EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

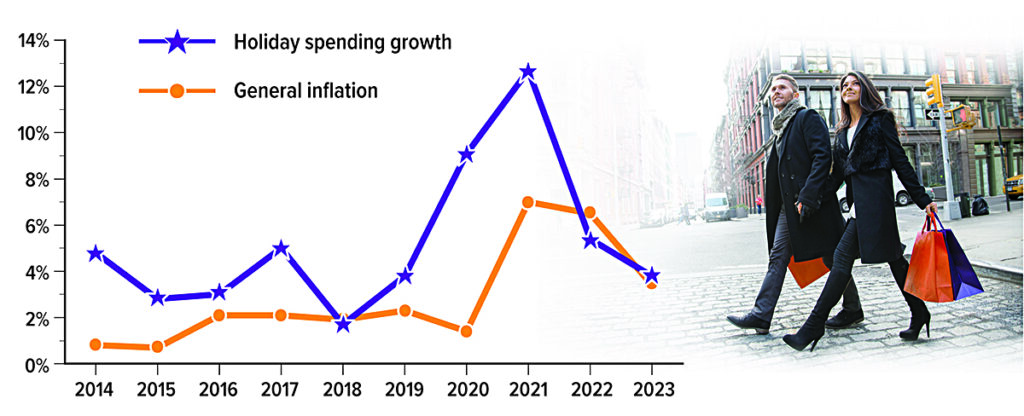

Will Holiday Spending Outpace Inflation?

Retail spending during the winter holiday months of November and December accounts for about 19% of total annual retail spending and is even more significant for some retail sectors.

In 2023, consumers spent $964.4 billion on retail goods and services during the holiday months. This was a 3.8% increase over 2022 and above the 3.4% rate of general inflation. Over the last decade, holiday spending has usually outpaced inflation, sometimes by a wide margin. With inflation slowing in 2024, this trend could continue.

Sources: National Retail Federation (NRF), January 17, 2024; U.S. Bureau of Labor Statistics, 2024 (In calculating retail sales, the NRF includes stores, online, and other non-store sales but excludes automotive dealers, gas stations, and restaurants.)

Would You Be Prepared for an Unplanned Early Retirement?

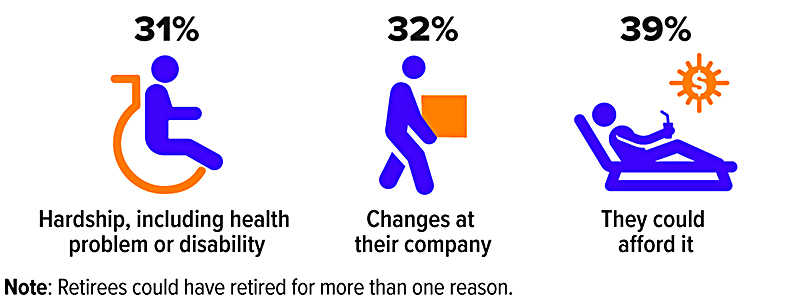

Most of us would prefer not to think about an unexpected (and unwelcome) early retirement, but it does happen frequently. In fact, nearly half of current retirees retired earlier than planned, and of that group, more than 60% did so due to changes at their company or a hardship, such as disability.1 For that reason, it’s a good idea to take certain steps now to help prepare for the unexpected.

What you can do now

Save as much as possible in tax-advantaged accounts. If you’re forced to retire earlier than planned, your work-sponsored retirement plans, IRAs, and health savings accounts (HSAs) could become critical resources. HSA assets can be used tax-free to pay for qualified medical expenses at any time, and you can generally tap your retirement plan and IRA assets after age 59½ without penalty. Although ordinary income taxes apply to distributions from pre-tax accounts, qualified withdrawals from Roth accounts are tax-free.2veSave as much as possible in tax-advantaged accounts. If you’re forced to retire earlier than planned, your work-sponsored retirement plans, IRAs, and health savings accounts (HSAs) could become critical resources. HSA assets can be used tax-free to pay for qualified medical expenses at any time, and you can generally tap your retirement plan and IRA assets after age 59½ without penalty. Although ordinary income taxes apply to distributions from pre-tax accounts, qualified withdrawals from Roth accounts are tax-free.2

In addition, the IRS has identified several situations in which retirement account holders may be able to take penalty-free early withdrawals. These include disability, terminal illness, leaving an employer after age 55 (work-based plans only),3 to pay for unreimbursed medical expenses that exceed 7.5% of your adjusted gross income, and to pay for health insurance premiums after a job loss (IRAs only).

Pay down debt. Generally, it’s wise to enter retirement (especially when unexpected) with as little debt as possible. Ensuring that your financial plan includes a strategy for paying down student loans, credit card debt, auto loans, and mortgages can help you minimize your income needs later in life.

