EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

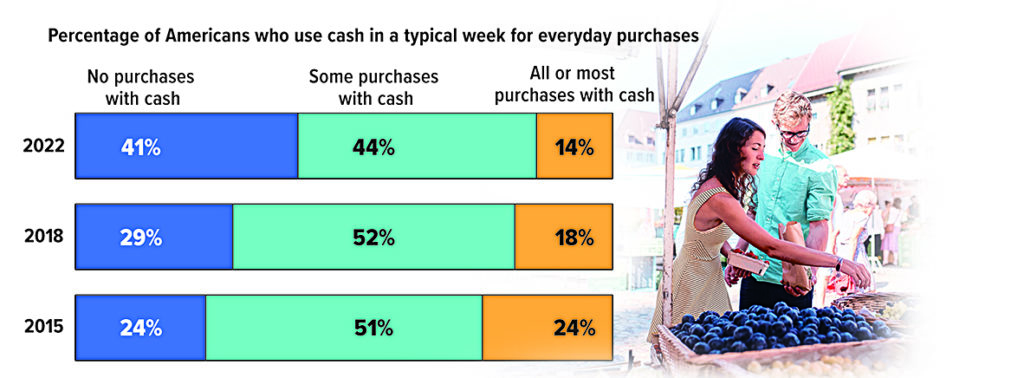

More Americans Embrace the Cashless Economy

A growing number of Americans are going “cashless” for everyday purchases like groceries, gas, services, and meals compared to previous years. A cashless payment might be made using a debit or credit card, or a payment app or mobile wallet on a smartphone.

In 2022, about 41% of Americans said none of their purchases in a typical week were paid for using cash, up from 29% in 2018 and 24% in 2015. Among affluent households, 59% said they didn’t use cash for any typical weekly purchases. The trend of not carrying cash varies by age, with 54% of people under age 50 saying they don’t worry much about whether they have cash on hand compared to 28% of people 50 and older.

Source: Pew Research Center, 2022 (numbers do not equal 100% due to rounding)

Give Your Money a Midyear Checkup

If 2023 has been financially challenging, why not take a moment to reflect on the progress you’ve made and the setbacks you’ve faced? Getting into the habit of reviewing your finances midyear may help you keep your financial plan on track while there’s still plenty of time left in the year to make adjustments.

Goal Overhaul

Rising prices put a dent in your budget. You put off a major purchase you had planned for, such as a home or new vehicle, hoping that inventory would increase and interest rates would decrease. A major life event is coming up, such as a family wedding, college, or a job transition.

Both economic and personal events can affect your financial goals. Are your priorities still the same as they were at the beginning of the year? Have you been able to save as much as you had planned? Are your income and expenses higher or lower than you expected? You may need to make changes to prevent your budget or savings from getting too far off course this year.

Post-Tax Season Estimate

Completing a midyear estimate of your tax liability may reveal planning opportunities. You can use last year’s tax return as a basis, then factor in any anticipated adjustments to your income and deductions for this year.

Check your withholding, especially if you owed taxes or received a large refund. Doing that now, rather than waiting until the end of the year, may help you avoid a big tax bill or having too much of your money tied up with Uncle Sam.

You can check your withholding by using the IRS Tax Withholding Estimator at irs.gov. If necessary, adjust the amount of federal income tax withheld from your paycheck by filing a new Form W-4 with your employer.

Investment Assessment

Review your portfolio to make sure your asset allocation is still in line with your financial goals, time horizon, and tolerance for risk. How have your investments performed against appropriate benchmarks, and in relationship to your expectations and needs? Looking for new opportunities or rebalancing may be appropriate, but be cautious about making significant changes while the market is volatile.

Asset allocation is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss. All investing involves risk, including the possible loss of principal and there is no guarantee that any investment strategy will be successful.

