EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

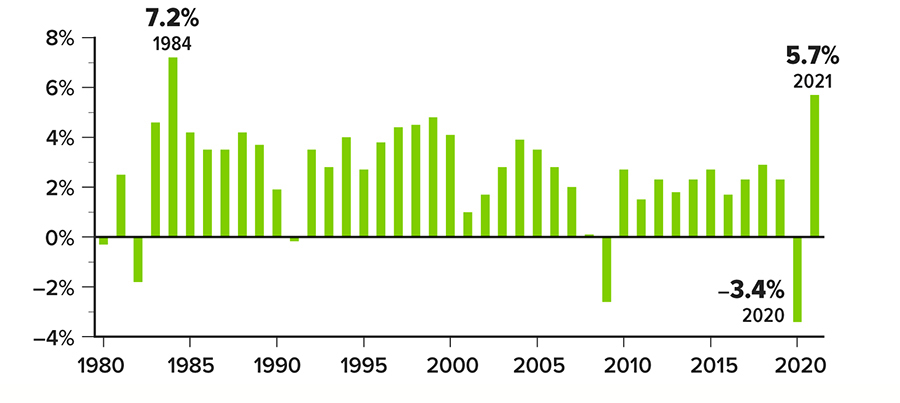

GDP Growth Highest in 37 Years

In 2021, U.S. real gross domestic product (GDP) — the value of goods and services produced in the United States — grew by 5.7%, the highest annual rate since 1984. This marked a strong recovery from 2020, when GDP dropped by 3.4%. Real GDP is adjusted for inflation to more accurately compare economic output at different periods. Current-dollar GDP, typically used to measure the overall size of the economy, increased by an even more impressive 10.1%.

Source: U.S. Bureau of Economic Analysis, 2022

Source: U.S. Bureau of Economic Analysis, 2022

Should You Consider Tapping the Equity in Your Home?

With home values skyrocketing recently, your home may be one of your largest assets. Using home equity to help finance other financial objectives is a strategy many people consider, but before doing so be sure you understand the risks as well as the potential benefits.

Home equity is the difference between how much your home is worth, based on current market conditions, minus your mortgage balance. Let’s say your home is worth $450,000 in the current market and your outstanding mortgage is $250,000. That means you have $200,000 in equity.

In most cases, lenders will allow you to borrow up to 80% of your home’s value minus your mortgage balance. In the example above, the total amount you might borrow would be $110,000 (assuming you qualify).

It’s probably best to be as conservative as possible when using home equity. There’s no guarantee that your home will maintain its current market value, so you could end up owing more than it’s worth. Moreover, in the unfortunate event of default, you could lose your house.

How to Access Home Equity

Generally, there are three ways to access home equity:

1. Cash-out refinance: In a cash-out refinance, you would refinance your mortgage for more than what you owe and take the difference in cash.

2. Home equity loan: With this type of loan, you would leave your current mortgage untouched and take out a separate loan against the equity in your home, with a fixed interest rate and fixed monthly payments.

3. Home equity line of credit: A HELOC works much like a credit card. You apply for a revolving credit amount up to a certain limit and, upon approval, have access to that money for a specific period, known as the draw period (usually 10 years). HELOC funds don’t all have to be used right away or at the same time. You can usually access the funds as needed by writing a check or using a linked credit card. Interest rates are variable; required payments will depend on how much you borrow and the prevailing rate. When the draw period ends, all outstanding balances need to be repaid.

Keep in mind that each of these options will have specific fees, including appraisal fees. A refinance could also require closing costs, which can equal thousands of dollars, depending on the amount borrowed.

The best type of loan will depend on your specific situation. If you need a fixed amount of money, a cash-out refinance or home equity loan might be appropriate. If you need an indeterminate amount over time or seek an emergency cash reserve, a HELOC might better serve your needs.

