EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

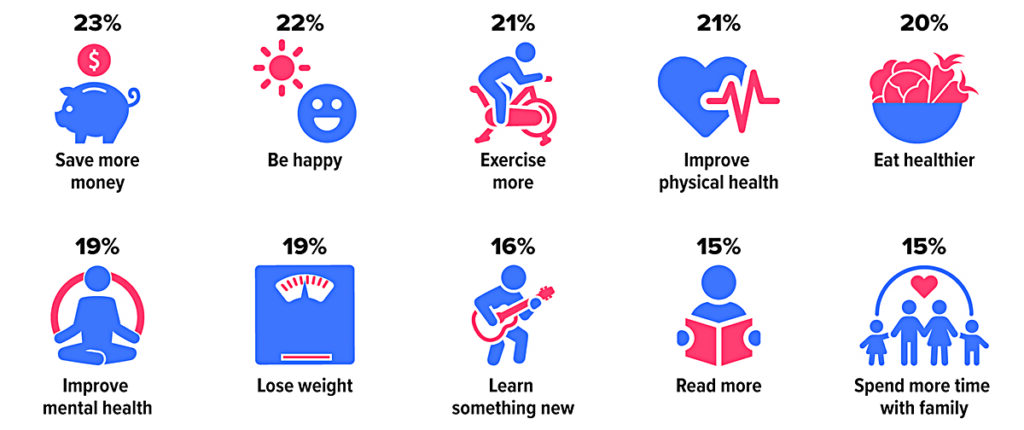

Do You Have a New Year's Resolution?

One out of three U.S. adults typically plan to make New Year’s resolutions. Younger people are more likely to make resolutions, and they tend to place more emphasis on finances, happiness, and mental health, whereas older people tend to emphasize physical health. Experts suggest that it’s easier to keep resolutions that are specific and measurable, and it can be helpful to reward yourself for meeting goals along the way.

These were the top 10 resolutions for 2024, ranked by the percentage of adults who said they would set these goals.

Sources: YouGov, December 21, 2023 (multiple responses allowed); Forbes Health, January 12, 2024

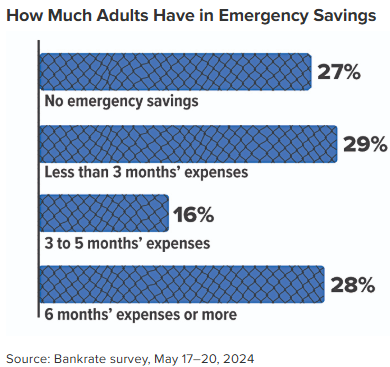

Financial Safety Nets: Exploring Available Sources of Emergency Funds

In moments of unexpected financial turmoil, having access to emergency funds can be the difference between a minor inconvenience and a major life disruption. Whether you have a sudden medical bill, car repair, or job loss, knowing where to turn for emergency financial support is crucial. However, not everyone has access to a financial safety net — nearly 60% of U.S. adults are uncomfortable with their level of emergency savings.1 Fortunately, there are options when it comes to exploring available sources of emergency funds.

Emergency savings account

A separate account dedicated solely to emergencies is the cornerstone of any financial plan and acts as the first line of defense in times of crisis. Generally, you’ll want to have at least three to six months’ worth of living expenses (e.g., mortgage, groceries, or car loan) in a readily accessible account. The actual amount, however, should be based on your particular circumstances, such as your job security, health, and income. In addition, review your emergency fund from time to time — either annually or when your personal or financial situation changes (e.g., a new baby or buying a home).

Credit cards and personal loans

While not ideal, credit cards can provide immediate access to funds in an emergency. They are particularly useful for covering short-term expenses that can be paid off quickly in order to avoid paying high interest rates. Cards that offer balance transfers with low introductory rates can also be used, as long as you are disciplined with your repayments in order to avoid incurring additional debt. Personal loans from banks, credit unions, or online lenders can also be a viable option for covering emergency expenses. These loans often come with fixed interest rates and structured repayment plans. However, loan eligibility and interest rates will vary, depending on the lender and your personal financial situation. And of course it takes time to obtain a loan.

