EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

The year 2022 may best be described by one word: inflation. The economies of the United States and the world were influenced by rising inflation, its causes, and the policies aimed at curtailing it. While inflationary pressures began to mount in 2021, they were exacerbated by continuing supply shortages; the ongoing effects of the COVID-19 pandemic, both here and abroad; the Russian invasion of Ukraine; and a global energy crisis.

Early in 2022, the Federal Reserve expected inflation to reach 2.6% by the end of the year, not much above their 2.0% target. Federal officials expected supply bottlenecks to ease, economies to re-open after relaxing COVID-related restrictions, and economic activity to return to something close to normal.

Unfortunately, the Fed underestimated how rising wages, federal aid, and expanded savings would lead to increased consumer spending, which continued to outpace supply, and drive prices higher. Most importantly, Fed officials didn’t foresee the impact the Russian invasion of Ukraine would have on world trade in energy, food commodities, and resources such as natural gas and crude oil. And inflation was not just felt in the U.S. but throughout world economies as well. The International Monetary Fund expects worldwide inflation to hit 8.8%, the highest rate since 1996. In response, the Federal Reserve began the most aggressive policy of interest-rate hikes in more than 15 years.

Consumer price indexes in the 19 countries that use the euro currencyrose to 10.0% or higher in November from a year earlier, while prices for food rose at a faster pace. Inflationary pressures also impacted world economies in the Middle East, Africa, South America, Canada, and Mexico. Rising inflation made countries’ imports more expensive and forced central banks to raise interest rates. The U.S. dollar surged in value against most world currencies, weakening foreign currencies and contributing to rising prices for goods and services.

While overall inflationary pressures may have peaked as we close out 2022, food and energy prices remain elevated. Energy prices led the price surge at the beginning of the year. Crude oil prices rose to more than $110.00 per barrel for the first time since 2011. Energy prices, which were already rising at the end of 2021, were sent soaring following the Russian invasion of Ukraine as Russian refining capacity diminished amidst sanctions and trade restrictions imposed by several countries.

However, energy prices have since stabilized somewhat. Helping to stem surging oil prices was a notable retreat in Chinese energy demand amidst COVID-related restrictions; the stabilization of Russian crude output; increased U.S. oil production; and a release of oil from the Strategic Petroleum Reserve.

The U.S. economy saw a slowdown in growth for much of 2022. Gross domestic product contracted in the first two quarters of the year after advancing at an annualized rate of 5.9% in 2021. But GDP rebounded in the third quarter, climbing 3.2%. Although inflation has cut into consumers’ purchasing power, they have continued to spend during difficult economic times, supported by rising wages, job growth, and access to savings accumulated during the pandemic.

Industrial production lagged through the summer months, only to rebound during the latter part of 2022, ultimately exceeding its pace from a year earlier. The housing sector was hit particularly hard by rising mortgage rates and diminished inventory. Existing home sales were more than 35.0% below their pace in 2021, while sales of new single-family homes lagged by more than 15.0%.

Inflation also impacted the stock market, both at home and abroad. Several market sectors that had led the bull surge since 2008 suffered notable pullbacks. Information technology and communication services ended up as two of the worst performing sectors in 2022. Retail stocks also took a tumble as inflation drove up nondiscretionary items like food and energy, leaving less for consumers to spend on discretionary products and services. Also plaguing retailers were rising costs associated with products, services, and labor.

This past year was not only a difficult one for stocks and bonds, but also for “alternative assets” such as crypto. Rising interest rates impacted the viability of crypto. Couple this with revelations of fraud and abuse, and crypto assets have fallen precipitously.

