EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

What's Causing the Consumer Blues?

Each month, researchers at the University of Michigan interview hundreds of consumers about their opinions on current economic conditions, as well as their personal finances, buying intentions, and expectations for the future. Survey results are captured in the Index of Consumer Sentiment, which is a closely watched economic indicator because household spending accounts for about two-thirds of U.S. gross domestic product.

Despite a strong labor market, the index fell to an all-time low in June 2022, before starting to improve in the third quarter. High inflation, the specter of rising interest rates, and stock market declines are some of the reasons consumers have felt pessimistic about their economic prospects.

Source: University of Michigan, 2022 (data from January 1978 through September 2022)

Three Stretch IRA Alternatives

The passage of the SECURE Act in 2019 effectively eliminated the stretch IRA, an estate planning strategy that allowed an inherited IRA to continue growing tax deferred, potentially for decades. Most nonspouse beneficiaries, including children and grandchildren, can no longer stretch distributions over their lifetimes. Moreover, proposed IRS regulations require most designated beneficiaries to take annual required minimum distributions (RMDs) within the 10-year distribution period if the original account owner died on or after his or her required beginning date. This shorter distribution period could result in unanticipated and potentially large tax bills for nonspouse beneficiaries who inherit high-value IRAs.

You may be looking for alternative ways to preserve your wealth and pass it on to your beneficiaries. Here are three options you might consider.

Roth Conversion

If you are willing to pay income taxes now instead of your beneficiaries paying them later, you could convert your IRA to a Roth IRA. Anyone can convert a traditional IRA to a Roth IRA. However, you generally have to include the amount you convert in your gross income for the year converted. Not only would you have to pay taxes on the amount converted, but the beneficiaries of your Roth IRA will generally have to liquidate the account within 10 years of inheriting it, although they won’t pay federal income taxes on the distribution(s).

Life Insurance

You could take distributions from your IRA and use them to buy life insurance on your life. The beneficiaries you name in the life insurance policy will receive those proceeds tax-free at your death. The policy beneficiaries could use the tax-free proceeds of the life insurance to pay any income taxes they would owe on the balance of the IRA they inherit from you. Or, if you’ve been able to liquidate or spend down your IRA during your lifetime, the tax-free life insurance death benefit would replace some or all of the taxable IRA that otherwise would have been inherited by the beneficiaries.

Irrevocable Trust

You could create an irrevocable trust and fund it with non-IRA assets. An irrevocable trust can’t be changed or dissolved once it has been created. You generally can’t remove assets, change beneficiaries, or rewrite any of the terms of the trust. Often, life insurance is used to fund the irrevocable trust. You can direct how and when the trust beneficiaries are to receive the life insurance proceeds from the trust after your death. In addition, if you have given up control of the property, all of the property in the trust, plus any future appreciation on the property, is removed from your taxable estate.

While trusts offer numerous advantages, they incur upfront costs and often have ongoing administrative fees. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional and your legal and tax professionals before implementing such strategies.

As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. In addition, if a policy is surrendered prematurely there may be surrender charges and income tax implications. Any guarantees are subject to the financial strength and claims-paying ability of the insurer.

To qualify for the tax-free and penalty-free withdrawal of earnings, a Roth IRA must meet the five-year holding requirement, and the distribution must take place after age 59½ or due to the owner’s death, disability, or a first-time home purchase ($10,000 lifetime maximum). Under current tax law, if all conditions are met, the Roth IRA will incur no further income tax liability for the rest of the owner’s lifetime or for the lifetimes of the owner’s heirs, regardless of how much growth the account experiences.

