EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

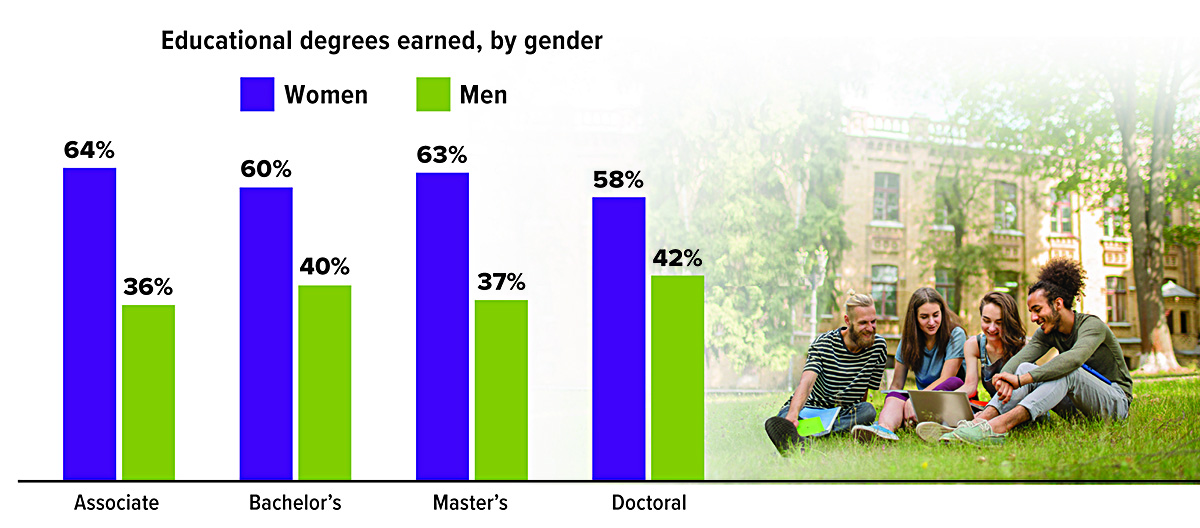

More Women Than Men Earn College Degrees

About 1,019,000 associate degrees, 2,136,000 bachelor’s degrees, 860,000 master’s degrees, and 206,200 doctoral degrees (which include medical and law degrees) are projected to be awarded during the 2023–2024 academic year. More women than men will attain undergraduate and graduate degrees at every level, a trend that is expected to continue.

Source: National Center for Education Statistics, 2023 (projected data)

A Pension Strategy that May Boost Your Income

If you participate in a traditional pension plan (also known as a defined benefit plan), your plan may offer several payout options including “qualified joint and survivor annuity” (QJSA) if you are married. A QJSA is an annuity that pays a dollar amount (usually monthly) for the rest of your life, with at least 50% of that amount continuing to your spouse after your death. However, if your spouse consents in writing, you can waive the QJSA and elect instead to receive a single-life annuity. With a single-life annuity, payments are made over your lifetime but stop upon your death. For example, if you receive just one payment after retirement and then die, the single-life annuity would end, and the plan would make no further payments.

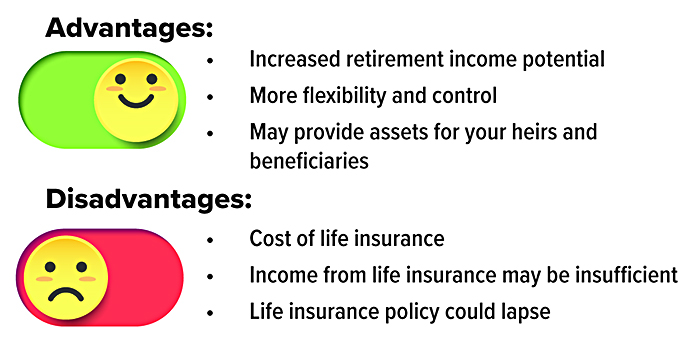

What is pension maximization?

Pension maximization is a strategy that may help solve this dilemma. The way it works is that your spouse waives the QJSA and you elect the single-life annuity. You then use the additional pension income to purchase insurance on your life, with your spouse named as beneficiary. If you die first, the pension payments will stop, but your spouse will receive the life insurance death proceeds free from federal income tax. The idea is that by coupling the larger pension payments with the purchase of a life insurance policy on your life, you may be able to increase your total income during retirement, while also providing for your spouse’s financial future if you die first.

