EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

There are two ways to obtain Medicare coverage: (1) Original Medicare (Part A hospital insurance and Part B medical insurance), often combined with a Medigap supplementary policy and a Part D prescription drug plan; and (2) Medicare Advantage (Part C), which replaces Original Medicare and often includes prescription drug coverage as well as features similar to those provided by a Medigap policy.

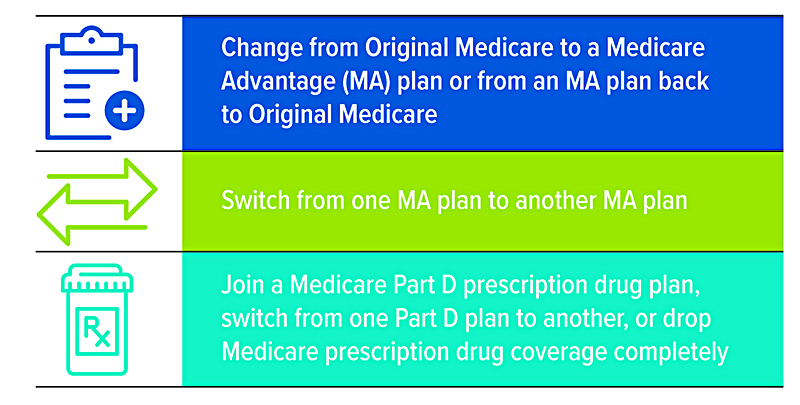

New beneficiaries can choose among these options when they enroll, while current beneficiaries can make changes during the annual Open Enrollment Period from October 15 to December 7 (see chart). Some changes can also be made at other times of the year.

Original Medicare with Medigap and Part D

Original Medicare is administered directly by the federal government and includes standardized premiums, deductibles, copays, and coinsurance payments. While these out-of-pocket costs are relatively moderate for doctor visits, laboratory tests, short hospital stays, and other medical services, there is no out-of-pocket maximum, so a serious illness or extended hospital stay could be financially devastating.

For this reason, beneficiaries often purchase a Medigap policy offered by private insurers, which pays nearly all or a percentage of Medicare out-of-pocket costs, and for some services not covered by Medicare such as emergency medical care outside the United States. In most states, Medigap policies are labeled by letter (for example, Plan A). Benefits for each plan are standardized, but premiums vary by insurance company, location, gender, tobacco use, and marital status.

The best time to buy a Medigap policy is when you first enroll in Medicare Part B. You then have a six-month period during which you can buy any Medigap policy in your state for the same premium the insurance company charges to healthy enrollees, even if you have health problems. If you miss this opportunity, a company can charge you more for coverage or refuse coverage altogether, depending on your health.

Part D prescription drug plans are offered by private insurers under Medicare supervision. Monthly premiums, deductibles, and out-of-pocket costs vary by plan.

Medicare Advantage

Medicare Advantage (MA) is offered by private insurers but mostly funded by Medicare. These “all-in-one” plans are generally more cost-effective than the combined costs of Original Medicare, Medigap, and Part D. All MA plans have out-of-pocket maximums and may offer additional benefits such as dental care and eyeglasses. In return for lower costs, MA plans strongly encourage or require the use of network providers and may deny claims that would be paid by Original Medicare.

Personalized comparisons

The best place to start exploring optional plans is at medicare.gov/plan-compare. After entering your zip code, you will have a choice to find a Medicare Advantage Plan, a Medicare Part D drug plan, or a Medigap policy. If you are already a Medicare beneficiary, you can save time by logging in to your online account, or create a new account. When exploring MA plans, be sure that your preferred providers are included in the plan’s network. Recently, an increasing number of providers have left MA networks due to claim denials and stringent preauthorization requirements.1

Open Enrollment offers the opportunity to change MA plans or return to Original Medicare. Keep in mind, however, that when you change from an MA plan to Original Medicare, you may pay a higher premium for a Medigap policy, or be unable to obtain a policy, depending on your health.

Annual Open Enrollment

Medicare beneficiaries can make the following changes during annual Open Enrollment from October 15 to December 7, with changes effective January 1.

In addition, you can change from MA to Original Medicare or switch MA plans during the Medicare Advantage Open Enrollment Period from January 1 to March 31. You may also be able to make changes during other special enrollment periods.

When exploring Part D drug plans, be sure to accurately enter the name, dosage, and frequency of your prescription drugs. Slight differences, such as a tablet vs. a capsule or generic vs. brand, can make a big difference in the cost of the medication. Note that Medicare Part D out-of-pocket costs will be capped at $2,000 starting in 2025.2

1) KFF Health News, November 29, 2023

2) The Part D cap will be adjusted annually based on the change in Medicare Part D per capita spending (i.e., the amount that Medicare spends on each Part D beneficiary).