EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

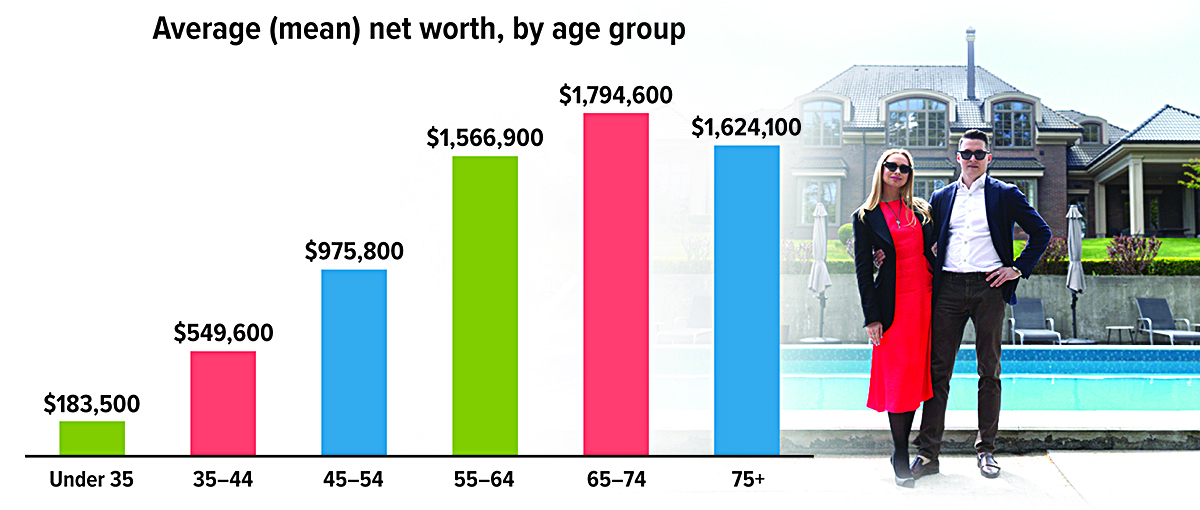

Just Your Average Millionaire

The average net worth of U.S. families surpassed $1 million ($1,063,700) for the first time in 2022, after increasing 23% from 2019. (A family’s net worth is the total of their financial assets minus their liabilities, or debts.) Unfortunately, this milestone does not mean the typical American is a millionaire, because a small number of very wealthy households skews the average. The median net worth ($192,900 in 2022) was much lower than the average, but its growth was by far the largest on record. Still, the net worth of U.S. families varies greatly depending on housing status, education, income level, and age — which shows that it usually takes time and diligence to build wealth.

Source: Federal Reserve, 2023

It's Complicated: Inheriting IRAs and Retirement Plans

The SECURE Act of 2019 dramatically changed the rules governing how IRA and retirement plan assets are distributed to beneficiaries. The new rules, which took effect for account owner deaths occurring in 2020 or later, are an alphabet soup of complicated requirements that could result in big tax bills for many beneficiaries.

RMDs and RBDs

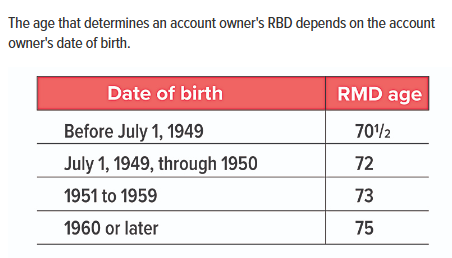

IRA owners and, in most cases, retirement plan participants must start taking annual required minimum distributions (RMDs) from their non-Roth accounts by April 1 following the year in which they reach RMD age (see table). This is known as their required beginning date (RBD).

Likewise, beneficiaries must take RMDs from inherited accounts (including, in most cases, Roth accounts). The timing and amount of an individual beneficiary’s RMDs depend on several factors, including the relationship of the beneficiary to the original account owner and whether the original owner had reached the RBD.