Nevertheless, as 2022 draws to a close, there are some positives to consider entering the new year. The GDP expanded for the first time in the third quarter, and crude oil and gas prices reversed course and dipped lower. Primary inflationary indicators, such as the consumer price index and the personal consumption expenditures price index, trended lower at the end of the year. Ultimately, the economic outlook for 2023 will likely depend on the path of inflation and whether the economies of the U.S. and the world can avoid a recession as prices are driven lower.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Snapshot 2020

The Markets

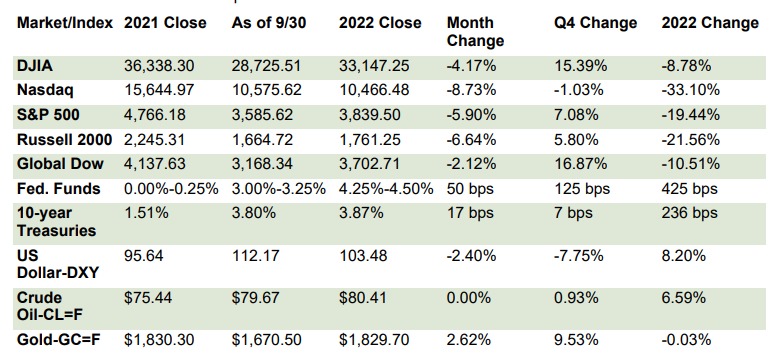

– Equities: Stocks began 2022 on a sour note, ending January and February in the red. Unfortunately, things didn’t get much better for the remainder of the year. Following a bull market that lasted more than 10 years, stocks experienced a sizeable pullback. The benchmark indexes listed here declined in each of the first three quarters of 2022. The Nasdaq lost more than 33.0% on the year, negatively impacted by the Federal Reserve’s aggressive, inflation-fighting policy, which hampered tech and growth stocks. While Wall Street showed some resilience in the fourth quarter, stocks suffered their worst year since the financial crisis of 2008.

– On the last day of the year, each of the benchmark indexes listed here ended the year lower, despite a solid fourth quarter. Among the market sectors, only energy advanced, gaining a robust 59.04%. The remaining market sectors lost value, led by communication services (-40.4%) and followed by consumer discretionary (-37.6%), information technology (-28.9%), real estate (-28.5%), materials (-14.1%), financials (-12.4%), industrials (-7.1%), health care (-3.6%), consumer staples (-3.2%), and utilities (-1.4%).

– Bonds: Historically, when stocks are down investors move to bonds. However, for most investors that paradigm did not hold true in 2022, as both stocks and bonds suffered double-digit losses. The Bloomberg (formerly, Barclays/Lehman) Aggregate Bond Index realized the worst return in its history after declining nearly 13.0%. The yield on 10-year Treasuries rose by more than 230 basis points, as bond prices sank (bond prices and yields move in opposite directions). The U.S. Treasury yield curve (the difference between short-term bond interest rates and long-term rates) has been inverted for much of the year. Currently, the difference between the 3-month bond and the 10-year bond is roughly -0.65%, indicating an inverted yield curve. Historically, an inverted yield curve has often signaled a recession. However, other economic indicators seem to indicate that a full-blown recession is unlikely.

– Oil: Crude oil prices rode a wave of volatility throughout 2022. An energy crisis, rising demand, and the Russian invasion of Ukraine sent prices soaring, hitting a high of more than $122.00 per barrel in early June. However, demand waned, particularly in China, where COVID-related lockdowns stifled requirements for crude oil. Crude oil prices were also driven lower by additional U.S. output, including the release of crude oil from the Strategic Petroleum Reserve. By the end of the year, crude oil prices rose by about 7.0%.

– Prices at the pump climbed higher to begin the year. However, as crude oil prices declined, so did retail gasoline prices. The national average retail price for regular gasoline was $3.281 per gallon to begin 2022. Gas prices steadily increased throughout the first half of the year, reaching a high of $5.006 in June. Gas prices trended lower for the remainder of 2022, closing out the year at $3.091 per gallon for the week ended December 26.