Is pension maximization right for you?

There are a number of factors to consider. Are you insurable? If not, pension maximization is not a viable strategy. How much will the life insurance cost? (If you are relatively young and in good health, the insurance premiums may be much more affordable than if you are older and/or in poor health.) How much more does the single-life annuity pay than the QJSA? The larger the benefits under the single-life annuity, the more life insurance you’ll probably want to buy. (Also make sure to factor in any cost-of-living adjustment the pension plan may provide when analyzing your payment options.) How healthy is your spouse, and what is his/her life expectancy?

The monthly retirement benefits you and your spouse receive from your pension are generally treated as taxable income, subject to federal (and possibly state and local) income tax. This is true regardless of whether you elect a single-life annuity payout or a QJSA. However, since the pension benefits are larger with a single-life annuity, electing that payout option will increase your taxable income during retirement. If you elect the QJSA payout, when the first spouse dies, the pension payout to the survivor will be included in the survivor’s taxable income.

If you instead use the pension maximization strategy and die before your spouse, the life insurance death benefits will not be included in your surviving spouse’s taxable income, because life insurance death benefits generally pass free from income tax to the beneficiary of the policy. Any earnings from investments of the life insurance proceeds by your surviving spouse (e.g., interest, dividends, and capital gains) may generally be included in your spouse’s taxable income.

The pension maximization strategy is not for everyone, but it could be worth considering as you and your spouse evaluate your pension benefit options. (Note: Any guarantees associated with payment of death benefits, income options, or rates of return are based on the financial strength and claims-paying ability of the insurer. Policy loans and withdrawals will reduce the policy’s cash value and death benefit.)

Be sure to seek qualified professional guidance, since choosing a pension payout option and life insurance coverage can be complex and will impact both your financial future and your spouse’s.

Saving for College: 529 Plan vs. Roth IRA

529 plans were created in 1996 to give families a tax-advantaged way to save for college. Roth IRAs were created a year later to give people another tax-advantaged way to save for retirement. Along the way, some parents began using Roth IRAs as a college savings tool. And now, starting in 2024, extra funds in a 529 plan can be rolled over to a Roth IRA for the same beneficiary. Here’s how the two options compare in a few key areas.

Contribution rules

529 plan: Anyone can open a 529 account. In 2024, individuals can contribute up to $18,000 ($36,000 for married couples) without triggering gift tax implications. And under a special accelerated gifting rule unique to 529 plans, individuals can make a lump sum contribution in 2024 up to $90,000 ($180,000 for married couples) with no gift tax implications if they elect to spread the gift over five years. Lifetime contribution limits for 529 plans are high — most plans have lifetime limits of $350,000 and up (limits vary by state).

Roth IRA: Not everyone can contribute to a Roth IRA. In 2024, single filers must have a modified adjusted gross income (MAGI) of $146,000 or less and joint filers must have a MAGI of $230,000 or less. (A partial contribution is allowed for single filers with a MAGI between $146,000 and $161,000, and joint filers with a MAGI between $230,000 and $240,000.) In 2024, the annual contribution limit is $7,000 ($8,000 for people age 50 and older).

Tax benefits

529 plan: Earnings in a 529 account accumulate tax-deferred and are tax-free when withdrawn if funds are used to pay the beneficiary’s qualified education expenses, a broad term that includes tuition, fees, housing, food, and books. States generally follow this tax treatment, and some states may offer a tax deduction for 529 contributions. If funds in a 529 account are used for a non-qualified expense, the earnings portion of the withdrawal is subject to income tax and a 10% federal penalty.

