EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

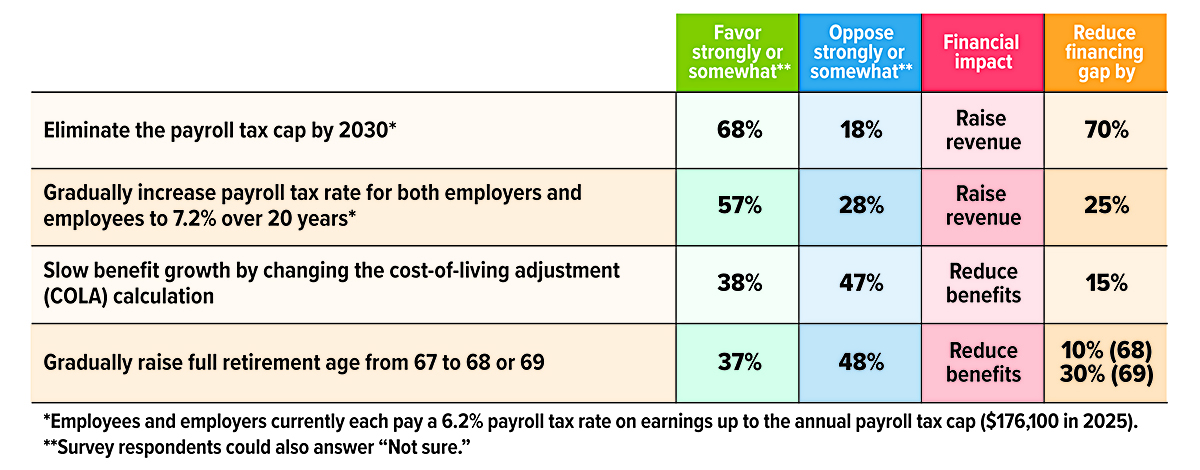

Saving Social Security: Which Solutions Do Americans Support?

According to the 2025 Trustees Report estimates, Social Security will only have sufficient funds to pay full benefits until 2033. After that, payroll tax and other revenues would cover only 81% of benefits. However, this financing gap can be closed if lawmakers act on proposed solutions.

A bipartisan survey found that across party lines, generations, and income and education levels, Americans want lawmakers to strengthen Social Security’s finances by increasing program revenues rather than cutting benefits. When asked about their views, 85% of those surveyed responded that benefits should not be reduced, or benefits should be increased, even if that meant raising taxes on some or all Americans. Here are a few key solutions that respondents weighed in on.

Sources: Social Security Administration, 2025; National Academy of Social Insurance, January 2025

Consider Munis for Tax-Free Income

In 2024, the municipal bond market saw record trading for the third consecutive year. New issues also set a record at $508 billion, the first time muni issues exceeded $500 billion. The trend continued through the first quarter of 2025, with trades and new issues both higher than the first quarter of 2024.1

This increased activity was primarily driven by individual investors attracted to higher yields that coincided with the Federal Reserve raising interest rates to combat inflation.2 Although the Fed has begun to lower rates, they may remain relatively elevated for some time, which could continue to support solid bond yields. Moreover, bonds purchased in a higher rate environment will typically increase in value on the secondary market as interest rates decline. Like other bonds, munis can help steady a portfolio during times of stock market turbulence and provide income regardless of market trends.

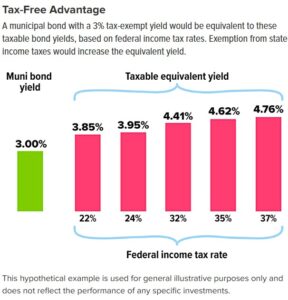

The primary appeal of municipal bonds as opposed to Treasuries or corporate bonds is that the interest is generally exempt from federal income tax, as well as from state or local taxes if you live in the state where the bond was issued. (Treasuries are generally exempt from state taxes but not federal taxes.) The tax-free yield may be higher than the after-tax yield on taxable bonds, especially for investors in higher tax brackets (see chart).

Government borrowing

Munis are debt obligations issued by state and local government entities. They typically fall into one of two categories.

General obligation bonds are issued to raise capital immediately, usually to cover expenses or refinance public debt. They are commonly repaid through taxes levied by the issuing agency.

Revenue bonds are issued to fund specific revenue-generating projects, such as utilities, sports stadiums, redevelopment projects, and toll roads. These bonds are typically repaid from the revenues generated by the finished projects.

Risk, ratings, and funds

Like all bonds, munis are rated for credit risk. A range of AAA down to BBB (or Baa) is considered “investment grade,” and lower-rated or “junk” bonds are considered to carry high risk. Some bonds may also be insured, with a separate credit rating for the insurer. However, bonds should not be purchased based solely on insurance. In general, munis carry more risk than Treasuries but less risk than corporate bonds.

Municipal bond funds spread risk across many individual bonds. Some muni funds focus on bonds from specific states and may also include bonds from U.S. territories that are not subject to state taxes, making the fund’s interest income tax free for investors who live in the targeted state.

The return and principal value of bonds and bond fund shares fluctuate with changes in market conditions. When redeemed, they may be worth more or less than their original cost. Bond funds are subject to the same inflation, interest-rate, and credit risks associated with their underlying bonds. As interest rates rise, bond prices typically fall, which can adversely affect a bond fund’s performance. Conversely, as interest rates fall, bond prices typically rise, which can boost a fund’s performance. Investments offering the potential for higher rates of return involve a higher degree of risk.