– FOMC/Interest Rates: The target range for the federal funds rate began the year at 0.00%-0.25% and ended 2022 at 4.25%-4.50%, an increase of 425 basis points. Inflation began to climb in 2021, as strong consumer demand collided with pandemic-related supply constraints, which drove prices up, reaching a 39-year high in November 2021. The Fed initially termed the rapid rise in prices “transitory,” expecting that the factors driving inflation upward would subside. However, inflationary pressures did just the opposite for much of 2022, particularly following the Russian invasion of Ukraine in February. In an effort to combat rising inflation, the Fed began hiking the federal funds target range. The first rate hike came in March (25 basis points), followed by four consecutive 75-basis point interest-rate increases. At its last meeting of 2022 in December, the Fed announced a 50-basis point rate hike. Following its last meeting in December, the Fed’s economic projections showed the personal consumption expenditures price to end 2022 at 5.6%, with prices not anticipated to settle at or near the Fed’s target goal of 2.0% until 2025.

– US Dollar-DXY: Since June, the value of the U.S. dollar has been increasing relative to most foreign currencies, particularly the British pound and the Euro. Despite slipping at the end of the year, the dollar remained on track for its biggest annual gain since 2015. In 2022, the dollar has gained about 8.5% against a basket of currencies. The aggressive policy adopted by the Fed to combat rising inflation sent the dollar soaring, reaching a high of about 18.0% in September. The expectation that the Fed will be less hawkish in 2023 has cut into the dollar’s value during the last quarter of 2022.

– Gold: Gold prices began the year at $1,830.30 and closed 2022 at $1,829.70, a decrease of about 0.3%. During the first quarter of 2022, gold prices spiked to $2,053.00 per ounce, following the start of the Russia/Ukraine war. However, by the end of the first quarter, gold prices settled in the $1,930.00 per ounce range. By the third quarter, weakness in the stock market coupled with a surging dollar sent gold prices down to a 30-month low of $1,691.00 per ounce. For the remainder of the year, gold prices hovered between $1,750.00 and $1,800.00 per ounce.

Last Months Economic News

– Employment: Job growth remained strong in November with the addition of 263,000 new jobs after adding 284,000 (revised) new jobs in October. Monthly job growth has averaged 392,000 thus far in 2022, compared with 562,000 per month in 2021. Despite federal interest-rate hikes aimed at slowing the economy and inflation, there is little evidence that the supply of labor is peaking. In November, the unemployment rate was unchanged at 3.7% and has remained in the range of 3.5%-3.7% since March. The number of unemployed persons was essentially unchanged at 6.0 million. Both the unemployment rate and the number of unemployed persons are in line with their levels prior to the coronavirus pandemic (3.5% and 5.7 million, respectively, in February 2020). Among the unemployed, the number of workers who permanently lost their jobs rose by 127,000 to 1.4 million in November (1.9 million in November 2021). The labor force participation rate dipped 0.1 percentage point to 62.1% in November (61.9% a year earlier). The employment-population ratio decreased by 0.1 percentage point to 59.9% in November (59.5% in November 2021). In November, average hourly earnings increased by $0.18 to $32.82. Over the past 12 months ended in November, average hourly earnings rose by 5.1% (average hourly earnings in November 2021 were $31.23). The average workweek decreased by 0.1 hour to 34.4 hours in November, down from 34.8 hours in November 2021.

– There were 225,000 initial claims for unemployment insurance for the week ended December 24, 2022. During the same period, the total number of workers receiving unemployment insurance was 1,710,000. Over the course of the year, initial weekly claims moved up and down, but generally remained within a range of 166,000-261,000. By comparison, there were 211,000 initial claims for unemployment insurance for the week ended December 25, and the total number of claims paid was 1,805,000.

– FOMC/Interest Rates: The Federal Open Market Committee met in December and increased the target range for the federal funds rate 50 basis points to 4.25%-4.50%. In support of its decision, the FOMC noted that inflation levels remain elevated due to supply and demand imbalances related to the pandemic, higher food and energy prices, broader price pressures, and the ongoing Russia/Ukraine war.

