EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

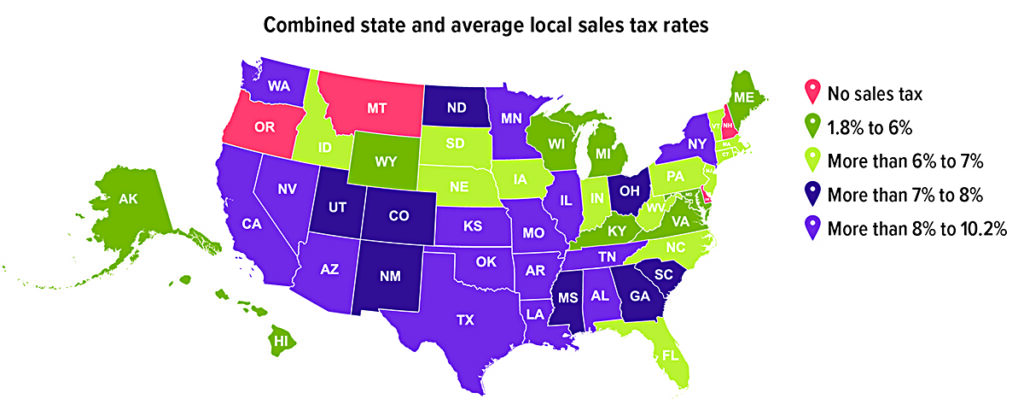

State and Local Sales Tax Across the Map

Among the 46 states (and the District of Columbia) with a state and/or local sales tax, the combined state and average local sales tax rates range from about 1.8% to 10.2%. The sales tax base (defining what is taxable and nontaxable) can also vary greatly. Some states exempt groceries and/or clothing from the sales tax or tax them at a reduced rate. Five states have no statewide sales tax, and of those, only Alaska allows local sales taxes.

Source: Tax Foundation, February 2025

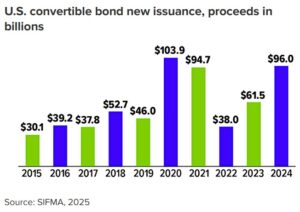

Convertible Bonds Straddle the Line Between Fixed Income and Potential Growth

A convertible bond is a regular corporate bond that comes with a special added feature: the investor has the right to convert it into shares of that company’s common stock.

U.S. convertible bond issuance reached $96.0 billion in 2024, far surpassing the $61.5 billion issued in 2023.1 The strong upward trend that began in 2023 picked up steam in 2024, driven by the resilience of the U.S. economy and interest rates that remained elevated longer than expected.2

Why companies choose convertibles

Convertible bonds tend to offer lower interest rates than ordinary bonds issued by the same company. They also provide a way for companies to raise capital while avoiding the immediate dilution of share values that occurs when new stock is sold.

Convertible bonds have long been utilized by corporations with less than stellar credit ratings, including younger companies and those with weak balance sheets. But with interest rates sitting at high levels, more established, investment-grade companies have also been relying on convertible debt to help lower their borrowing costs.

In addition, a “maturity wall” of more than $1.2 trillion in investment-grade corporate debt is coming due in the next couple of years. Many of these companies could try to save money by refinancing their debt with convertible bonds.3

What’s under the hood for investors

Bond holders will receive income and principal unless the bond issuer defaults. Convertible bonds combine the income and relative price stability of bonds with the opportunity to participate in stock market returns. Thus, their value on the open market is affected not only by interest rates, as all bonds are, but also by changes in the company’s stock price.

The bond agreement spells out either how many shares of stock the bond can be converted into (the conversion ratio), or the stock price at which the conversion can be made (the conversion price). For example, a bond that can be converted into 45 shares of stock would have a conversion ratio of 45:1. A $1,000 bond that has a conversion price of $50 a share would convert to 20 shares of stock.

If the stock’s price rises, the convertible’s price also rises, though convertibles usually are not as volatile as the stock itself. If the stock’s price falls, the convertible’s value on the open market could be less than its face value if sold before it matures, though the fixed interest it pays could help cushion the impact.

Challenges to consider

Most convertibles are callable, usually within five years after they’re issued. If the stock price doesn’t rise before the bond is called, the advantage of being able to convert the bond disappears.

Convertibles can also be relatively illiquid. As a result, individual investors may have difficulty finding buyers and sellers for small lots and end up paying higher prices than institutional investors.

In fact, liquidity is one of several reasons an investor might prefer to access convertibles through a mutual fund or exchange-traded fund (ETF) instead of purchasing individual bonds: the use of funds makes it easier to compare investment performance, and it can also help increase portfolio diversification.