Three key points apply to both owners and beneficiaries: (1) individuals must pay income taxes on the taxable portion of any distribution, (2) the larger the RMD, the higher the potential tax burden, and (3) failing to take the required amount generally results in an additional excise tax.1

Spouse as sole beneficiary

Spouses who are sole beneficiaries have the most options for managing inherited accounts. By default, a surviving spouse beneficiary is treated as what’s known as an eligible designated beneficiary (EDB) with certain advantages (see next section, “EDBs and DBs”). And if the deceased spouse died before the RBD, a surviving spouse EDB who is the sole owner can wait until the year the deceased would have reached RMD age to begin distributions.

Alternatively, a surviving spouse who is the sole owner can generally roll over the inherited account to their own account or elect to be treated as the account owner (rather than as an EDB). In these cases, the rules for account owners would apply. However, there is a potential drawback to this move: if the surviving spouse is younger than 59½, a 10% early distribution penalty may apply to subsequent withdrawals unless an exception applies.

EDBs and DBs

The SECURE Act separated other individual beneficiaries into two groups: EDBs and designated beneficiaries (DBs). EDBs are spouses and minor children of the deceased, those who are not more than 10 years younger than the deceased, and disabled and chronically ill individuals. DBs are essentially everyone else, including adult children and grandchildren.

EDBs have certain advantages over DBs. If the account owner dies before the RBD, an EDB is able to spread distributions over their own life expectancy. If the account owner dies on or after the RBD, an EDB may spread distributions over either their own life expectancy or that of the original account owner, whichever is more beneficial.2

By contrast, DBs are required to liquidate inherited assets within 10 years, which could result in unanticipated and hefty tax bills. If the account owner dies before the RBD, the beneficiary can leave the account intact until year 10. If the owner dies on or after the RBD, a DB must generally take annual RMDs based on their own life expectancy in years one through nine, then liquidate the account in year 10.

Other considerations

Work-sponsored retirement plans are not required to offer all distribution options; for example, an EDB may be required to follow the 10-year rule. However, both EDBs and DBs may roll eligible retirement plan assets into an inherited IRA, which may offer more options for managing RMDs.

This is just a broad overview of the complicated new rules as they apply to individual beneficiaries. If an account has multiple designated beneficiaries, or if a beneficiary is an entity such as a trust, charity, or estate, other rules apply. Beneficiaries should seek the assistance of an estate-planning attorney before making any decisions.

1) The IRS has waived this tax as it applies to the DB 10-year rule through 2024.

2) An inherited account must be liquidated 10 years after an EDB dies or a minor child EDB reaches age 21.

Thinking of Selling Your Home? Don't Be Surprised by Capital Gains Taxes

The Taxpayer Relief Act of 1997 provided homeowners who sell their principal residence an exclusion from capital gains taxes of $250,000 for single filers and $500,000 for joint filers. At that time, the average price of a new home was about $145,000, so this exclusion seemed generous and allowed more Americans to move freely from one home to another.1 Unfortunately, the exclusion was not indexed to inflation, and what seemed generous in 1997 can be restrictive in 2024.

Capital gains taxes apply to the profit from selling a home, so they may be of special concern — and potential surprise — for older homeowners who bought their homes many years ago and might yield well over $500,000 in profits if they sell. In some areas of the country, a home bought for $100,000 in the 1980s could sell for $1 million or more today.2 At a federal tax rate of 15% or 20% (depending on income) plus state taxes in some states, capital gains taxes can take a big bite out of profits when selling a home. Fortunately, there are some things you can do to help reduce the taxes.

Qualifying for exclusion

In order to qualify for the full exclusion, you or your spouse must own the home for at least two years during the five-year period prior to the home sale. You AND your spouse (if filing jointly) must live in the home for at least two years during the same period. The exclusion can only be claimed once every two years. There are a number of exceptions, including rules related to divorce, death, and military service. If you do not qualify for the full exclusion, you may qualify for a partial exclusion if the main reason for the home sale was a change in workplace location, a health issue, or an unforeseeable event.