When Using Home Equity Might Make Sense

Because you’re putting your home at risk, it’s important to think critically and strategically when using home equity. Are you using the funds in a way that could reap future financial benefits, such as home repairs and improvements, helping to pay for a child’s college education, or consolidating high-interest debt? Then it might make sense. (A loan used for home repairs may also offer tax benefits; talk to a tax professional.) On the other hand, it might not be in your best financial interest if you’re thinking of using the money to fund an extravagant purchase, such as an expensive vacation or new luxury car.

Home equity loans and lines of credit that are not used to buy, build, or substantially improve your primary home (or a second home) are considered home equity debt; you cannot deduct the interest on home equity debt. With a cash-out refinance, you can only deduct interest on the new loan if you use the cash to make a capital improvement on your property.

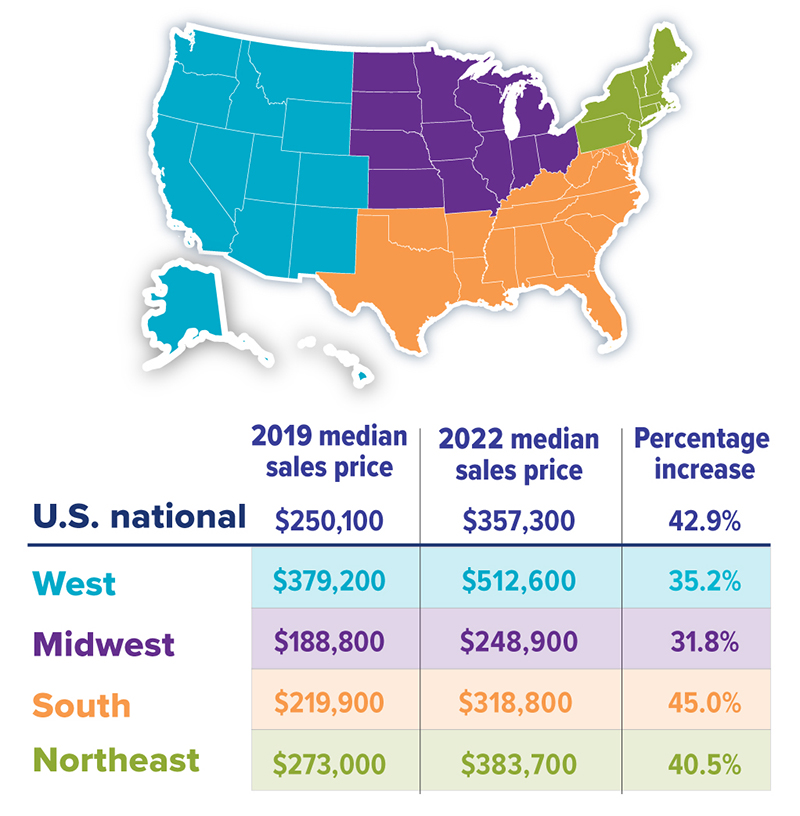

Growth in Home Sales Prices Since 2019

Source: National Association of Realtors, 2020-2022 (median existing-home sales data as of February 2019 and 2022)

Source: National Association of Realtors, 2020 -2022 (median existing-home sales data as of February 2019 and 2022)

A Wealth of Information: How to Read a Mutual Fund Prospectus

With more than 7,400 mutual funds to consider in the United States alone, some investors may feel overwhelmed by the thought of deciding which ones to select for their portfolios. At the same time, most mutual fund-owning households base their purchase decisions on these measures: historical performance (94%), investment objectives and risk potential (91%), and fees and expenses (90%).1

Fortunately, reading a mutual fund prospectus is a key way to learn important details about your investment options while learning more about how they may help you pursue your financial goals.

What’s in a Prospectus

A prospectus is a document containing specific details about the fund’s unique characteristics, designed to help investors better understand their options and make well-informed decisions. The Securities and Exchange Commission requires investment companies to provide prospective investors with a free, up-to-date prospectus for each fund they offer. Although the exact content of each prospectus varies from fund to fund, all prospectuses must include the same general information. (A shorter version, called a summary prospectus, contains much of the same information discussed here in an abbreviated format.)