Retirement Savings Reality Check

If the value of your retirement portfolio has dipped, you may be concerned that you won’t have what you need in retirement. If retirement is years away, you have time to ride out (or even take advantage of) market ups and downs. If you’re still saving for retirement, look for opportunities to increase retirement plan contributions. For example, if you receive a pay increase this year, you could contribute a higher percentage of your salary to your employer-sponsored retirement plan, such as a 401(k), 403(b), or 457(b) plan. If you’re age 50 or older, consider making catch-up contributions to your employer plan. For 2023, the contribution limit is $22,500, or $30,000 if you’re eligible to make catch-up contributions.

If you are close to retirement or already retired, take another look at your retirement income needs and whether your current investment and distribution strategy will provide enough income. You can’t control challenging economic cycles, but you can take steps to help minimize the impact on your retirement.

More to Consider

Here are five questions to consider as part of your midyear financial review.

This hypothetical example is used for illustrative purposes only and does not represent the performance of any specific investment. Fees and expenses are not considered and would reduce the performance shown if they were included. Rates of return will vary over time, particularly for long-term investments. Actual results will vary.

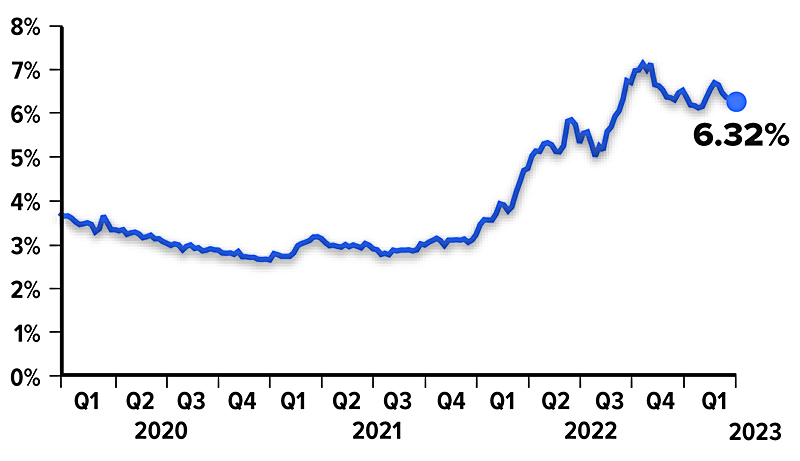

Financing Options to Help You Ride the Mortgage Rate Roller Coaster

The mortgage industry has been on a roller coaster ride over the last couple of years. Interest rates for fixed-rate mortgage loans were at historical lows during the beginning of the pandemic in 2020, rising to a 20-year high in late 2022 — and fluctuating ever since. 1 Many buyers are finding it difficult to afford a new home with traditional fixed-rate mortgage loans in such a high interest rate environment. As a result, more buyers are relying on alternative financing options to help lower their interest rates.2

Adjustable-Rate Mortgages

With an adjustable-rate mortgage (ARM), also referred to as a variable-rate mortgage, there is a fixed interest rate at the beginning of the loan which then adjusts annually for the remainder of the loan term. ARM rates are usually tied to the performance of an index. To determine the ARM rate, the lender will take the index rate and add it to an agreed-upon percentage rate, referred to as the margin. Most lenders offer ARMs with fixed-rate periods of five, seven or 10 years, along with caps that limit the amount by which rates and payments can change.

The initial interest rate on an ARM is generally lower than the rate on a traditional fixed-rate mortgage, which will result in a lower monthly mortgage payment. However, depending on interest rates, buyers with ARMs may find themselves with significantly higher mortgage payments once the fixed-rate period ends. Buyers should only consider ARMs if they can tolerate fluctuations in their mortgage payments or plan on refinancing or selling the home before the initial interest rate period ends.