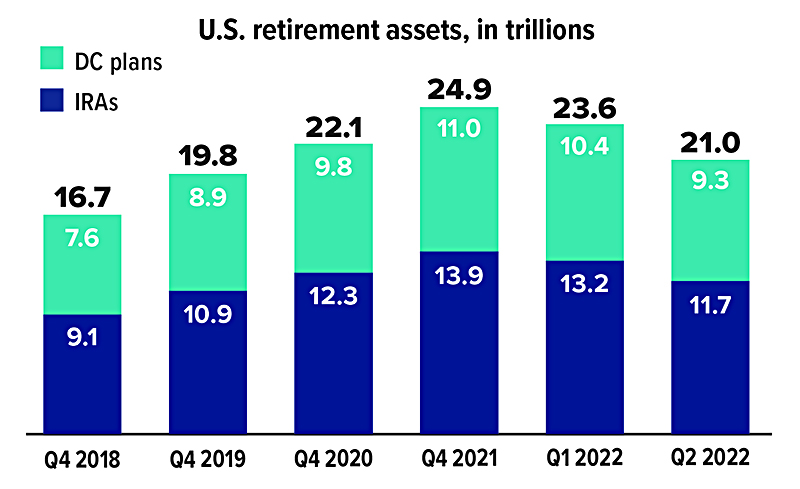

Wealth Cache

Assests held in individual retirement accounts (IRAs) and defined-contribution plans such as 401(k) dipped in the first half of 2022 to $21 trillion. Even so, that total was up more than 25% from year-end 2018.

Source: Investment Company Institute, 2022

When Should Young Adults Start Investing for Retirement?

As young adults embark on their first real job, get married, or start a family, retirement might be the last thing on their minds. Even so, they might want to make it a financial priority. In preparing for retirement, the best time to start investing is now — for two key reasons: compounding and tax management.

Power of Compound Returns

A quick Internet search reveals that Albert Einstein once called compounding “the most powerful force in the universe,” “the eighth wonder of the world,” or “the greatest invention in human history.” Although the validity of these quotes is debatable, Einstein would not have been far off in his assessments.

Compounding happens when returns earned on investments are reinvested in the account and earn returns themselves. Over time, the process can gain significant momentum.

For example, say an investor put $1,000 in an investment that earns 5%, or $50, in year one, which gets reinvested, bringing the total to $1,050. In year two, that money earns another 5%, or $52.50, resulting in a total of $1,102.50. Year three brings another 5%, or $55.13, totaling $1,157.63. Each year, the earnings grow a little bit more.

Over the long term, the results can snowball. Consider the examples in the accompanying chart.

Tax Management

Another reason to start investing for retirement now is to benefit from tax-advantaged workplace retirement plans and IRAs.

Lower taxes now. Contributions to traditional 401(k)s and similar plans are deducted from a paycheck before taxes, so contributing can result in a lower current tax bill. And depending on a taxpayer’s income, filing status, and coverage by a workplace plan, contributions to a traditional IRA may result in an income tax deduction.

Tax-deferred compounding. IRAs and workplace plans like 401(k)s compound on a tax-deferred basis, which means investors don’t have to pay taxes on contributions and earnings until they withdraw the money. This helps drive compounding potential through the years.

Future tax-free income. Roth contributions to both workplace accounts and IRAs offer no immediate tax benefit, but earnings grow on a tax-deferred basis, and qualified distributions are tax-free. A qualified distribution is one made after the Roth account has been held for five years and the account holder reaches age 59½, dies, or becomes disabled.

Saver’s Credit. In 2022, single taxpayers with adjusted gross incomes of up to $34,000 ($66,000 if married filing jointly) may qualify for an income tax credit of up to $1,000 ($2,000 for married couples) for eligible retirement account contributions. Unlike a deduction — which helps reduce the amount of income subject to taxes — a credit is applied directly to the amount of taxes owed.

Avoiding penalties. Keep in mind that withdrawals from pre-tax retirement accounts prior to age 59½ and nonqualified withdrawals from Roth accounts are subject to a 10% penalty on top of regular income tax.