Know your bare-bones budget. Another way to help cushion the shock of an unexpected early retirement is knowing exactly how much you spend each month on your basic necessities, including housing, food, utilities, transportation, and health care. Maintaining a written budget throughout life’s ups and downs will help you quickly identify how much income you’d need over the short term while you work on a longer-term income-replacement strategy.

Maintain adequate levels of disability insurance. Your employer may offer group coverage at reduced rates; however, you lose those benefits if your employment is terminated. Private disability income insurance can help you secure coverage specific to your needs, and since the premiums are typically paid with after-tax dollars, any benefits would generally be tax-free (unlike work-sponsored coverage that is paid with pre-tax dollars).

Understand Social Security benefits. If you stop working due to disability, you may qualify for Social Security Disability Insurance benefits if you meet certain requirements. You must have earned a certain number of work credits in a job covered by Social Security and have a physical or mental impairment that has lasted or is expected to last at least 12 months or result in death. If you remain eligible, benefits may continue up to age 65 and then convert to Social Security retirement benefits.

If you need to retire earlier than planned for reasons unrelated to disability and are eligible for Social Security retirement benefits, you can apply as early as age 62. However, starting payments prior to your full retirement age (66 or 67, depending on year of birth) will result in a permanently reduced monthly benefit.

For more information on Social Security disability and retirement benefits, visit the Social Security Administration’s website at ssa.gov.

Consider your health insurance options. Terminating employment prior to age 65 could leave you without health insurance. You may opt to continue your employer-sponsored health coverage for a limited period (permitted through COBRA, the Consolidated Omnibus Reconciliation Act), although this can be quite expensive. If you’re married and your spouse works, you may get coverage under their plan. You may also seek coverage through the federal or a state-based health insurance marketplace. If you receive Social Security disability benefits, you’d automatically qualify for Medicare after 24 months.

Don’t be caught off guard

Don’t wait for an unwelcome surprise. Take steps now to help ensure your overall financial plan considers the “what-if” of an unexpected early retirement.

1) Employee Benefit Research Institute, 2024

2) Qualified Roth withdrawals are those made after a five-year holding period and after the account owner dies, becomes disabled, or reaches age 59½. The penalty for early retirement account distributions and nonqualified withdrawals from Roth accounts is 10%. Nonqualified withdrawals from HSAs will be subject to ordinary income tax and a 20% penalty. After age 65, individuals can take money out of HSAs penalty-free, but regular income taxes will apply to funds not used for qualified medical purposes.

3) Age 50 or after 25 years of service for public safety officers

Why 49% of Retirees Earlier Than Planned

Source: Employee Benefit Research Institute, 2024

Home Energy Rebates Could Save You Money

The Inflation Reduction Act of 2022 included two provisions allowing rebates for home energy efficiency retrofit projects and home electrification and appliance projects. These home energy rebate programs are to be administered by state energy offices, with the U.S. Department of Energy (DOE) providing guidance and oversight.

Many states have applied for or have received optional early funding to jumpstart their home energy rebate programs. Rebates are available in some states starting in 2024 (possibly delayed until 2025 for others). The DOE tracks the application progress of states on energy.gov.

What are the DOE home energy rebates?

There are two DOE home energy rebates and various factors help determine the amount of rebates that may be available.

For a home energy efficiency retrofit project with at least 20% predicted energy savings, a rebate may be available per household for 80% of project costs, up to $4,000 (reduced to 50% of project costs, up to $2,000, if household income is above 80% of area median income (AMI)). For a home energy efficiency retrofit project with at least 35% predicted energy savings, a rebate may be available per household for 80% of project costs, up to $8,000 (reduced to 50% of project costs, up to $4,000, if household income is above 80% of AMI).

For a home electrification and appliance project, a rebate may be available per household for 100% of project costs, up to specific technology cost maximums, with a maximum total of $14,000. The 100% of project costs limit is reduced to 50% if household income is above 80% of AMI. This rebate is not available if household income is above 150% of AMI. The specific technology cost maximums range from $840 for an Energy Star electric stove to $8,000 for an Energy Star electric heat pump for space heating and cooling.

An installed technology may be eligible for rebates either because of its predicted energy savings or because of its inclusion on the home electrification project qualified technologies list, but not for both reasons in a single household.

Tax treatment of DOE home energy rebates

A rebate paid to or on behalf of a purchaser participating in either of the DOE home energy rebate programs is not includible in the purchaser’s gross income and will be treated as a purchase price adjustment. This means that to the extent the rebate is provided at the time of sale, the rebate is not included in the purchaser’s cost (or tax) basis in the property. If the rebate is provided later, the tax basis is reduced.

Payments of rebate amounts made directly to a business taxpayer, such as a contractor, in connection with the business taxpayer’s sale of goods or provision of services to a purchaser are includible in the business taxpayer’s income.