Temporary Buydowns

A temporary buydown provides the buyer with a lower interest rate on a fixed-rate mortgage during the beginning of the loan period (e.g., the first one or two years) in exchange for an upfront fee or higher interest rate once the buydown feature expires. Buydowns typically offer large interest rate discounts (e.g., up to one to three percentage points, depending on the type of buydown). The costs associated with the buydown feature can be paid for by the home buyer, seller, builder, or mortgage lender.

While a buydown can make a home purchase more affordable at the beginning of the loan period, the long-term interest rates and mortgage payments on the loan can end up being substantially higher. This is why a borrower usually must initially qualify for the loan based on the full interest rate in effect after the buydown expires.

Assumable Mortgagaes

Assumable mortgages may be another way for buyers to circumvent high mortgage rates. An assumable mortgage is when a buyer takes over a seller’s existing loan and loan terms and pays cash or takes out a second mortgage to cover the remainder of the purchase price.

This type of loan could be advantageous if the existing loan has a low enough interest rate, and the buyer has enough access to cash or financing to cover the difference between the sale price and outstanding balance of the assumed loan. Not all mortgage loans are assumable — generally they are limited to certain types of government-backed loans (e.g., FHA, VA loans).

Other Incentives

One type of incentive offered by lenders is for a buyer to pay an upfront fee at closing, also known as points. By paying points at closing, buyers can reduce their interest rates — usually by around .25 percent per point — and lower their monthly mortgage loan payments. To make paying points cost effective, buyers should plan on staying in the home for several years so that they can recoup the costs. Sometimes a home builder or seller will offer to pay for points on a mortgage in order to attract more potential buyers.

Another incentive, often referred to as a “future refi,” is one that allows borrowers to purchase a home at current interest rates, with the ability to refinance their loans at a later date. The refinancing can be free or the costs can be rolled into the new loan, depending on the lender and loan type. Keep in mind that there is typically a set time period for refinancing with these types of loans.

1-2) Consumer Financial Protection Bureau, 2022

Should You Organize Your Business as an LLC?

There’s a certain amount of risk that comes with owning a business. Accidents can happen no matter how well a company is run, and a lawsuit could be devastating if the business is found to be at fault.

A limited liability company (LLC) is a business structure that offers many of the same legal protections as a corporation. Establishing an LLC creates a separate legal entity to help shield a business owner’s personal assets from lawsuits brought against the firm by customers or employees.

In theory, the financial exposure of the owners (members) would be limited to their stake in the company, but exceptions may include any business debt they personally guarantee or misdeeds (such as fraud) they carry out. But just like a corporation, an LLC can lose its limited liability if the owner does not follow formalities that continue to exhibit the separate existence of the business — which is known as “piercing the veil.”

Beyond liability protection, there are some additional benefits associated with LLCs.

Tax efficiency. An LLC is a pass-through entity for tax purposes, so a firm may pass any profits and losses to the owners, who report them on their personal tax returns. Members can elect whether the LLC should be taxed as a sole proprietorship, a partnership, an S corporation, or a C corporation, provided that it qualifies for the particular tax treatment. For example, about 71.5% of business partnerships are LLCs, as are 8.8% of sole proprietorships.1

Credibility. Starting an LLC may help a new business appear more professional than it would if it were operated as a sole proprietorship or partnership.

Simplicity. In most states, an LLC is easier to form than a corporation, and there may be fewer rules and compliance requirements associated with operating an LLC. The management structure is less formal, so a board of directors and annual meetings are not usually required.

Flexibility. Being registered as an LLC may facilitate growth because it’s possible to add an unlimited number of owners and/or investors to the business, and ownership stakes may be transferred easily from one member to another. LLCs may also be owned by another business.

The specific rules for forming an LLC vary by state, as do some of the tax rules and benefits. A written operating agreement that outlines the division of ownership, labor, and profits is a common requirement. It generally costs more to form and maintain an LLC than it does to operate as a sole proprietor or general partnership, but for many businesses the benefits may outweigh the costs.

1) Internal Revenue Service, 2022 (most recent data from 2019)

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.