Here’s an overview of what you’ll find in a fund prospectus — and why you should care.

Investment Objective, Strategies, and Risks

A fund’s investment objective describes the financial goal it targets on behalf of shareholders. For example, the objective could be capital appreciation (i.e., providing asset growth), income (providing interest or dividend payments), or a combination of the two.

The section of a prospectus highlighting a fund’s investment strategies, on the other hand, explains how the fund will invest its holdings to attempt to pursue its objectives. It typically identifies the geographic regions, industries, and types of securities the fund focuses on. It also lets you know whether the fund is actively managed or passively tracks the performance of a market index.

In addition, a prospectus lists the types of risk a particular fund or group of funds may entail, such as market risk, credit risk, inflation risk, and business or issuer risk. (See table for definitions.) This information clarifies exactly what types of risk you may encounter by adding a fund to your portfolio. All investments are subject to market fluctuations, risk, and loss of principal. Investments, when sold, may be worth more or less than their original cost. Investments seeking to achieve higher yields also involve a higher degree of risk.

Types of Mutual Fund Risk

Peace, Performace, and Management

The fees you pay to invest in mutual funds, such as sales charges and operating expenses, can have a direct impact on your net investment returns. To offer insight into how they may influence your portfolio’s bottom-line performance, a fund’s prospectus specifies the types and amount of fees the fund charges. Each prospectus must include a table illustrating the effect of those fees on a hypothetical investment over different time periods. You can also find details about a fund’s management team, rules for buying and selling shares, dividend payment policies, and other helpful information.

A prospectus is required to disclose the fund’s performance during the past 10 years (or since inception) and to compare its performance with that of a relevant market index. Keep in mind, however, that the performance of an index is not indicative of the performance of any particular investment, individuals cannot invest directly in an index, and past performance is not a guarantee of future results.

Mutual funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional.

1) Investment Company Institute, 2021-2022

Adjusting Your Tax Withholding

Now that you’ve seen last year’s tax results and can see where this year is heading, it may be a good time to consider adjustments to your income tax withholding.

Getting It Right

If you have too much tax withheld, you will receive a refund when you file your income tax return, but it might make more sense to reduce your withholding and receive more in your paycheck. However, if you have too little tax withheld, you will owe tax when you file your tax return and might owe a penalty.

Two tools — IRS Form W-4 and the Tax Withholding Estimator on irs.gov — can be used to help figure out the right amount of federal income tax to have withheld from your paycheck. This can be beneficial when tax laws change, your filing status changes, you start a new job, or there are other changes in your personal situation.

You might make a more concerted effort to review your withholding if any of the following situations apply to you:

- File as a two-income family

- Hold more than one job at the same time

- Work for only part of the year

- Claim credits, such as the child tax credit

- Itemize deductions

- Have a high income and a complex return

From W-4

In some circumstances, you will need to give your employer a new Form W-4 within 10 days (for example, if the number of allowances you are allowed to claim is reduced or your filing status changes from married to single). In other circumstances, you can submit a new Form W-4 whenever you wish. See IRS Publication 505 for more information.

Your employer will withhold tax from your paycheck based on the information you provide on Form W-4 and the IRS withholding tables.

If you have a large amount of nonwage income, such as interest, dividends, or capital gains, you might want to increase the tax withheld or claim fewer allowances. In this situation, also consider making estimated tax payments using IRS Form 1040-ES.

You can claim exemption from federal tax withholding on Form W-4 if both of these situations apply: (1) in the prior tax year, you were entitled to a refund of all federal income tax withheld because you had no tax liability, and (2) for the current year, you expect a refund of all federal income tax withheld because you anticipate having no tax liability.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Prepared by Broadridge Advisor Solutions Copyright 2022.