EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

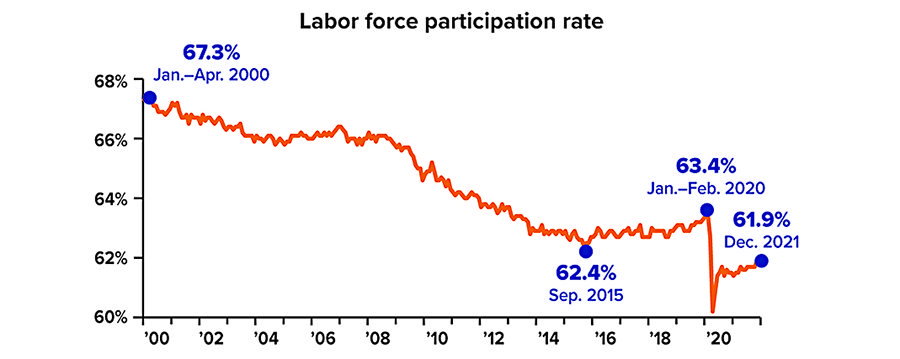

Where are the workers?

The labor force participation rate — the percentage of Americans age 16 and older who are working or actively looking for work — peaked in early 2000, when it began to drop due to aging baby boomers and more young people in college. Participation was rising before plummeting at the onset of the pandemic.

The rate has only partially recovered due in large part to accelerated retirement among workers age 55 and older. Other reasons include fewer child-care workers, reduced immigration, and many workers unwilling to return to low-paying jobs. Some experts believe it may never return to pre-pandemic levels. The question for the U.S. economy is whether technology and other productivity measures can maintain economic growth with a smaller percentage of the population in the workforce.

Sources: U.S. Bureau of Labor Statistics, 2016 & 2022; The Wall Street Journal, October 14, 2021; CNN, December 15, 2021

Working While Receiving Social Security Benefits

The COVID-19 recession and the continuing pandemic pushed many older workers into retirement earlier than they had anticipated. A little more than 50% of Americans age 55 and older said they were retired in Q3 2021, up from about 48% two years earlier, before the pandemic.1

For people age 62 and older, retiring from the workforce often means claiming Social Security benefits. But what happens if you decide to go back to work? With the job market heating up, there are opportunities for people of all ages to return to the workforce. Or to look at it another way: What happens if you are working and want to claim Social Security benefits while staying on your job?

Retirement Earnings Test

Some people may think they can’t work — or shouldn’t work — while collecting Social Security benefits. But that’s not the case. However, it’s important to understand how the retirement earnings test (RET) could affect your benefits.

- The RET applies only if you are working and receiving Social Security benefits before reaching full retirement age (FRA). Any earnings after reaching full retirement age do not affect your Social Security benefit. Your FRA is based on your birth year: age 66 if born in 1943 to 1954; age 66 & 2 months to 66 & 10 months if born in 1955 to 1959; age 67 if born in 1960 or later.

- If you are under full retirement age for the entire year in which you work, $1 in benefits will be deducted for every $2 in gross wages or net self-employment income above the annual exempt amount ($19,560 in 2022). The RET does not apply to income from investments, pensions, or retirement accounts.

- A monthly limit applies during the year you file for benefits ($1,630 in 2022), unless you are self-employed and work more than 45 hours per month in your business (15 hours in a highly skilled business). For example, if you file for benefits starting in July, you could earn more than the annual limit from January to June and still receive full benefits if you do not earn more than the monthly limit from July through December.

- In the year you reach full retirement age, the reduction in benefits is $1 for every $3 earned above a higher annual exempt amount ($51,960 in 2022 or $4,330 per month if the monthly limit applies). Starting in the month you reach full retirement age, there is no limit on earnings or reduction in benefits.

- The Social Security Administration may withhold benefits as soon as it determines that your earnings are on track to surpass the exempt amount. The estimated amount will typically be deducted from your monthly benefit in full. (See example.)

- The RET also applies to spousal, dependent, and survivor benefits if the spouse, dependent, or survivor works before full retirement age. Regardless of a spouse’s or dependent’s age, the RET may reduce a spousal or dependent benefit that is based on the benefit of a worker who is subject to the RET.

The RET might seem like a stiff penalty, but the deducted benefits are not really lost. Your Social Security benefit amount is recalculated after you reach full retirement age. For example, if you claimed benefits at age 62 and forfeited the equivalent of 12 months’ worth of benefits by the time you reached full retirement age, your benefit would be recalculated as if you had claimed it at age 63 instead of 62. You would receive this higher benefit for the rest of your life, so you could end up receiving substantially more than the amount that was withheld. There is no adjustment for lost spousal benefits or for lost survivor benefits that are based on having a dependent child.

If you regret taking your Social Security benefit before reaching full retirement age, you can apply to withdraw benefits within 12 months of the original claim. You must repay all benefits received on your claim, including any spousal or dependent benefits. This option is available only once in your lifetime.

1) Pew Research Center, November 4, 2021

In this hypothetical example, Fred claimed Social Security in 2021 at age 62, and he was entitled to a $1,500 monthly benefit as of January 2022. Fred returned to work in April 2022 and is on track to earn $31,560 for the year–$12,000 above the $19,560 RET exempt amount. Thus, $6,000 ($1 for every $2 above the exempt amount) in benefits will be deducted. Assuming that the Social Security Administration (SSA) became aware of Fred’s expected earnings before he returned to work, benefits might be paid as illustrated below.

In practice, benefits may be withheld earlier in the year or retroactively, depending on when SSA becomes aware of earnings.

