EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

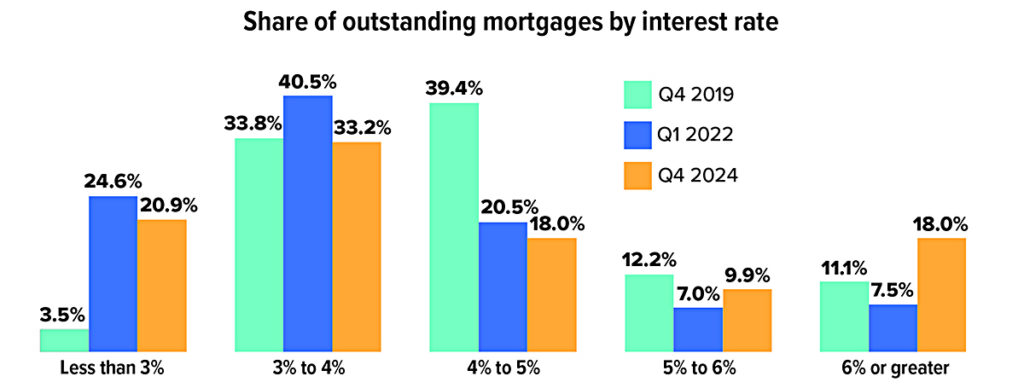

The Lock-in Effect Is Easing, But Oh So Slowly

The lock-in effect is a term that economists use to explain why the existing-home market has suffered from a severe lack of inventory in recent years. Homeowners have been discouraged from selling because they would have to finance their next homes at much higher rates than they pay on their current mortgages.

Nearly two-thirds of outstanding mortgages had rates below 4% in the first quarter of 2022, after many homeowners grabbed the chance to refinance at historically low rates during the pandemic. The share of mortgages with very low rates has ticked down since then, because some households want or need to sell regardless of interest rates, but it’s still much higher than before the pandemic. Although it’s possible that the lock-in effect may linger for years to come, it could loosen its grip on the housing market more quickly if mortgage rates drop.

Source: Federal Housing Finance Agency, 2025

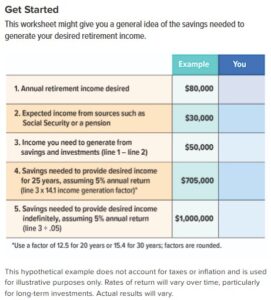

Have You Set a Retirement Savings Goal?

It’s difficult to reach a destination unless you know where you’re heading. Yet only 54% of workers or their spouses have tried to estimate the savings they would need to live comfortably in retirement.1

To get a start on establishing a retirement savings goal, use the simple worksheet on this page to compare the income you think you will need (or want) with the sources of income you expect. Keep in mind that estimates are in today’s dollars, so your desired income should account for the rising cost of living between now and the time you plan to retire.

How much will you need?

Everyone’s situation is different, but one common guideline is that you will need at least 70% to 80% of your pre-retirement income to meet your retirement expenses. This assumes that you will have paid off your mortgage, will have lower transportation and clothing expenses when you stop working, and will no longer be contributing to a retirement savings plan.

Although some expenses may be lower, others might increase, depending on your retirement lifestyle. For example, you may want to travel more or engage in new activities.

Unfortunately, medical expenses will likely be higher as you age. A recent study suggests that a man, woman, or couple who retired in 2024 at age 65 — with median prescription drug expenses and average Medigap premiums — might need $191,000, $226,000, or $366,000 in savings, respectively, to cover retirement health-care expenses (not including dental, vision, or long-term care).2 Future retirees may need even higher levels of savings.

Estimate income sources

You can estimate your monthly Social Security benefit at different retirement ages by establishing a my Social Security account at ssa.gov/myaccount. The closer you are to retirement, the more accurate this estimate will be. If retirement is many years away, your benefit could be affected by changes to the Social Security system, but it might also rise as your salary increases and the Social Security Administration makes cost-of-living adjustments.

If you expect a pension from current or previous employment, you should be able to obtain an estimate from the employer.

Add other sources of income, such as from consulting or a part-time job, if that is in your plans. Be realistic. Consulting can be lucrative, but part-time work often pays low wages, and working in retirement is less likely than you might expect. In 2025, 75% of workers expected to work for pay after retirement, but only 29% of retirees said they had actually done so.3

The income from your savings may depend on unpredictable market returns and the length of time you need your savings to last. Higher returns could enable your nest egg to grow faster, but it would be more prudent to use a modest rate of return in your calculations. Remember that all investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful. Investments seeking higher rates of return also involve a higher degree of risk.

The income from your savings may depend on unpredictable market returns and the length of time you need your savings to last. Higher returns could enable your nest egg to grow faster, but it would be more prudent to use a modest rate of return in your calculations. Remember that all investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful. Investments seeking higher rates of return also involve a higher degree of risk.

A more detailed projection

A rough estimate of your retirement savings goal is a good beginning, and a professional assessment may be the next step. Although there is no assurance that working with a financial professional will improve investment results, a professional can evaluate your objectives and resources and help you consider appropriate long-term financial strategies.

1–3) Employee Benefit Research Institute, 2025 (Health-care expenses include Medigap premiums, Medicare Part B premiums and deductibles, Medicare Part D premiums, and out-of-pocket prescription drug expenses; projection is based on a 90% chance of meeting expenses and assumes a 7.32% return on savings from age 65 until expenditures are made.)