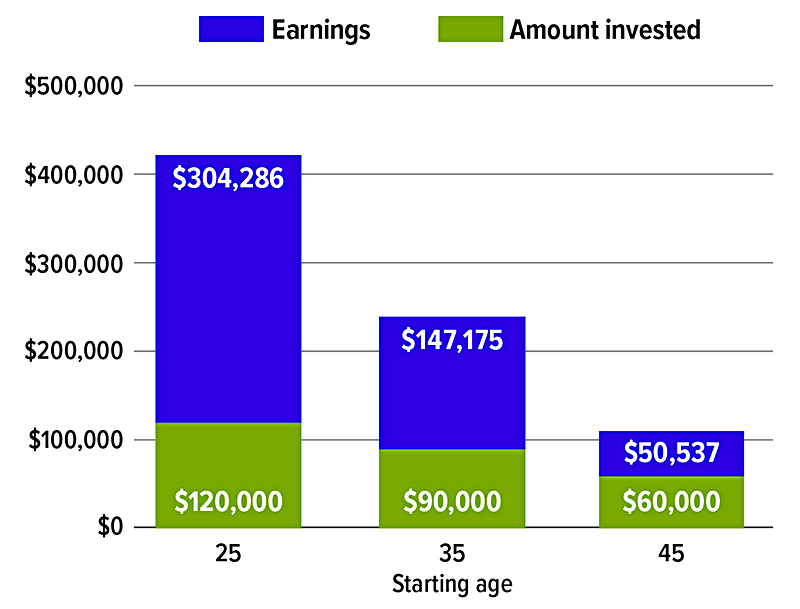

A Head Start Can Be a Strong Ally

This chart illustrates how much an investor could accumulate by age 65 by investing $3,000 a year starting at age 25, 35, and 45 and earning a 6% annual rate of return, compounded annually.

These hypothetical examples of mathematical compounding are used for illustrative purposes only and do not reflect the performance of any specific investments. Fees, expenses, and taxes are not considered and would reduce the performance shown if they were included. Rates of return will vary over time, particularly for long-term investments. Investments offering the potential for higher rates of return also involve a higher degree of investment. Actual results will vary.

Additional Fuel for the Fire

Workplace plans that offer employer matching or profit-sharing contributions can further fuel the tax-advantaged compounding potential. Investors would be wise to consider taking full advantage of employer matching contributions, if offered.

Don’t Delay

With the power of compounding and the many tax advantages, it may make sense to make retirement investing a high priority at any age.

Tips for Safe Online Shopping

According to the National Retail Federation, online sales accounted for over $1 trillion of total U.S. retail sales in 2021.1 Online shopping is especially popular during the holiday season, enabling you to avoid the crowds and conveniently purchase gifts using your smartphone or computer. Unfortunately, the popularity of online shopping also means that cyber criminals and online scams are more prevalent than ever. Here are some tips to help protect yourself when shopping online.

Check your device. Make sure that all of your devices (e.g., mobile phone, computer, and tablet) are up-to-date and configured to update automatically or notify you when updates are available.

Maintain strong passwords. Create strong passwords, at least 8 characters long, using a combination of lower- and upper-case letters, numbers, and symbols, and don’t use the same password for multiple accounts.

Use multi-factor authentication when available. Two-factor or multi-factor authentication, which involves using a one-time code sent to your mobile device in addition to your password, provides an extra layer of protection.

Watch out for phishing emails. Beware of emails that contain links or ask for personal information. Legitimate shopping websites will never email you and randomly ask for your personal information. In addition, don’t be fooled by fake package delivery updates. Make sure that all delivery emails are from reputable delivery companies you recognize.

Beware of scam websites. Typing one word into a search engine to reach a particular retailer’s website may be easy, but it might not take you to the site you are actually looking for. Scam websites often contain URLs that look like misspelled brand or store names to trick online shoppers. To help determine whether an online retailer is reputable, research sites before you shop and read reviews from previous customers. Look for https:// in the URL and not just http://, since the “s” indicates a secure connection.

Use credit instead of debit. Credit cards generally have better protection than debit cards against fraudulent charges. In addition, consider using a mobile payment service (e.g., Apple Pay or Google Pay), which doesn’t require you to give your credit-card information directly to a merchant.

1) National Retail Federation, 2022

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Prepared by Broadridge Advisor Solutions Copyright 2022.