Diversification is a method used to help manage investment risk; it does not guarantee a profit or protect against investment loss. The return and principal value of bonds, stocks, mutual funds, and ETFs fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost. Bond funds are subject to the same inflation, interest-rate, and credit risks associated with their underlying bonds. Supply and demand may cause ETF shares to trade at a premium or discount relative to the value of the underlying shares. Investments seeking to achieve higher yields also involve a higher degree of risk.

Mutual funds are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained from your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

1) SIFMA, 2025

2) London Stock Exchange Group, 2024

3) The Financial Times, January 2, 2024

Will You Pay a Medicare Surcharge?

Medicare is a federal program that provides health insurance to retired individuals, regardless of their medical condition, and certain younger people with disabilities or end-stage renal disease. Medicare has several parts, many of which include a premium cost based on your tax filing status and income. If your income is high, in some cases you may be subject to a premium surcharge called the income-related monthly adjustment amount (IRMAA).

What does Medicare cover?

Medicare coverage consists of two main parts: Medicare Part A (hospital insurance) and Medicare Part B (medical insurance). These parts together are known as Original Medicare. A third part, Medicare Part C (Medicare Advantage), covers all Part A and Part B services and may provide additional services. A fourth part, Medicare Part D, offers prescription drug coverage that can help you handle the rising costs of prescriptions.

What does Medicare cost?

Most people age 65 or older who are citizens or permanent residents of the United States are eligible for Medicare Part A without paying a monthly premium. Although Medicare Part B is optional, most people sign up for it. If you want to join a Medicare Advantage plan, you’ll need to enroll in both Parts A and B. And Medicare Part B is never free — you’ll pay a monthly premium for it, even if you are eligible for premium-free Medicare Part A. If you delay starting Part B or Part D after age 65, you may also be subject to a surcharge unless you continue to work and are covered by a workplace health plan.

The standard Part B premium is $185.00 in 2025. However, premiums for Part B and Part D can vary based on income levels. If your modified adjusted gross income (MAGI) as reported on your federal income tax return from two years ago is above a certain amount, you’ll pay the standard premium plus the IRMAA surcharge. You’ll receive a notice from the Social Security Administration if you’re subject to IRMAA.

What can you do to lower your income?

Most people may see a decline in their income once they retire. However, high-income Medicare recipients may want to lower their income to help reduce the potential premium surcharges. Here are some ideas:

- Put off transactions that could increase income, such as the sale of real estate or stocks.

- Defer distributions from tax-qualified accounts such as IRAs and 401(k)s as long as possible.

- Rethink the timing of converting IRA funds to a Roth IRA to avoid increased taxable income.

Since your income is based on information from two years ago, it may subsequently change, or you may experience a life-changing event (as defined by the SSA) that causes a reduction in your income. Report income changes to the SSA as soon as possible. You’ll need to provide documentation verifying the event and your reduction in income. Visit https://www.ssa.gov/benefits for more information.

Get Help

Navigating Medicare programs and their costs can be tricky. You might consider consulting with an appropriately qualified professional for help.

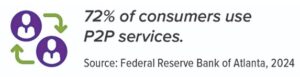

Peer-to-Peer Payments Are Popular, but Be Careful

Making a peer-to-peer (P2P) payment is a convenient way to transfer money to family, friends, or businesses. Whether you’re splitting a bill or paying a babysitter, if you have someone’s contact information, you can send or receive money quickly and easily using a mobile app or an online platform linked to your bank account or credit card.

Most P2P transactions go smoothly, but what happens when something goes wrong? Unauthorized transactions will generally be refunded by the P2P service. But what if you accidentally type an incorrect character in a username and send money to a stranger, or you’re tricked into transferring funds to a scammer? Unfortunately, in either of those situations, because you’ve authorized the transaction, the P2P service or your financial institution is generally not required to reverse it or issue a refund, so your money is likely gone for good.

Take precautions to help avoid costly mistakes

Verify requests, especially if they are unexpected. Scammers may try to persuade you to send money by pretending to be an acquaintance, a bank representative, or a merchant — make sure you really know and trust the person who contacted you.

Double-check information before sending funds. Confirm that the recipient’s contact information is correct, and consider sending a small test payment to make sure that the right person received it. And check the amount you’re sending to help avoid transferring more than you intended.

Use available security features. These include multi-factor authentication, biometrics, and passkeys. Keep your app up to date to ensure you have the latest protection, and never share your credentials or make payments through unsecured networks.

Read terms and conditions. Make sure you understand what fraud protections and policies apply to the P2P service you’re using.

what fraud protections and policies apply to the P2P service you’re using.

Pay attention to permissions. If the app allows social sharing of transactions, check the permissions you’re granting. Periodically review privacy notices and disclosures to make sure your selections match your privacy preferences.

If you do encounter a problem, contact the app’s customer service department and your financial institution; ask them to investigate, and find out what recourse you may have.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.