EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

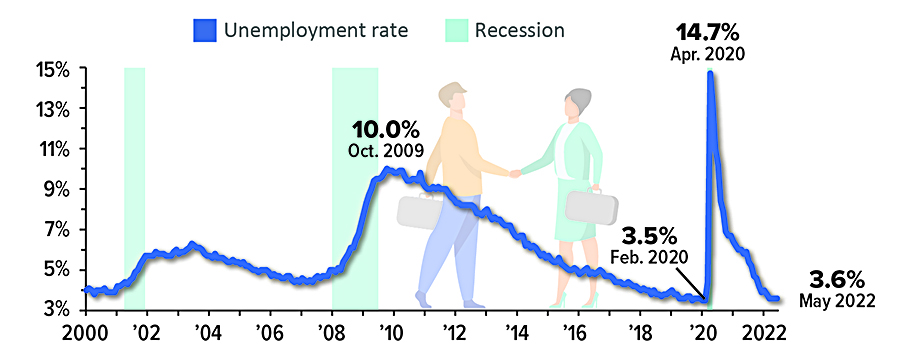

Quick Recovery for Unemployment Rate

The U.S. unemployment rate skyrocketed to 14.7% in April 2020 when the economy shut down in response to the pandemic. This was by far the highest rate since the current tracking system began in 1948. Fortunately, employment has recovered at a record pace — the unemployment rate was just 3.6% in March, April, and May 2022, nearly the same as before the pandemic.

The official unemployment rate only reflects unemployed workers who are actively looking for a job. A broader measure that captures workers who want a job but are not actively looking, as well as part-time workers who want full-time work, dropped from 22.9% in April 2020 to 7.1% in May 2022.

Source: U.S. Bureau of Labor Statistics, 2022; National Bureau of Economic Research, 2022

Source: U.S. Bureau of Labor Statistics, 2022; National Bureau of Economic Research, 2022

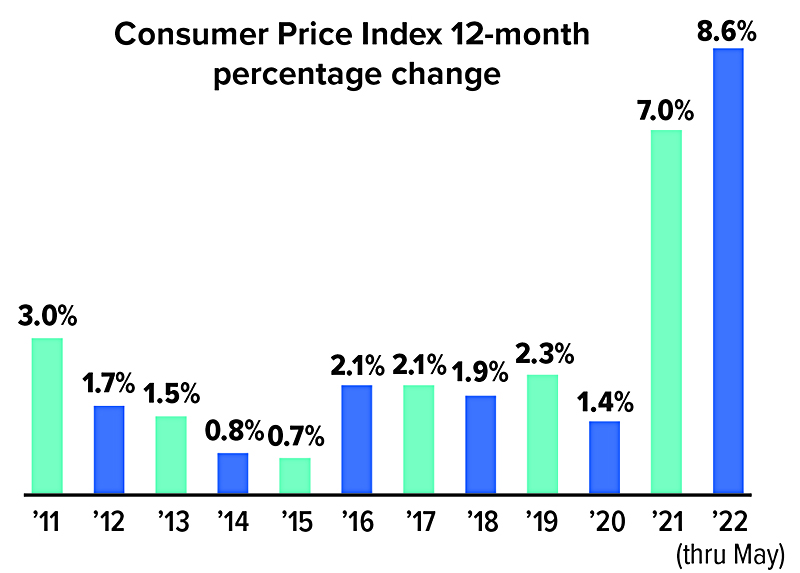

Inflation Protection for Investment Dollars

For the 12-month period ending in May 2022, the Consumer Price Index for All Urban Consumers (CPI-U) — the most widely used measure of inflation — increased 8.6%, the fastest pace in 40 years.1 The rate may trend downward as the Federal Reserve raises interest rates and supply-chain issues improve. But inflation is likely to be relatively high for some time.

High inflation not only hits consumers in the pocketbook for current spending, it also has a negative impact on the future purchasing power of fixed-income investments. For example, a hypothetical investment earning 5% annually would have a real return of –2.5% during a period of 7.5% annual inflation. This rate of return might be further reduced by taxes.

One way to help hedge your bond portfolio against inflation is by investing in Treasury Inflation-Protected Securities (TIPS).

How TIPS Fight Inflation

The principal value of TIPS is automatically adjusted twice a year to match any increases or decreases in the Consumer Price Index. If the CPI-U moves up or down, the Treasury recalculates your principal to reflect the change. A fixed rate of interest is paid twice a year based on the current principal, so the amount of interest may also fluctuate. Thus, you are trading the certainty of knowing exactly how much interest you’ll receive for the assurance that your investment will maintain its purchasing power over time.

