EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

Saving Less? You're Not Alone

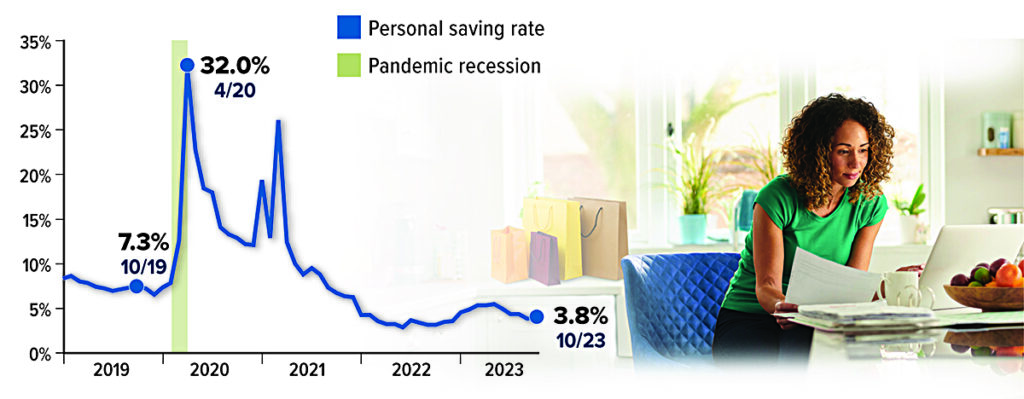

The U.S. personal saving rate — the percentage of personal income that remains after taxes and spending — was 3.8% in October 2023. The saving rate spiked to an all-time high during the pandemic, when consumers received government stimulus money with little opportunity to spend, but fell quickly as stimulus payments ended and high inflation ate into disposable income. The current level is well below pre-pandemic saving rates.

A low personal saving rate means there is less money available on a monthly basis for saving and investment. However, many households still have pandemic-era savings, and the low rate indicates consumers are willing to spend, which is good for the economy. The question is how long this spending can be sustained.

Sources: U.S. Bureau of Economic Analysis, 2023; Bloomberg, October 10, 2023

How Savers and Spenders Can Meet in the Middle

Couples who have opposite philosophies regarding saving and spending often have trouble finding common ground, and money arguments frequently erupt. But you can learn to work with — and even appreciate — your financial differences.

Money habits run deep

If you’re a saver, you prioritize having money in the bank and investing in your future. You probably hate credit card debt and spend money cautiously. Your spender spouse may seem impulsive, prompting you to think, “Don’t you care about our future?” But you may come across as controlling or miserly to your spouse who thinks, “Just for once, can’t you loosen up? We need some things!”

Such different outlooks can lead to mistrust and resentment. But are your characterizations fair? Money habits run deep, and have a lot to do with how you were raised and your personal experience. Instead of assigning blame, focus on finding out how each partner’s financial outlook evolved.

Saving and spending actually go hand in hand. Whether you’re saving for a vacation, a car, college, or retirement, your money will eventually be spent on something. You just need to decide together how and when to spend it.

Talk through your differences

Sometimes couples avoid talking about money because they are afraid to argue. But scheduling regular money meetings could give you more insight into your finances and provide a forum for handling disagreements, helping you avoid future conflicts.

You might not have an equal understanding of your finances, so start with the basics. How much money is coming in and how much is going out? Next, work on discovering what’s important to each of you.

To help ensure a productive discussion, establish some ground rules. For example, you might set a time limit, insist that both of you come prepared, and take a break if the discussion becomes too heated. Communication and compromise are key. Don’t just assume you know what your spouse is thinking — ask, and keep an open mind.

Here are some questions to get started.

- What does money represent to you? Security? Freedom? The opportunity to help others?

- What are your short-term and long-term savings goals? Why are these important to you?

- How comfortable are you with debt? This could include mortgage debt, credit card debt, and loans.

- Who should you spend money on? Do you agree on how much to give to your children or spend on gifts to family members, friends, or charities?

