 2022 is $7,000. You can open a new IRA or invest in a current one, but be sure to specify the contribution is for the 2022 tax year. The income limits for a full deduction in 2022 are $68,000 for single taxpayers, $109,000 for married taxpayers filing jointly, and $204,000 for taxpayers who aren’t covered by a workplace plan but their spouse is.2

1) Participants in 403(b) and 457(b) plans may benefit from other catch-up contributions specific to each plan type. Participants in government 457(b) plans cannot combine age 50 catch-up contributions with other catch-up contributions. When calculating allowable annual amounts, contributions to all plans except 457(b)s must be aggregated.

2) Phaseout limits apply. Married couples filing separately cannot take a full deduction. You must have earned income at least equal to your IRA contribution. Talk to a tax professional.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through DAI Securities, LLC, Member FINRA/SIPC. Financial Planning, Wealth Management and Tax Services offered through EagleStone Tax & Wealth. DAI Securities and EagleStone are not affiliated entities.

Financial Planning, Investment & Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax & Accounting services provided through EagleStone Tax & Accounting Services.

This communication is strictly intended for individuals residing in the state(s) of CO, DC, FL, KS, KY, MD, MA, NY, NC and VA. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2023.