Coordination with the energy efficient home improvement credit

In some cases, a taxpayer can receive an energy efficient home improvement credit for federal income tax purposes. The credit is for 30% of amounts paid for certain qualified expenditures, with limits on the allowable annual credit and on the amount of credit for certain types of qualified expenditures. The maximum annual credit amount may be up to $3,200.

If the taxpayer receives a DOE home energy rebate (whether at the time of sale or later), the amount of qualified expenditures used to calculate the energy efficient home improvement credit must be reduced by the amount of the rebate. If the taxpayer purchases items eligible for both the DOE home energy rebate and the energy efficient home improvement credit, the taxpayer can make a pro rata allocation of amounts received as rebates to the individually itemized expenditures as a share of total project cost in determining the amounts treated as paid or incurred for such items for purpose of the credit. The allocated rebate amounts reduce the qualified expenditures to which they are allocated, and the various limits on costs under the energy efficient home improvement credit are then applied.

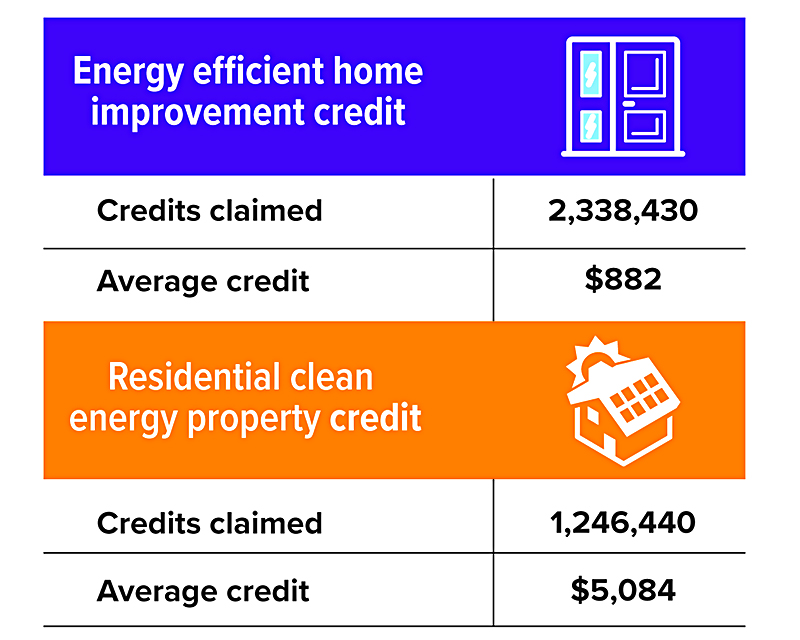

Popular Home Energy Tax Credits

Source: IRS, 2024 (2023 tax return data)

Three Ways to Invest in Yourself

The end of the year is a good time to reflect on everything you’ve accomplished and given to others. As you set resolutions for the new year, why not think about how investing in yourself might give you a fresh start?

Investing in yourself means focusing on your personal growth and well-being. By fostering a stronger “you,” you might be in a better position to give your time and energy to other people and things, including your financial goals, which require discipline, perseverance, and often sacrifice to maintain a robust savings effort month after month.

Here are three areas you might target.

Your health and well-being

Staying active is critical to maintaining good physical and mental health, and it might make it easier for you to tackle all the tasks, financial and otherwise, on your plate each day. Feeling sluggish, stressed, or sore? Having trouble sleeping? To get on a better health track, consider joining a gym, working with a personal trainer or nutritionist, taking a fitness class, experimenting with a wearable fitness tracker, or buying home exercise equipment. Or you might invest in an ergonomic office chair, a stand-up work desk, or a new bed and pillows.

What about your diet? To take your eating habits to the next level, consider investing in some new kitchen equipment and/or appliances; signing up for a food delivery service that sends ingredients for healthy meals right to your door; or trying new cookbooks and recipes to discover dishes you enjoy.

Could you use more peace and quiet in a 24/7 world? To enhance your inner solitude, you might invest in a cozy chair, small desk, greenery, soft lighting, and assorted furnishings to create a quiet spot for reading, reflection, or meditation.

Your lifelong learning

The world is a big place, and there is so much to see and do. Trying something new outside your normal routine or comfort zone can provide inspiration and a fresh perspective. Possibilities include traveling to a new destination, investing in new equipment for outdoor recreation, enrolling in an adult education class, or getting involved in a new project or hobby.

Your everyday life

Still wearing clothes, eyeglasses, or a hairstyle from your younger days? Trying to get by using an older laptop, phone, or printer? It might be time to update your wardrobe, look, or tech gadgets.

By investing in yourself today, not only might you feel better now, but you might reap future benefits, too, in the form of potentially lower health-care costs, a wider social circle, expanded hobbies and experiences, and a new perspective on life.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.