- What rules would you like to apply to purchases? For example, you might set a limit on how much one spouse can spend without consulting the other.

- Would you like to set aside some discretionary money for each of you? That could help you feel more free to save or spend those dollars without having to justify your decision.

Agree on a plan

Once you’ve explored what’s important to you, create a concrete budget or spending plan that will help keep you on the same page. For example, to account for both perspectives, you could make savings an “expense” and also include a “just for fun” category. If a formal budget doesn’t work for you, find other ways to blend your styles, such as automating your savings or bill paying, prioritizing an emergency account, or agreeing to put specific percentages of your income toward wants, needs, and savings.

And track your progress. Scheduling money dates to go over your finances will give you a chance to celebrate your successes or identify what needs to improve. Be willing to make adjustments if necessary. It’s hard to break out of patterns, but with consistent effort and good communication, you’ll have a strong chance of finding the middle ground.

Source: Consumer Financial Protection Bureau

Extreme Weather and Your Home Insurance: How to Navigate the Financial Storm

With wildfires in Maui, Hurricane Idalia in Florida, and the heat wave that blanketed the South, Midwest, and Great Plains, 2023 was a record-setting year for extreme weather in the United States. In fact, last year the U.S. saw more weather and climate-related disasters that cost over $1 billion than ever before. 1

As a result of these extreme weather events, many insurance companies have begun to raise rates, restrict coverage, or stop selling policies in high-risk areas. This has left homeowners in a precarious situation when it comes to home insurance, as many are now faced with higher premiums, lower home values, and the possibility of the nonrenewal of their policies.

If you live in an area that is susceptible to extreme weather events, you’ll want to be prepared for the possible disruption of your home insurance coverage. The key is to act quickly so that you can manage your financial risk and help make sure that your home is protected.

Handling a nonrenewal

Depending on the state you live in, if your insurer chooses not to renew your coverage, they generally have 30 to 60 days to send you a notice of nonrenewal. Your first step should be to contact your insurer and ask why your policy wasn’t renewed. They may reverse their decision and renew your policy if the reason for nonrenewal can be fixed, such as by installing a fire alarm system or fortifying a roof.

If that doesn’t work, you should begin shopping for new coverage as soon as possible. Start by contacting your insurance agent or broker or your state’s insurance department to find out which licensed insurance companies are still selling policies in your area. You can also try using the various online comparison tools that will allow you to compare rates and coverage amongst different insurers. Finally, ask for recommendations for insurers from friends, neighbors, and coworkers who live nearby.

Consider high-risk home insurance

If your home is deemed to be at high risk due to its geographic area, you may want to look for an insurance company that specializes in high-risk home insurance.

High-risk policies often have significant exclusions and policy limits and are more expensive than traditional home insurance policies. However, they can provide coverage to a home that might otherwise be uninsurable.

Use a FAIR plan as a last resort

If you have trouble obtaining standard home insurance coverage, you may be eligible to obtain coverage under your state’s Fair Access to Insurance Requirements (FAIR) plan. Many states offer homeowners access to some type of FAIR plan.2

FAIR plans are often referred to as “last resort” plans, since homeowners who obtain insurance through a FAIR plan are usually not eligible for standard home insurance coverage due to their home being located in a high-risk area. Coverage under a FAIR plan is more expensive than standard home insurance and is fairly limited — it usually only provides basic dwelling coverage, although some states may offer other coverage options for things like personal belongings or additional structures. In addition, most states require you to show proof that you have been denied coverage before you can apply for a FAIR plan.

Avoid expensive force-placed insurance

If you have a mortgage, your lender will require your home to be properly insured. If you lose your home insurance coverage or your coverage is deemed insufficient, your lender will purchase home insurance for you and charge you for it. These types of policies are referred to as “force-placed insurance” and are designed to protect lenders, not homeowners. They usually only provide limited coverage, such as coverage for the amount due on the loan or replacement coverage if the structure is lost.