Buying a Condo? Focus on the Financials

Condominiums, or condos, appeal to home buyers of all ages and life stages, but they are especially attractive to younger families and retirees who want to reap the benefits of homeownership while spending less time and money on upkeep.

Residential condos are typically individually owned apartments in multi-family buildings, but a condo is a form of property ownership, not a type of housing. Condos may also be attached or detached single-family units within a community. Each owner generally owns and maintains the interior of the unit and has a shared interest in exterior and common areas which are maintained by the community, such as the roof, lobby, and landscaping, and any amenities such as a fitness center, clubhouse, and pool.

Prices vary, depending on market and other factors, but condos are generally priced lower than single family houses. In 2024, the median price of a condo was about 12% less than a single family home.1 But that doesn’t necessarily mean you’re getting more bang for your buck. Condo ownership comes with some special costs and financial implications.

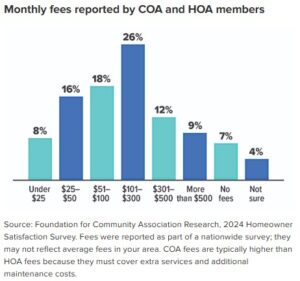

Factor in condo fees

In addition to making mortgage, condo insurance, and real estate tax payments, condo owners typically pay ongoing, mandatory fees (called assessments) to a condo association (COA) or homeowners association (HOA) to cover the costs of running and maintaining the community. Part of the fees collected often go into a reserve fund, which is money set aside to cover unexpected expenses.

On occasion, condo owners may be required to make a one-time payment in addition to regular monthly fees. This special assessment may be necessary when there is not enough money in the reserve fund to cover a large or unexpected expense.

When you’re buying a condo, it’s important to understand that fees are likely to go up each year, as maintenance and upgrade expenses, utility costs, and insurance premiums for the community increase. Fees vary widely, but condo fees that seem especially low in comparison to similar communities could be a red flag. Perhaps residents are unwilling to pay more to strengthen reserves or maintenance is being deferred, which is a serious issue that can lead to critical, expensive repairs, and diminish the property’s resale value. On the other hand, condo fees that seem especially high could also be a problem — will they become unaffordable if they continue to rise? High condo fees could also deter future buyers.

Look at appreciation potential

Like single family homes, condos may appreciate in value over time. In 2024, condos appreciated 2.9% on average, while single family homes appreciated 5%.2 Of course, real estate appreciation fluctuates, depending on market conditions, and depreciation is also possible. Before you make an offer, consider current value, market trends, location, size, age, condition, recent improvements, and whether any assessments might affect the future value.

Other considerations

Work with a knowledgeable real estate professional. Someone who knows the condo market well can help you navigate the buying process. This includes doing a comparable sales analysis and pointing out positive or negative factors that could affect future costs or appreciation potential.

Review condo documents. These will spell out community rules and regulations (called covenants, conditions, and restrictions) and bylaws. Also review financial statements to help ensure that the community is adequately funded, and ask questions.

Explore financing options. Getting a mortgage for a condo is generally similar to getting one for a single family home, but there are some different rules and qualifications. For example, the condo community must meet lender guidelines, so the lender may ask to review the community’s proof of insurance, financial statements, and condo documents. Interest rates and costs may vary, and not every lender will finance condominiums, so you’ll need to shop around.

Understand rental rules if you plan to rent out your condo. Some communities ban rentals, while others may have limits on the length of a lease or the percentage of owners who are able to rent their units.

1–2) National Association of Realtors, 2024

Tips to Help Preserve Your Inheritance

According to the Federal Reserve’s Survey of Consumer Finances, taken every three years, slightly more than one in five U.S. households had received an inheritance as of 2022.1 If you expect to receive an inheritance one day, these tips may help you better manage your financial windfall.

Wait a while before you act. Emotions run high after the death of a loved one. You might regret quitting your job, buying a sports car, or making other costly decisions before you have thought them through. Consider how the funds might be used to strengthen your financial position now and over the long term. You may also want to be discreet. Telling people that you have inherited a substantial amount of money may lead to unwanted advice, business or investment solicitations, and requests for financial support.

Boost (don’t blow up) your lifestyle. If you have a large balance on a high-interest credit card or vehicle loan, consider paying it off and using the increased cash flow to save more toward your retirement or other long-term goals. Whether it would be wise to pay off your mortgage depends on your individual circumstances and goals. Investing represents an opportunity to grow an inheritance and potentially make it last longer. You could use any income generated by your portfolio to supplement your paycheck, which might allow you to live better now while preserving the bulk of the money for future needs, such as a child’s education or your retirement.

Take advantage of tax deferral. If you inherit tax-deferred assets, such as those in a traditional 401(k) or IRA, keep in mind that withdrawals are taxed as ordinary income. You could choose to cash out and pay the taxes all at once, or you might consider transferring the inherited funds to a properly titled beneficiary IRA. Inherited retirement funds can be withdrawn over a period of up to 10 years, although some beneficiaries may have to take yearly required minimum distributions (if the original owner had started taking them). Spouses and other eligible designated beneficiaries receive preferential treatment. The rules and deadlines for handling inherited retirement account assets and taking distributions are complex. Because each choice could have far-reaching implications, be sure to seek tax guidance.

Consider meeting with a financial professional. Discussing your situation with someone outside of your family may help you gain perspective, clarify your goals, and make sound decisions. Although there is no assurance that working with a financial professional will improve investment results, he or she can consider your objectives and available resources and help you evaluate appropriate financial strategies.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.