EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

Economy Staying Strong

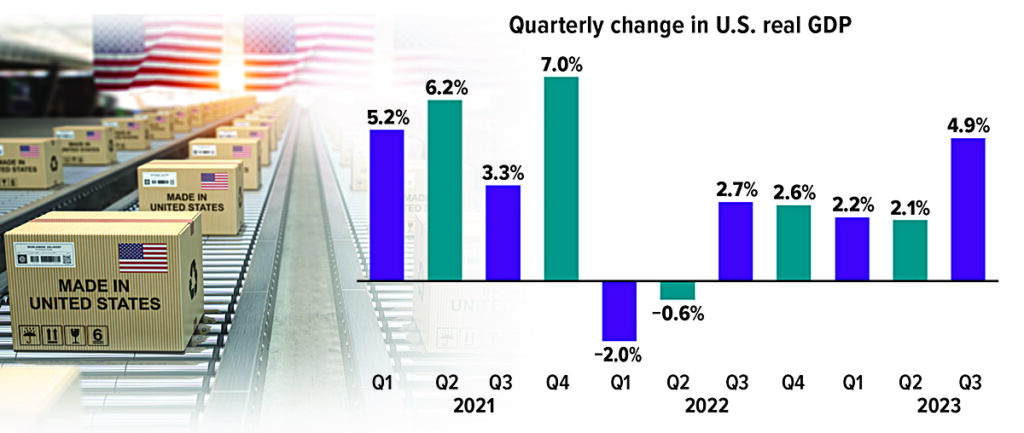

After a worrisome decline in the first half of 2022 — which sparked fears of a recession — U.S. inflation-adjusted gross domestic product (real GDP) has grown steadily. The third quarter of 2023 showed the strongest growth since the post-pandemic bounceback.

Current-dollar (nominal) GDP measures the total market value of goods and services produced in the United States at current prices. By adjusting for inflation, real GDP provides a more accurate comparison over time, making its rate of change a preferred indicator of the nation’s economic health.

Source: U.S. Bureau of Economic Analysis, 2023 (seasonally adjusted at annual rates; Q3 2023 based on advance estimate)

Do You Have These Key Estate Planning Documents?

Estate planning is the process of managing and preserving your assets while you are alive, and conserving and controlling their distribution after your death. There are four key estate planning documents almost everyone should have regardless of age, health, or wealth. They are: a durable power of attorney, advance medical directive(s), a will, and a letter of instruction.

Durable power of attorney

Incapacity can happen to anyone at any time, but your risk generally increases as you grow older. Consider what would happen if, for example, you were unable to make decisions or conduct your own affairs. Failing to plan may mean a court would have to appoint a guardian, and the guardian might make decisions that would be different from what you would have wanted.

A durable power of attorney (DPOA) enables you to authorize a family member or other trusted individual to make financial decisions or transact business on your behalf, even if you become incapacitated. The designated individual can do things like pay everyday expenses, collect benefits, watch over your investments, and file taxes.

There are two types of DPOAs: (1) an immediate DPOA, which is effective at once (this may be appropriate, for example, if you face a serious operation or illness), and (2) a springing DPOA, which is not effective unless you become incapacitated.

Advance medical directive(s)

An advance medical directive lets others know what forms of medical treatment you prefer and enables you to designate someone to make medical decisions for you in the event you can’t express your own wishes. If you don’t have an advance medical directive, health-care providers could use unwanted treatments and procedures to prolong your life at any cost.

There are three types of advance medical directives. Each state allows only a certain type (or types). You may find that one, two, or all three types are necessary to carry out all of your wishes for medical treatment.

- A living will is a document that specifies the types of medical treatment you would want, or not want, in a particular situation. In most states, a living will takes effect only under certain circumstances, such as a terminal illness or injury. Generally, one can be used solely to decline medical treatment that “serves only to postpone the moment of death.”

- A health-care proxy lets one or more family members or other trusted individuals make medical decisions for you. You decide how much power your representative will or won’t have.

- A do-not-resuscitate (DNR) order is a legal form, signed by both you and your doctor, that gives health-care professionals permission to carry out your wishes.

Will

A will is quite often the cornerstone of an estate plan. It is a formal, legal document that directs how your property is to be distributed when you die. Your will should generally be written, signed by you, and witnessed. If you don’t leave a will, disbursements will be made according to state law, which might not be what you would want.

There are a couple of other important purposes for a will. It allows you to name an executor to carry out your wishes, as specified in the will, and a guardian for your minor children.

Most wills have to be filed with the probate court. The executor collects assets, pays debts and taxes owed, and distributes any remaining property to the rightful heirs. The rules vary from state to state, but in some states smaller estates are exempt from probate or qualify for an expedited process.

Letter of instruction

A letter of instruction is an informal, nonlegal document that generally accompanies a will and is used to express your personal thoughts and directions regarding what is in the will (or about other things, such as your burial wishes or where to locate other documents). This can be the most helpful document you leave for your family members and your executor.

Unlike your will, a letter of instruction remains private. Therefore, it is an opportunity to say the things you would rather not make public.

A letter of instruction is not a substitute for a will. Any directions you include in the letter are only suggestions and are not binding. The people to whom you address the letter may follow or disregard any instructions.

Take steps now

Life is unpredictable. So take steps now, while you can, to have the proper documents in place to ensure that your wishes are carried out.

Source: Caring.com, 2023

Can Your Personality Influence Your Portfolio? New Research Points to Yes

Academic researchers have been exploring how investors’ personalities might affect their financial decisions and wealth outcomes.