HELOCs

For homeowners, a home equity line of credit (HELOC) is a revolving line of credit secured by the equity you’ve built in your home. Unlike a home equity loan, which provides a lump sum, a HELOC functions more like a credit card. You can borrow up to a predetermined credit limit and repay over time, with the ability to borrow again as needed during the draw period. This option usually offers lower interest rates and more flexibility compared to credit cards or personal loans. However, there are some drawbacks to using a HELOC. Most HELOCs have variable interest rates, which means payments can increase if interest rates rise. In addition, since a HELOC is secured by your home, you could face foreclosure if you can’t repay it.

Retirement accounts

When faced with an unexpected expense, another possible source of emergency funds is a retirement account, such as a 401(k) or IRA. Although most withdrawals prior to age 59½ are subject to income tax and a 10% penalty tax, you may be able to take penalty-free early distributions for specific emergencies. These include disability, extraordinary unreimbursed medical expenses, disaster recovery, up to $1,000 per year for general emergencies, and other situations. Ordinary income taxes and certain restrictions apply.

In addition, many 401(k) plans allow participants to take out loans. Typically, you can borrow up to 50% of your account balance or $50,000, whichever is less. The loans generally must be repaid within five years unless used for a first-time home purchase. You may also be able to take a hardship withdrawal in certain circumstances. Hardship withdrawals may be subject to the 10% early withdrawal penalty, as well as ordinary income tax. Check with your plan or IRA administrator to see what options are available to you.

Finally, keep in mind that contributions to a Roth IRA can be withdrawn at any time without taxes or penalties, since they are made with after-tax dollars. Nonqualified withdrawals of earnings, on the other hand, are subject to ordinary income taxes and the 10% early withdrawal penalty. Qualified Roth IRA withdrawals are those made after five years and the account owner reaches age 59½, dies, or becomes disabled.

1) Bankrate’s 2024 Annual Emergency Savings Report

Three Market-Moving Economic Indicators to Watch

Among all of the economic indicators released each month, three reports in particular can move the market: the Employment Situation, gross domestic product, and Personal Income and Outlays.

The Employment Situation

Each month, the Bureau of Labor Statistics (BLS) publishes the Employment Situation Summary report based on information from the prior month. The data for the report is derived primarily from two sources: (1) a survey of approximately 60,000 households, or about 110,000 individuals (household survey), and (2) an establishment survey of over 650,000 worksites. The information contained in each report includes the total number of employed and unemployed people, the unemployment rate, the number of people working full time or part time, average hourly and weekly earnings, and average hours worked per week.

According to the BLS, when workers are unemployed, they, their families, and the country as a whole can be negatively impacted. Workers and their families lose wages, and the country loses the goods or services that could have been produced. In addition, the purchasing power of these workers is lost, which can lead to unemployment for even more workers.

Investors pay particular attention to the information provided in this report. For instance, a rising unemployment rate may indicate a slowing economy. In this scenario, stock values may decline with falling corporate profits, while bond prices may rise as yields fall in response to lower interest rates. Slower wage growth may also be a sign of lower inflation and interest rates, and reduced economic productivity.

Gross domestic product

Gross domestic product (GDP) measures the value of goods and services produced by a nation’s economy less the value of goods and services used in production. GDP offers a broad measure of the nation’s overall economic activity in the U.S. and serves as a gauge of the country’s economic health. GDP contains a vast amount of economic information, including gross domestic income (the net of incomes earned and costs incurred in the production of GDP); gross output (the value of the goods and services produced by the nation’s economy); gross domestic purchase price index (measures the value of goods and services bought by U.S. residents); personal consumption expenditures (PCE) price index (costs of consumer goods and services); and profits from current production (corporate profits).