U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities fluctuates with market conditions. If not held to maturity, they could be worth more or less than the original amount paid.

Funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

1–2) Municipal Securities Rulemaking Board, January 2025 and April 2025

Navigating Financial Conversations with Aging Parents

Having a conversation with your parents about their finances can seem like a daunting task. However, it is an essential step in helping to ensure their financial well-being as they get older. Here are some practical tips to help you navigate these discussions.

Start the conversation

Talking about money can be difficult. However, it’s important to initiate a financial conversation with your parents before they become too ill or incapacitated. Your parents may be unwilling to talk to you at first because they are reluctant to give up control over their financial affairs, or they are embarrassed to admit that they need your help. It’s important to approach the topic sensitively and make it clear that you fully respect their needs and concerns.

If they are still hesitant to talk to you and are capable of managing their affairs for now, you may want to revisit the discussion later. Or you could suggest that they talk to another family member, trusted friend, attorney, or financial professional.

Organize financial and legal documents

Once the lines of communication are open, you can help your parents organize their financial and legal documents. Start by creating a personal data record that lists the following types of information:

Financial: Include all of your parents’ bank/investment account information, including account/routing numbers and online usernames and passwords. You should also list any real estate holdings, along with any outstanding mortgages. Do your parents receive income from Social Security, a pension, and/or a retirement plan? You will want to include that information as well.

Legal: Find out if your parents have had any legal documents drawn up, such as wills, trusts, durable powers of attorney and/or health-care directives. Locate other important documents too, such as birth certificates, property deeds, and certificates of title.

Medical: Determine what type of health insurance your parents have — Medicare, private insurance, or both. You should also have the names and contact information for their health-care providers, their medical history, and any current medications.

Insurance: List what other types of insurance coverage your parents have — life, home/property, auto, or long-term care, for example — along with the names of their insurance companies and policy numbers.

Store the data record and any other pertinent documents either electronically or in a secure, fireproof box or file cabinet.

Help with managing finances

You can help your parents manage their finances by examining their budget and finding out their monthly income and expenses. Track your parents’ spending to make sure that they are living within their means. You should also discuss ways to address any outstanding debts they may have.

Find out how your parents pay their bills and expenses. If they still use traditional methods, encourage them to set up safer and more convenient ways to bank such as direct deposit and making payments online, instead of mailing paper checks. If your parents are uncomfortable with electronic payments, remind them to mail all bills inside the physical post office and not to use outdoor mailboxes, which may be targets for mail theft.

Do your parents need additional support in managing their finances? There are ways for you to obtain the necessary authorization to assist them. One way is to become a joint account holder on certain bank accounts. This can give you direct access to manage transactions, monitor account activity, and ensure bills are paid. However, being a joint account holder may have certain legal and tax ramifications. Another option is for them to obtain a durable power of attorney, which is a legal document that grants you authorization to make financial decisions on their behalf, even if they become incapacitated. It may also be helpful for them to add you or someone else as a trusted contact for their accounts.

Discuss estate planning issues

If they haven’t already done so, make sure your parents have certain legal documents in place — such as wills and/or trusts — to ensure that their estate planning wishes are followed. In addition, they may need to have a durable power of attorney, health-care proxy, and living will in place so they have someone to manage their money and health-care issues if they become ill/impaired. Issues surrounding the care of an aging parent can be complex. Consider consulting a financial professional and/or elder law attorney who specializes in financial and legal issues that affect older adults.

Home Appliance Economics

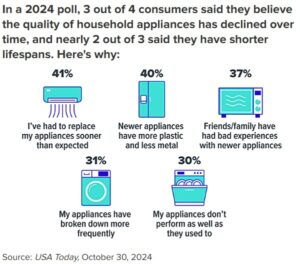

The prices of major home appliances fell 19.5% over the three years between April 2022 and March 2025. They now cost less than they did ten years ago, despite having lots of convenient new features.1 The flip side is that repair costs for today’s complicated appliances have gone through the roof. Plus, many homeowners are convinced appliances are less reliable and don’t last as long.2

Here are three things to consider when an appliance you rely on breaks down.

Should I repair or replace it? If your appliance malfunctions while it is still under the manufacturer’s warranty, the repair may be covered, but you should use a factory-authorized repair shop if you don’t want to risk voiding the warranty. Service calls can cost $100 or more just to bring a tech to the door. If a broken appliance is approaching seven years old, or the cost to repair it will be more than half the price of a new one, replacement is often recommended.3

If I buy a new one, should I pay to extend the warranty? Extended warranties (or service contracts) generally cover service and repairs after the manufacturer’s warranty expires. Ask yourself whether you are more comfortable paying a fixed monthly cost than unexpectedly facing a high repair bill that eats into your emergency fund or ends up on your credit card. Each warranty is different, so read the contract carefully to find out what’s covered and what’s not.

Can I fix it myself? Before you give up on your old appliance, you might search for online repair guides provided by retailers that sell replacement parts and/or do some research on social media. An active community of DIYers may help you diagnose problems, and you will likely find plenty of free videos with step-by-step directions for common repairs.

1) U.S. Bureau of Labor Statistics, 2025; 2)The Wall Street Journal, February 20, 2024; 3) Realtor.com, 2024

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.