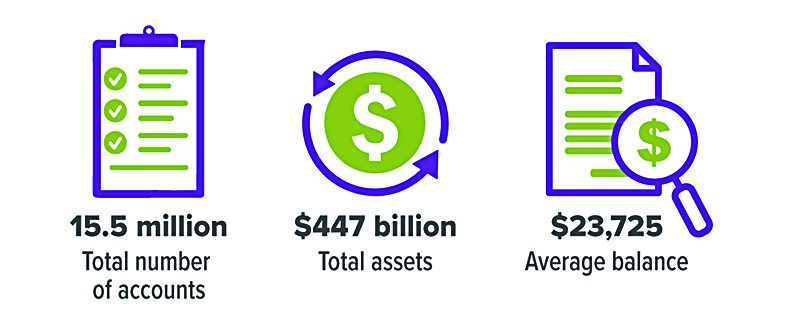

529 Plan Snapshot (2023)

Source: ISS Market Intelligence, 529 Market Highlights Q4 2023

Roth IRA: Earnings in a Roth IRA also accumulate tax-deferred and are tax-free if a distribution is qualified. A distribution is qualified if a five-year holding period is met and the distribution is made: (1) after age 59½, (2) due to a qualifying disability, (3) to pay certain first-time home buyer expenses, or (4) to your beneficiary after your death. If your distribution isn’t qualified, the earnings portion of the withdrawal is subject to income tax and, if you’re younger than 59½, a 10% early withdrawal penalty (unless an exception applies). One exception to this penalty is when the withdrawal is used to pay college expenses.

So, your age is key. Once you’ve met both the age 59½ and five-year holding requirements, money withdrawn from your Roth IRA to pay college expenses is tax-free. But even though withdrawing funds before age 59½ for college expenses won’t trigger an early withdrawal penalty, you may owe income tax on the earnings. (Nonqualified distributions draw out contributions first and earnings last, so you could withdraw up to the amount of your contributions and not owe income tax.)

Investment options and flexibility

529 plan: You’re limited to the investment options offered by the 529 plan. Plans typically offer a range of static and age-based portfolios (where the underlying investments automatically become more conservative as the beneficiary gets closer to college) with varying levels of risk, fees, and management goals. If you’re unhappy with the investment performance of the options you’ve chosen, you can change the investment options on your current contributions only twice per year, per federal law.

Roth IRA: With a Roth IRA, you generally can choose from a wide range of investments, and you can typically buy and sell investments whenever you like (usually incurring transaction costs and fees), so they offer a lot of flexibility.

There are generally fees and expenses associated with investing in a 529 plan, as well as the risk that investments may lose money or not perform well enough to cover college costs as anticipated. The tax implications of a 529 plan can vary from state to state and should be discussed with a legal and/or tax professional. States offering their own 529 plans may provide their residents and taxpayers with exclusive advantages and benefits, which may include financial aid, scholarship funds, and protection from creditors. Before investing in a 529 plan, consider the investment objectives, risks, charges, expenses, investment options, underlying investments, and the investment company, which are available in the official disclosure statement and applicable prospectuses. Contact your financial professional to obtain a copy.

Can Home Improvements Lower Your Tax Bill? It Depends

Most home improvements are not tax deductible — with one possible exception. In certain situations, you may be able to deduct improvements deemed necessary for medical reasons (not just beneficial to general health). If you itemize instead of taking the standard deduction, you can deduct unreimbursed medical expenses that exceed 7.5% of your adjusted gross income, so the tax savings could be significant if a costly home improvement pushes your total medical expenses above that threshold. Installing air conditioning to help treat asthma or modifying a home to make it wheelchair accessible are common examples of qualifying expenses.

Here are two more ways that improving your home could potentially reduce your tax burden.

Capital improvements

Projects that add to the value of your home, prolong its life, or adapt it to new uses are considered capital improvements. When you sell your home in the future, you can add the cost of capital improvements to your initial basis (what you paid for it originally), reducing your capital gain and the resulting tax bill.

Some examples of capital improvements include remodeling the kitchen, replacing all your home’s windows, adding a bathroom, or installing a new roof. Repairs that keep your home in good condition (such as repainting, replacing a broken door or window, or fixing a leak) don’t count as capital improvements. However, an entire repair job may be considered an improvement if it’s done as part of an extensive remodel or restoration.

Energy-saving tax credits

The Inflation Reduction Act of 2022 reconfigured two nonrefundable tax credits for home improvements that save energy. Unlike a deduction, which reduces your taxable income, a tax credit lowers your tax bill dollar for dollar. Both credits are available only for the installation of new products that meet specific energy efficiency requirements.

The energy efficient home improvement credit is equal to 30% of qualified expenditures for an existing home (not new construction). A $3,200 maximum annual credit is available through 2032. A $2,000 limit (30% of all costs, including labor) applies to electric or natural gas heat pumps, heat pump water heaters, and biomass stoves and boilers. A separate $1,200 limit applies to home energy audits and building envelope components (such as exterior doors, windows, skylights, and insulation) and energy property (including central air conditioners).

The residential clean energy property credit is a 30% tax credit available for qualifying expenditures for clean energy property (and related labor costs) such as solar panels, solar water heaters, geothermal heat pumps, wind turbines, fuel cells, and battery storage.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.