Increasing basis for lower taxes

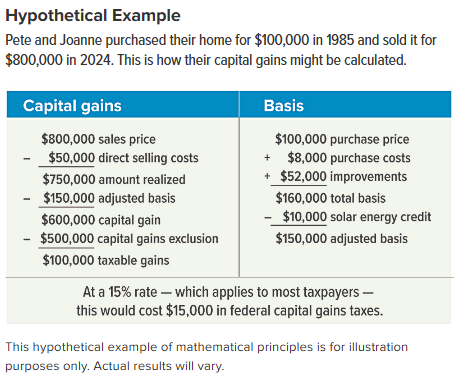

The capital gain (or loss) in selling a home is determined through a two-part calculation. First, the selling price is reduced by direct selling costs, including certain fees and closing costs, real estate commissions, and certain costs that the seller pays for the buyer. (The amount of any mortgage pay-off is not relevant for determining capital gains.) This yields the amount realized, which is then reduced by the adjusted basis.

The basis of your home is the amount you paid for it, including certain costs related to the purchase, plus the costs of improvements that are still part of your home at the date of sale. In general, qualified improvements include new construction or remodeling, such as a room addition or major kitchen remodel, as well as repair-type work that is done as part of a larger project. For example, replacing a broken window would not increase your basis, but replacing the window as part of a project that includes replacing all windows in your house would be eligible. This basis is adjusted by adding certain payments, deductions, and credits such as tax deductions and insurance payments for casualty losses, tax credits for energy improvements, and depreciation for business use of the home. (See hypothetical example.)

Inheriting a home

Upon the death of a homeowner, the basis of the home is stepped up (increased) to the value at the time of death, which means that the heirs will only be liable for future gains. In community property states, this usually also applies to a surviving spouse. In other states, the basis for the surviving spouse is typically increased by half the value at the time of death (i.e., the value of the deceased spouse’s share).

Determining the capital gain on a home sale is complex, so be sure to consult your tax professional. For more information, see IRS Publication 523 Selling Your Home.

1) U.S. Census Bureau, retrieved from FRED, Federal Reserve Bank of St. Louis, 2024

2) CNN, January 29, 2024

The IRS Wants More Info About Your Gig Income

If you earn money through a payment app or online marketplace, you may be affected by a tax reporting change enacted by the 2021 American Rescue Plan. The law requires third-party settlement organizations to report business transactions totaling over $600 per year by issuing a Form 1099-K to the taxpayer and the IRS. The previous reporting threshold was much higher ($20,000 and 200 business transactions).

This change was delayed for the 2023 tax year because it could trigger frustrating unintended consequences. According to the Internal Revenue Service, an estimated 44 million taxpayers might have received unexpected 1099-K forms — with amounts that may not have been taxable. To provide more lead time, the agency announced plans to drop the threshold from $20,000 to $5,000 in 2024 (without regard to the total number of transactions) as part of a phase-in of the $600 threshold.

Here are a few more things that may be helpful to know about this far-reaching new rule.

It’s not personal. Business transactions are payments for goods or services, including tips. Money received from the online sale of personal items (like old clothing or furniture), which are normally sold at a loss, is not taxable and generally doesn’t need to be reported. However, those in the business of reselling goods for a profit should carefully track the original costs of their purchases. Payment apps are not required to report personal transactions intended as gifts or to split costs. The payer will typically be asked to note nonbusiness transactions.

It’s not a tax change. Taxpayers who sell goods, rent out a vacation home, walk dogs, or perform any other type of freelance work through digital platforms were already responsible for self-reporting all income on their tax returns regardless of the threshold. But now the IRS can cross-reference the information sent by third parties with the reported amounts.

It’s not foolproof. This change could still cause confusion and costly mistakes. If a payer (such as a roommate making a shared rent payment) accidently clicks on the wrong box, the recipient could receive a Form 1099-K in error. A freelancer might receive a Form 1099-K from the payment processor and a Form 1099-MISC from the client for the same transaction. In such cases, the taxpayer may need to contact the issuer, and if a discrepancy is not corrected, the reported amount can be adjusted with a notation on the tax return.

Using separate accounts for business and personal digital transactions and keeping organized records will help ensure that your tax return is accurate, so you don’t overpay or raise red flags with the IRS. If you have questions about how the new rule might affect you, don’t hesitate to consult a qualified tax professional.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.