Like all Treasury securities, TIPS are guaranteed by the federal government as to the timely payment of principal and interest. If you hold TIPS to maturity, you will receive the greater of the inflation-adjusted principal or the amount of your original investment.

Pricing-in Protection

TIPS pay lower interest rates than equivalent Treasury securities that don’t adjust for inflation. The breakeven inflation rate is the difference between the yield of TIPS and nominal (non-inflation-protected) Treasury securities with similar maturities. It is the premium the investor pays for inflation protection, as well as a market-based measure of expected inflation.

If inflation runs higher than expected, TIPS will earn a better return than nominal Treasury securities. If inflation runs below the breakeven rate, then TIPS have no clear advantage. However, the increased principal due to any level of inflation can still add to the value of your portfolio.

In some situations, TIPS can have negative interest rates that might produce a positive return after the principal is increased for inflation. For example, if a five-year TIPS offers a return of –0.5% while a five-year Treasury note offers a return of 2.5%, the 3% difference between these rates is the breakeven inflation rate. If inflation were to run at 4% over the five-year period, the TIPS would return 3.5% (4% – 0.5%) after adjustments for inflation, 1% higher than the return on the Treasury note.2

TIPS are sold in $100 increments and are available in maturities of 5, 10, and 30 years. As with all bonds, the return and principal value of TIPS on the secondary market will vary with market conditions, are sensitive to movements in interest rates, and may be worth more or less than their original cost. When interest rates rise, the value of existing TIPS will typically fall on the secondary market. Changing rates and secondary-market values should not affect the principal of TIPS held to maturity.

You must pay federal income tax each year on the interest income from TIPS plus any increase in principal, even though you won’t receive the principal and interest until the bonds mature. For this reason, investors might consider holding TIPS in a tax-deferred account such as an IRA.

1) U.S. Bureau of Labor Statistics, 2022

2) This hypothetical example of mathematical principles is used for illustrative purposes only. Rates of return will vary over time, particularly for long-term investments. Actual results will vary.

Eroding Purchasing Power

After an extended period of low inflation, consumer prices spiked in 2021 and 2022 due to supply and demand Imbalances as the U.S. economy reopened.

Source: U.S. Bureau of Labor Statistics, 2022

Life Insurance Living Benefits

When thinking about life insurance, you might focus on the death benefit that can be used for income replacement, business continuation, and estate preservation. But life insurance policies may include other provisions that allow you to access some or all of the death benefit while you are living. These features are often referred to as living benefits, which are usually offered as optional add-ons called riders.

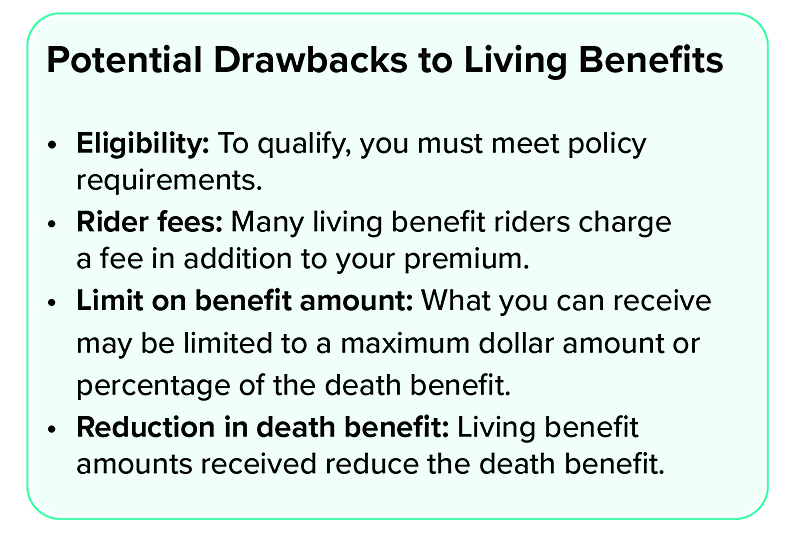

Some living benefit riders are added to a life insurance policy at no additional cost. Other riders are optional and come with an added cost to your basic policy premium. Living benefits vary depending on the type of life insurance and the company issuing the policy. Generally, living benefits are available to the policy owner, but using your living benefits will reduce the life insurance death benefit available for policy beneficiaries.