GDP can offer valuable information to investors, including whether the economy is expanding or contracting, trends in consumer spending, the status of residential and business investing, and whether prices for goods and services are rising or falling. A strong economy is usually good for corporations and their profits, which may boost stock prices. Increasing prices for goods and services may indicate advancing inflation, which can impact bond prices and yields. In short, GDP provides a snapshot of the strength of the economy over a month and a year and can play a role when making financial decisions.

Personal Income and Outlays

The Personal Income and Outlays report measures household income, expenditures, and savings. It also includes data on consumer prices for goods and services. In particular, this report includes data on personal income, disposable (after-tax) personal income, personal consumption expenditures, personal savings, and prices for consumer goods and services as measured by the PCE price index.

In general, consumer spending, which accounts for more than two-thirds of the economy, usually influences market performance. Knowing what consumers are buying (i.e., durable goods, nondurable goods, or services) may offer insight into how various market sectors might perform. Changes in income and spending can have a direct impact on the market. Greater spending usually enhances corporate profits and stock values and vice versa. While the Consumer Price Index may be the more recognized measure of inflation, the PCE price index is the Federal Reserve’s preferred measure of inflationary (or deflationary) trends. The rate of inflation and interest rates often move in the same direction because interest rates are the primary tool used by central banks (including the Federal Reserve) to manage inflation. Rising inflation usually prompts the Fed to increase interest rates, while falling inflation (and slowing economic growth) might lead to a decrease in interest rates to promote borrowing and stimulate the economy.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

What's New for 2025?

To help you stay informed, here are five changes you can look forward to in the new year.

Higher catch-up contributions for some. As of January 1, individuals ages 60 through 63 may be able to make increased catch-up contributions (if offered) to their workplace plan. The catch-up amount for people age 50 and older is $7,500 for 2025, but for people ages 60 through 63, the limit will be $11,250.1

Cap on out-of-pocket Medicare drug costs. A bit of welcome news for people with Medicare Part D prescription drug coverage — a $2,000 annual cap on out-of-pocket prescription costs takes effect on January 1.2 People with Part D will also now have the option to pay out-of-pocket costs in monthly installments over the course of the plan year instead of having to pay all at once at the pharmacy, which may help make it easier to manage prescription drug costs.

Automatic enrollment for new workplace retirement plans. Businesses that have adopted 401(k) and 403(b) plans since the passage of the SECURE 2.0 Act in December 2022 are now required to automatically enroll eligible employees at a contribution rate of 3% to 10%. After the first year, this rate will increase by 1% each year until it reaches 10% to 15%. New companies in business less than three years and employers with 10 or fewer employees are excluded, and other exceptions apply. Employees may opt out of coverage or elect a different percentage.

REAL ID deadline. The deadline for getting a REAL ID is May 7 (although the TSA has announced that enforcement may be phased in). As of that date, every air traveler who is at least 18 years old will need a REAL ID-compliant drivers license or identification card or another TSA-acceptable form of identification for domestic air travel and to enter certain federal facilities. Other TSA-acceptable documents are active passports, passport cards, or Global Entry cards. Standard drivers licenses will no longer be valid ID for TSA purposes, but enhanced drivers licenses from certain states are acceptable alternatives. Travelers who don’t have a REAL ID by the deadline could face delays at airport security checkpoints. Visit the TSA website at tsa.gov for updates and information.

New credit scoring risk model for mortgages. In late 2025, lenders are expected to begin using VantageScore 4.0 and FICO Score 10 T (instead of Classic FICO) to qualify borrowers. These new credit scoring models will provide a more precise assessment of credit risk.3 Models will consider trended credit data (an analysis of a customer’s behavior over time or historical payment and balance information) and other data not previously considered as part of the Classic FICO score, such as rent, utility, and telecom payments. This change will potentially help more applicants qualify for mortgages.

1–2) These are indexed annually for inflation so may rise each year.

3) Fannie Mae and Freddie Mac, 2024

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.