– GDP/Budget: The economy, as measured by gross domestic product, accelerated at an annual rate of 3.2% in the third quarter. GDP declined in the first and second quarters, 1.6% and 0.6%, respectively. Consumer spending, as measured by the personal consumption expenditures index, rose 2.3% in the third quarter, marginally higher than in the second quarter (2.0%) and the first quarter (1.3%). Spending on services rose 3.7% in the third quarter compared with a 4.6% increase in the second quarter. Consumer spending on goods actually decreased 0.4% in the third quarter. Fixed investment fell 3.5% in the third quarter (-5.0% in the second quarter), pulled lower by a 27.1% drop in residential fixed investment. Nonresidential (business) fixed investment rose 6.2% in the third quarter. Exports rose 14.6% in the third quarter, compared with a 13.8% increase in the previous quarter. Imports, which are a negative in the calculation of GDP, fell 7.3% in the third quarter, after advancing 2.2% in the second quarter. Consumer prices increased 4.3% in the third quarter (6.5% in the second quarter). Excluding food and energy, consumer prices advanced 4.6% in the third quarter (7.1% in the second quarter).

– November saw the federal budget deficit come in at $248.5 billion, up roughly 30.0% from the November 2021 deficit. The deficit for the first two months of fiscal year 2023, at $336.4, is $20.0 billion lower than the first two months of the previous fiscal year. For fiscal year 2022, which runs through September 2022, the government deficit was $1.4 trillion, which was $1.4 trillion lower than the government deficit for fiscal year 2021. For fiscal year 2022, government outlays declined $550.0 billion, while government receipts increased $850.1 billion. Individual income tax receipts rose by $587.8 billion, and corporate income tax receipts increased by $53.0 million.

– Inflation/Consumer Spending: According to the latest Personal Income and Outlays report, personal income and disposable personal income rose 0.4% in November after increasing 0.7% in October. Consumer spending advanced 0.1% in November after increasing 0.9% the previous month. Consumer prices inched up 0.1% in November after advancing 0.4% in October. Consumer prices have risen 5.5% since November 2021.

– The Consumer Price Index for November may offer more evidence that inflation may be peaking. The CPI rose 0.1% after advancing 0.4% in October. Over the 12 months ended in November, the CPI rose 7.1%, down from 7.7% in October, falling to its lowest 12-month advance since December 2021. Excluding food and energy prices, the CPI rose 0.2% in November and 6.0% for the year ended in November. Although energy prices fell 1.6% in November, food prices rose 0.5% and prices for shelter rose 0.6%. For the 12 months ended in November, energy prices increased 13.1% (despite the recent decrease), while food prices rose 10.6% (food at home prices increased 12.0%). New vehicle prices advanced 7.2%, prices for transportation services rose 14.2%, and prices for shelter increased 7.1%.

– Prices that producers receive for goods and services rose 0.3% in November following a 0.2% October jump. Producer prices increased 7.4% for the 12 months ended in November. Producer prices less foods, energy, and trade services rose 0.3% in November, while prices excluding foods and energy increased 0.4%. In November, prices for services increased 0.4%, while prices for goods inched up 0.1%. For the 12 months ended in November, prices less foods, energy, and trade services moved up 4.9%, while prices less foods and energy increased 6.2%.

– Housing: Sales of existing homes decreased 7.7% in November, marking the tenth consecutive monthly decline. Existing home sales dropped 35.4% from November 2021. The median existing-home price was $370,700 in November, lower than the October price of $378,800 but 3.5% higher than the November 2021 price of $358,200. Unsold inventory of existing homes represents a 3.3-month supply at the current sales pace, unchanged from October but well above the 2.1-month supply in November. Sales of existing single-family homes dropped 7.6% in November and have not recorded an increase since January 2022. Over the 12 months ended in November, sales of existing single-family homes are down 35.2%. The median existing single-family home price was $376,700 in November, down from $384,600 in October but higher than the November 2021 price of $365,000.

– New single-family home sales advanced in November, climbing 5.8% and marking the second consecutive monthly increase. However, sales are down 15.3% from November 2021. The median sales price of new single-family houses sold in November was $421,700 ($484,700 in October). The November average sales price was $543,600 ($533,400 in October). The inventory of new single-family homes for sale in November represented a supply of 8.6 months at the current sales pace, down from the October estimate of 9.3 months.

– Manufacturing: Industrial production declined 0.2% in November, following a 0.1% decrease in October. Manufacturing decreased 0.6% in November, mining fell 0.7%, while utilities rose 3.6%. Over the past 12 months, total industrial production in November was 2.5% above its year-earlier reading. Although manufacturing fell in November, it remained 1.2% above its November 2021 rate.