However, most riders let you take a portion of the total amount available — you don’t have to take the full amount so you can preserve a portion of the death benefit for your life insurance beneficiaries. Generally, living benefits are received free of income tax. Here are some common living benefits.

Accelerated Death Benefit for Terminal Illness

An accelerated benefit rider for terminal illness allows you to access a portion or all of the death benefit if you are diagnosed with a terminal illness or medical condition with a life expectancy of six to 24 months, depending on specific policy provisions. Most accelerated death benefit riders do not restrict how you use the money from the death benefit — you can use the money to help pay medical bills or other expenses arising from your illness. Or you can use the money to pay for funeral expenses.

Chronic Illness Rider

A chronic illness rider allows you to use a portion of your death benefit if you become chronically ill and cannot perform at least two of six activities of daily living (ADLs). These ADLs include bathing, continence, dressing, toileting, eating, and transferring. You may file a claim using this rider to receive a portion or possibly all of the death benefit. Usually, the insurance company will want to evaluate your claim and may require that you be examined by a medical professional chosen by the insurer. Often there are no restrictions on how you use the proceeds.

Critical Illness Rider

Similar to the chronic illness rider, the critical illness rider allows you to receive some or all of the death benefit if you are diagnosed with an illness or medical condition specified in the policy. Common critical illnesses include heart attack, stroke, cancer, end-stage renal failure, ALS, major organ transplant, blindness, or paralysis. With some critical illness riders, the percentage of death benefit available to you is based on the type of illness you have.

Long-term Care Rider

A long-term care rider can be added to a life insurance policy, generally for an additional cost, to help cover qualifying long-term care expenses. Like the chronic illness rider, you must be unable to perform at least two of six ADLs to claim a benefit. Unlike the chronic illness rider, the long-term care rider usually pays a portion of the death benefit on a periodic basis, commonly monthly. Some riders have a waiting period during which you must incur long-term care expenses before you can receive any proceeds. Other riders may only require that you cannot perform at least two of six ADLs, after which you receive periodic payments to use any way you wish.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable. An individual should have a need for life insurance and evaluate the policy on its merits as life insurance. Optional benefit riders are available for an additional fee and are subject to contractual terms, conditions, and limitations as outlined in the policy and may not benefit all investors. Any payments used for covered long-term care expenses would reduce (and are limited to) the death benefit or annuity value and can be much less than those of a typical long-term care policy. Policy guarantees are contingent on the financial strength and claims-paying ability of the insurance provider.

The Potential Benefits of Roth IRAs for Children

Most teenagers probably aren’t thinking about saving for retirement, buying a home, or even paying for college when they start their first jobs. Yet a first job can present an ideal opportunity to explain how a Roth IRA can become a valuable savings tool in the pursuit of future goals.

Rules of the Roth

Minors can contribute to a Roth IRA as long as they have earned income and a parent (or other adult) opens a custodial account in the child’s name. Contributions to a Roth IRA are made on an after-tax basis, which means they can be withdrawn at any time, for any reason, free of taxes and penalties. Earnings grow tax-free, although nonqualified withdrawals of earnings are generally taxed as ordinary income and may incur a 10% early-withdrawal penalty.

A withdrawal is considered qualified if the account is held for at least five years and the distribution is made after age 59½, as a result of the account owner’s disability or death, or to purchase a first home (up to a $10,000 lifetime limit). Penalty-free early withdrawals can also be used to pay for qualified higher-education expenses; however, regular income taxes will apply.

In 2022, the Roth IRA contribution limit for those under age 50 is the lesser of $6,000 or 100% of earned income. In other words, if a teenager earns $1,500 this year, his or her annual contribution limit would be $1,500. Other individuals may also contribute directly to a teen’s Roth IRA, but the total value of all contributions may not exceed the child’s annual earnings or $6,000 (in 2022), whichever is lower. (Note that contributions from others will count against the annual gift tax exclusion amount.)

Lessons for Life

When you open a Roth IRA for a minor, you’re giving more than just an investment account; you’re offering an opportunity to learn about important concepts that could provide a lifetime of financial benefits. For example, you can help explain the different types of investments, the power of compounding, and the benefits of tax-deferred investing. If you don’t feel comfortable explaining such topics, ask your financial professional for suggestions.

The young people in your life will thank you — sooner or later.

For questions about laws governing custodial Roth IRAs, consult your tax or legal professional. There is no assurance that working with a financial professional will improve investment results.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Prepared by Broadridge Advisor Solutions Copyright 2022.