In one study, three finance professors (Dr. Zhengyang Jiang from Northwestern University’s Kellogg School of Management, Cameron Peng from the London School of Economics, and Hongjun Yan from DePaul University’s Driehaus College of Business) surveyed more than 3,000 members of the American Association of Individual Investors — a relatively sophisticated group of market participants. These researchers examined correlations between five personality traits and the investors’ market expectations and portfolio allocations.1

Another study (by Mark Fenton-O’Creevy from The Open University Business School and Adrian Furnham from the BI Norwegian School of Management) involved more than 3,000 U.K. participants. These authors looked for correlations between the same five personality traits and three measures of wealth: property, savings and investments, and physical items.2

The Big Five

Both studies were designed around the “Big Five” model of personality, which has long been used by psychologists to measure people’s personalities and identify their dominant tendencies, based on five broad traits. These traits are openness to experience (curious and creative), conscientiousness (organized and responsible), extraversion (sociable and action-oriented), agreeableness (cooperative and empathetic), and neuroticism (emotionally unstable and worry-prone).

Each participant was rated on a spectrum for each trait according to how they answered survey questions, the results of which typically capture how individuals differ from one another in terms of their preferences, feelings, and behaviors.

Meaningful results

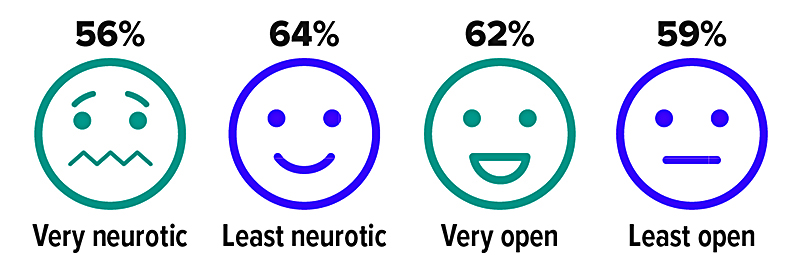

The first study pinpointed two traits that were closely correlated with investors’ market perceptions and investment behavior: openness and neuroticism. Investors who scored high for openness entertained the possibility of extreme market swings, but were more willing to bear the risk, and they allocated a larger share of their investment portfolios to stocks. Highly neurotic personalities were pessimistic about market performance, worried more about a potential crash, and had a smaller portion of their assets invested in stocks. Investors who scored higher on neuroticism and extraversion were more likely to buy certain investments when they became popular with people around them — which could easily take them down the wrong road.3

The second study found that conscientiousness was positively correlated with all three measures of wealth, even more so than education level, often because this personality type brings a diligent approach to saving and investing. Unfortunately, the traits of agreeableness, extraversion, and neuroticism were associated with lower lifetime wealth accumulation. Highly agreeable people may devote more of their money to helping others and might also be more vulnerable to financial scams, whereas extroverts could be more impulsive spenders.4

Both studies found common ground in one respect: highly neurotic investors tend to be risk-averse, and their volatility fears may cause them to have overly conservative portfolios.

Implications for investors

You might take some time to consider how your personality impacts the many financial decisions that you make in life. Becoming more self-aware may help you tap into your strengths and counter weaknesses that could prevent you from reaching your goals.

Even the most experienced investors can fall into psychological traps, but having a long-term perspective and a thoughtfully crafted investing strategy may help you avoid costly, emotion-driven mistakes. Also, discussing your concerns with an objective financial professional might help you deal with tendencies that could potentially cloud your judgment.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful. Although there is no assurance that working with a financial professional will improve investment results, a financial professional can provide education, identify appropriate strategies, and help you consider options that could have a substantial effect on your long-term financial prospects.

1, 3) “Personality Differences and Investment Decision-Making,” National Bureau of Economic Research, March 2023

2, 4) “Personality and Wealth,” Financial Planning Review, 2023

Small Businesses Could Face Borrowing Challenges

According to an October 2023 survey, higher interest rates impacted more than half of small businesses, and over 20% reported that higher rates and tighter lending standards influenced their hiring decisions.1

Small businesses paid an average rate of 9.1% for short-term loans in October 2023, the highest rate since 2006, and nearly twice as much as they were paying just two years ago (4.6% in August 2021).2

Despite these hurdles, many people who need working capital or want to start, invest in, or expand a business may need to borrow money. Here’s a rundown of some common financing options.

Bank loans. National and regional banks cater to the most creditworthy businesses, as they generally require significant collateral and documentation of stable profits. New or fast-growing small businesses (even healthy ones with good prospects) are often rejected. Small banks, however, tend to have higher approval rates than large banks.3

SBA programs. In fiscal year 2022, the U.S. Small Business Administration (SBA) provided more than $43 billion in financing, in many cases to guarantee loans issued by participating banks.4 The program often makes it easier to qualify for financing and may offer more competitive terms and longer repayment periods. However, traditional SBA loans also require “worthwhile” collateral, and it can take several months for qualified borrowers to complete the application process (through a local bank or online).

Other lenders. Online lenders that use digital technology to approve smaller, short-term loans can sometimes make it easier to access cash quickly, but they often charge higher interest rates and fees. Some loans may need to be backed by business assets such as securities, equipment, inventory, and accounts receivable.

HELOCs. Homeowners may have an extra source of funds to tap into for business needs. A home equity line of credit, or HELOC, is a secured loan that may offer more flexible repayment periods and competitive interest rates than many other types of business financing. But there is one major disadvantage to consider: if the business struggles and the owner can’t make loan payments, the lender could take the home.

Credit cards. Business accounts tend to charge higher interest rates — which could now be north of 20% — and offer fewer protections than personal credit cards. Using a business credit card responsibly, however, is one way that a new business can establish the positive credit history necessary to obtain bank loans at better rates in the future.

1) The Wall Street Journal, November 14, 2023

2) National Federation of Independent Business, October 2023

3) 2022 Small Business Credit Survey, Federal Reserve, 2023

4) U.S. Small Business Administration, 2022

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.