Baseball Lessons That Might Help Change Up Your Finances

Baseball stadiums are filled with optimists. Fans start each new season with the hope that even if last year ended badly, this year could finally be the year. After all, teams rally mid-season, curses are broken, and even underdogs sometimes make it to the World Series. As Yogi Berra famously put it, “It ain’t over till it’s over.”1 Here are a few lessons from America’s pastime that might inspire you to take a fresh look at your finances.

Proceed One Base at a Time

There’s nothing like seeing a home run light up the scoreboard, but games are often won by singles and doubles that put runners in scoring position through a series of hits. The one-base-at-a-time approach takes discipline, something you can apply to your finances. What are your financial goals? Do you know how much money comes in and how much goes out? Are you saving regularly for retirement or for a child’s college education? Answering some fundamental questions will help you understand where you are now and help you decide where you want to go.

Cover Your Bases

Baseball players must be positioned and prepared to make a play at the base. What can you do to help protect your financial future in case life throws you a curveball? Try to prepare for those “what ifs.” For example, you could buy the insurance coverage you need to help make sure your family is protected. And you could set up an emergency account that you can tap instead of dipping into your retirement funds or using a credit card when an unexpected expense arises.

Expect to Strike Out

Fans may have trouble seeing strikeouts in a positive light, but every baseball player knows that striking out is a big part of the game. In fact, striking out is much more common than getting hits. The record for the highest career batting average record is .366, held by Ty Cobb.2 As Ted Williams once said, “Baseball is the only field of endeavor where a man can succeed three times out of ten and be considered a good performer.”3

So how does this apply to your finances? As Hank Aaron put it, “Failure is a part of success.” 4 If you’re prepared for the misses as well as the hits, you can avoid reacting emotionally rather than rationally when things don’t work out according to plan. For example, when investing, you have no control over how the market is going to perform, but you can decide what to invest in and when to buy and sell, according to your investment goals and tolerance for risk. In the words of longtime baseball fan Warren Buffett, “What’s nice about investing is you don’t have to swing at every pitch.”5

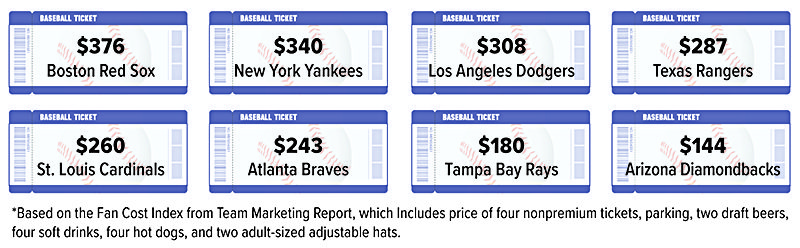

Take me to the Ball game

The average cost of taking a family of four to a Major League Baseball game during the 2021 season was $253. Costs varied across the league, with Red Sox fans paying the most and Dlamondbacks’ fans paying the least.*

Source: The Athletic, 2021

See Every Day as a New Ball Game

When the trailing team ties the score (often unexpectedly), the announcer shouts, “It’s a whole new ball game!” 6

Whether your investments haven’t performed as expected, or you’ve spent too much money, or you haven’t saved enough, there’s always hope if you’re willing to learn from what you’ve done right and what you’ve done wrong. Hall of Famer Bob Feller may have said it best. “Every day is a new opportunity. You can build on yesterday’s success or put its failures behind and start over again. That’s the way life is, with a new game every day, and that’s the way baseball is.”7

All investing involves risk, including the possible loss of principal. There is no guarantee that any investment strategy will be successful.

1, 3-4, 6-7) BrainyQuote.com

2) ESPN.com

5) quotefancy.com

Raising Money-Smart Teens

As teens look forward to summer activities, especially those that cost money, the next few months might present an ideal opportunity to help them learn about earning, spending, and saving. Here are a few age-based tips.

Younger Teens

In recent years, apps have proliferated to help parents teach tweens and teens basic money management skills. Some money apps allow parents to provide an allowance or pay their children for completing chores by transferring money to companion debit cards. Many offer education on the basics of investing. Others allow children to choose from a selection of charities for donations. Some even allow parents to track when and where debit-card transactions are processed and block specific retailers or types of businesses.

Most apps typically charge either a monthly or an annual fee (although some offer limited services for free), so it’s best to shop around and check reviews.

Older Teens

Many teens get their first real-life work experience during the summer months, presenting a variety of teachable moments.

Review payroll deductions together. A quick review can be an eye-opening education in deductions for federal and state income taxes, and Social Security and Medicare taxes.

Open checking and savings accounts. Many banks allow teens to open a checking account with a parent co-signer. Encouraging teens to have a portion of their earnings automatically transferred to a companion savings account helps them learn the importance of “paying yourself first.” They might even be encouraged to write a small check or two to help cover the expenses they help incur, such as Internet, cell phone, food, gas, or auto insurance.

Consider opening a Roth account. A teen with earned income could be eligible to contribute to a Roth IRA set up by a parent — a great way to introduce the concept of retirement saving. Because Roth contributions are made on an after-tax basis, they can be withdrawn at any time, for any reason.

Roth IRA earnings can be withdrawn free of taxes as long as the distribution is “qualified”; that is, it occurs after a five-year holding period and the account holder reaches age 59½, dies, or becomes disabled. Nonqualified earnings distributions are taxed as ordinary income and subject to a 10% early-withdrawal penalty; however, if the account is held for at least five years, penalty-free distributions can be taken for a first-time home purchase and to help pay for college expenses, which may be helpful in young adulthood. (Regular income taxes will still apply.)

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Prepared by Broadridge Advisor Solutions Copyright 2022.