Force-placed insurance policies are typically much more expensive than traditional home insurance, with the premiums being paid upfront by your lender and added on to your monthly mortgage payment. Your lender is required to give you notice before it charges you for force-placed insurance. In addition, you have the right to have the force-placed insurance removed once you obtain proper home insurance coverage on your own.

1) NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters, 2023

2) National Association of Insurance Commissioners, 2023

2) National Association of Insurance Commissioners, 2023

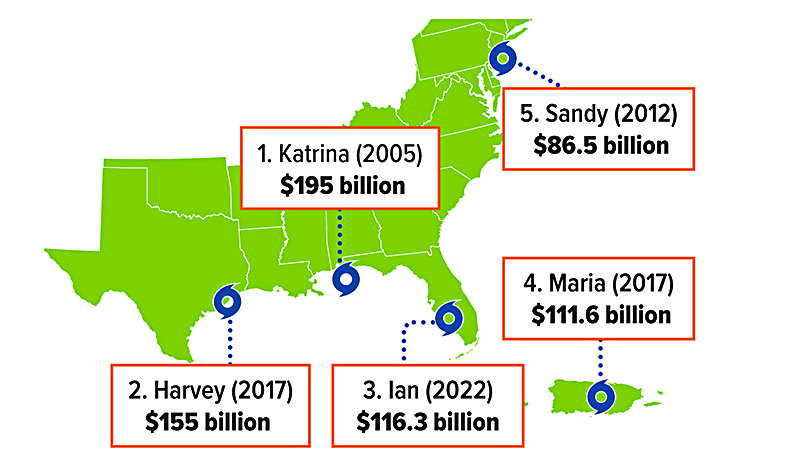

United States infographic map concept with space for your copy.

Source: NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters, 2023

SoSEPPs Allow Penalty-Free Access to Retirement Savings at Any Age

You’re probably aware that a 10% penalty tax generally applies to distributions from qualified retirement plan accounts prior to age 59½, unless an exception applies; however, you may not be aware of the exception that allows retirement account holders to access their savings at any age, penalty-free.1 Specifically, this exception allows distributions through a series of substantially equal periodic payments (SoSEPPs). Also known as the 72(t) strategy, SoSEPPs are subject to strict and complicated rules, so it may be best to proceed with caution.

SoSEPPs explained

Under the SoSEPP rule, you can take distributions from IRAs and most work-based plan accounts in a series of regular payments calculated using a specific method over a certain period of time. The payments must be taken at least annually and continue for a minimum of five years or until you reach age 59½, whichever is later. You may also be allowed to establish an installment arrangement — quarterly or monthly, for example — that totals the required payment each year. With respect to work-based plans, SoSEPPs can be used only after you separate from service from the employer maintaining the plan.

You may use one of three methods for calculating the payment — the required minimum distribution (RMD) method, the fixed amortization method, or the fixed annuitization method. Distribution amounts are based on your life expectancy or that of you and your beneficiary. To calculate the correct amount, you’ll need to determine which method to use and then choose a life expectancy table (found in IRS Publication 590-B), interest rate (for the amortization or annuitization methods only), and account valuation date.

The IRS permits a one-time change from either the amortization or annuitization method to the RMD method. Otherwise, if you change from one distribution method to another or fail to take the required amount in any given year, the 10% penalty (plus interest) will generally apply to not only the current year’s distribution(s) but to all prior SoSEPP distributions.2

Note that you cannot make additional contributions to the account nor take payments other than the SoSEPPs during the required period. Additionally, if the account balance reaches zero before the required time period is up, no penalty will apply.

Although it may be comforting to know you can access your retirement account penalty-free at any age, calculating and managing SoSEPPs is a complex process. Mistakes can be costly. For these reasons, you may want to seek the guidance of a qualified tax professional before making any decisions.

1) There is a 25% penalty for distributions from SIMPLE IRAs taken within the first two years of participation.

2) The 10% penalty, plus interest, does not apply if the change was due to death, disability, or another IRS-approved reason.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.