– November saw new orders for durable goods decrease 2.1%, after increasing in each of the previous three months. Durable goods orders advanced 0.7% in October. New orders for durable goods rose 10.5% since November 2021. Excluding transportation, new orders increased 0.2% in November. Excluding defense, new orders decreased 2.6%. Transportation equipment, down following three consecutive monthly increases, led the November decrease, falling 6.3%.

– Imports and exports: Both import and export prices declined in November. Import prices fell 0.6% after decreasing 0.4% in the prior month. Prices for imports have not increased since June 2022. Import prices declined 4.6% from June to November, after rising 8.1% in the first half of 2022. Despite the recent decreases, prices for U.S. imports rose 2.7% over the past year, the smallest 12-month advance since January 2021. Prices for import fuel fell 2.8% in November following a decline of 2.7% in October. Import fuel prices have not recorded a monthly increase since a 5.6% advance in June 2022. Export prices declined 0.3% in November and have not recorded a 1-month increase since rising 1.1% in June 2022. Prices for exports advanced 6.3% from November 2021 to November 2022, the smallest 12-month increase since February 2021.

– The international trade in goods deficit was $83.3 billion in November, down $15.5 billion, or 15.6%, from October. Exports of goods were $168.9 billion in November, $5.3 billion less than in October. Imports of goods were $252.2 billion in November, $20.8 billion less than in October. The November drop in exports was widespread, with only automotive vehicles and consumer goods increasing. Each category of imports decreased, led by consumer goods (-13.0%), automotive vehicles (-8.9%), and industrial supplies (-6.0%).

– The latest information on international trade in goods and services, released December 6, is for October and shows that the goods and services trade deficit was $78.2 billion, an increase of $4.0 billion from the September deficit. October exports were $256.6 billion, 0.7%, less than September exports. October imports were $334.8 billion, 0.6%, more than September imports. Year to date, the goods and services deficit increased $136.9 billion, or 19.1%, from the same period in 2021. Exports increased $415.3 billion, or 19.8%. Imports increased $552.2 billion, or 19.8%.

– International markets: The impact of inflation was felt throughout much of the world. Most countries saw double-digit increases in prices for goods and services during the year. In 2022, the consumer price index advanced 10.0% in Germany, 10.7% in the United Kingdom, 10.1% in the Eurozone, and 6.8% in Canada. Japan (3.8%) and China (1.6%) were not significantly impacted by rising inflation. However, gross domestic product in both Japan (-0.8%) and China (2.8% through the third quarter) retreated from the prior year. Stock markets of several countries were also hit hard. For 2022, the STOXX Europe 600 Index declined 12.4%; the United Kingdom’s FTSE advanced 0.9%; Japan’s Nikkei 225 Index fell 9.4%; and China’s Shanghai Composite Index lost 15.1%.

– Consumer confidence: The Conference Board Consumer Confidence Index® increased in December following two consecutive monthly declines. The index stands at 108.3, up from 101.4 in November. The Present Situation Index, based on consumers’ assessment of current business and labor market conditions, rose to 147.2 in December, up from 138.3 in the previous month. The Expectations Index — based on consumers’ short-term outlook for income, business, and labor market conditions — improved to 82.4 in December from 76.7 in November.

Eye on the Year Ahead

The battle against rising inflation will likely continue to dominate much of the economy and stock market in 2023. If and when the Federal Reserve scales back its aggressive interest-rate hikes, investors might be more inclined to return to equities, particularly tech shares. However, the war in Ukraine and new COVID cases will also have an impact. If nothing else, 2023 should be very interesting.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indexes listed are unmanaged and are not available for direct investment.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Triad Advisors, LLC, Member FINRA/SIPC. Financial Planning, Wealth Management and Tax Services offered through EagleStone Tax & Wealth. Triad and EagleStone are not affiliated entities.

Financial Planning, Investment & Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax & Accounting services provided through EagleStone Tax & Accounting Services.