EagleStone Wealth Advisors, Inc. is in the process of withdrawing its registration with the SEC and is no longer taking on any new clients. EagleStone Tax & Wealth Advisors has merged with Onyx Bridge Wealth Group, Onyx Bridge Tax Group, and Onyx Bridge Retirement Group, respectively. You will be redirected to their site in the next 5 seconds.

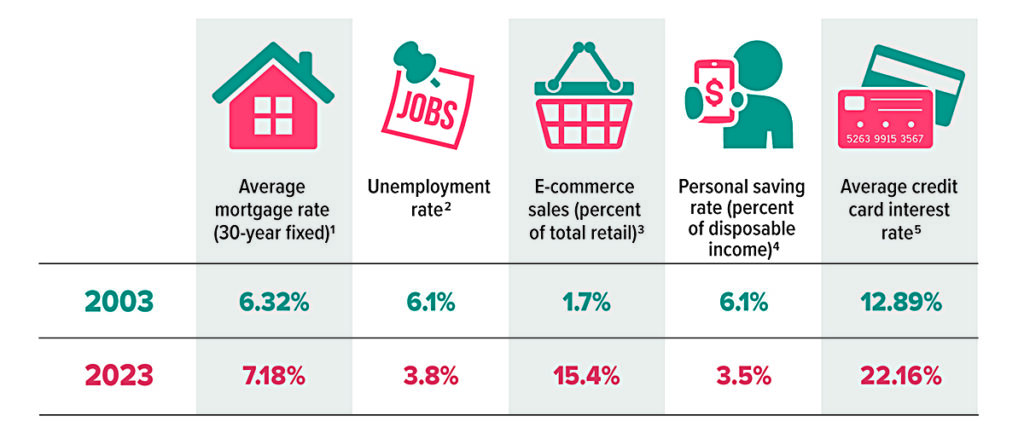

Then and Now

In 2003, the U.S. was emerging from the dot-com recession, unemployment rates were peaking during a jobless recovery, and online shopping was becoming more popular. Twenty years have passed, and here’s how some things have changed — one pandemic and two recessions later.

Source: 1) Freddie Mac, 2023 (August); 2) U.S. Bureau of Labor Statistics, 2023 (August); 3) U.S. Census Bureau, 2023 (Q2); 4) U.S. Bureau of Economic Analysis, 2023 (July); 5) Federal Reserve Board, 2023 (Q2)

Year-End 2023 Tax Tips

Here are some things to consider as you weigh potential tax moves before the end of the year.

Set Aside Time to Plan

Effective planning requires that you have a good understanding of your current tax situation, as well as a reasonable estimate of how your circumstances might change next year. There’s a real opportunity for tax savings if you’ll be paying taxes at a lower rate in one year than in the other. However, the window for most tax-saving moves closes on December 31, so don’t procrastinate.

Defer Income to Next Year

Consider opportunities to defer income to 2024, particularly if you think you may be in a lower tax bracket then. For example, you may be able to defer a year-end bonus or delay the collection of business debts, rents, and payments for services in order to postpone payment of tax on the income until next year.

Accelerate Deductions

Look for opportunities to accelerate deductions into the current tax year. If you itemize deductions, making payments for deductible expenses such as qualifying interest, state taxes, and medical expenses before the end of the year (instead of paying them in early 2024) could make a difference on your 2023 return.

Make Deductible Charitable Contributions

If you itemize deductions on your federal income tax return, you can generally deduct charitable contributions, but the deduction is limited to 50% (currently increased to 60% for cash contributions to public charities), 30%, or 20% of your adjusted gross income, depending on the type of property you give and the type of organization to which you contribute. (Excess amounts can be carried over for up to five years.)

Increase Withholding

If it looks as though you’re going to owe federal income tax for the year, consider increasing your withholding on Form W-4 for the remainder of the year to cover the shortfall. The biggest advantage in doing so is that withholding is considered as having been paid evenly throughout the year instead of when the dollars are actually taken from your paycheck.

More to Consider

Here are some other things to consider as part of your year-end tax review.

Save More for Retirement

Deductible contributions to a traditional IRA and pre-tax contributions to an employer-sponsored retirement plan such as a 401(k) can help reduce your 2023 taxable income. If you haven’t already contributed up to the maximum amount allowed, consider doing so. For 2023, you can contribute up to $22,500 to a 401(k) plan ($30,000 if you’re age 50 or older) and up to $6,500 to traditional and Roth IRAs combined ($7,500 if you’re age 50 or older). The window to make 2023 contributions to an employer plan generally closes at the end of the year, while you have until April 15, 2024, to make 2023 IRA contributions. (Roth contributions are not deductible, but qualified Roth distributions are not taxable.)

Take Any Required Distributions

If you are age 73 or older, you generally must take required minimum distributions (RMDs) from your traditional IRAs and employer-sponsored retirement plans (an exception may apply if you’re still working for the employer sponsoring the plan). Take any distributions by the date required — the end of the year for most individuals. The penalty for failing to do so is substantial: 25% of any amount that you failed to distribute as required (10% if corrected in a timely manner). Beneficiaries are generally required to take annual distributions from inherited retirement accounts (and under certain circumstances, a distribution of the entire account 10 years after certain events, such as the death of the IRA owner or the beneficiary); there are special rules for spouses.

Weigh Year-End Investment Moves

Though you shouldn’t let tax considerations drive your investment decisions, it’s worth considering the tax implications of any year-end investment moves. For example, if you have realized net capital gains from selling securities at a profit, you might avoid being taxed on some or all of those gains by selling losing positions. Any losses above the amount of your gains can be used to offset up to $3,000 of ordinary income ($1,500 if your filing status is married filing separately) or carried forward to reduce your taxes in future years.

Much Ado About RMDs

The SECURE 2.0 Act, passed in late 2022, included numerous provisions affecting retirement savings plans, including some that impact required minimum distributions (RMDs). Here is a summary of several important changes, as well as a quick primer on how to calculate RMDs.

What Are RMDs?

Retirement savings accounts are a great way to grow your nest egg while deferring taxes. However, Uncle Sam generally won’t let you avoid taxes indefinitely. RMDs are amounts that the federal government requires you to withdraw annually from most retirement accounts after you reach a certain age. Currently, RMDs are required from traditional IRAs, SEP and SIMPLE IRAs, and work-based plans such as 401(k), 403(b), and 457(b) accounts.

If you’re still working when you reach RMD age, you may be able to delay RMDs from your current employer’s plan until after you retire (as long as you don’t own more than 5% of the company); however, you must still take RMDs from other applicable accounts.

While you can always withdraw more than the required minimum, if you withdraw less, you’ll be subject to a federal penalty.

Four Key Changes

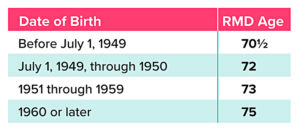

1. Perhaps the most notable change resulting from the SECURE 2.0 Act is the age at which RMDs must begin. Prior to 2020, the RMD age was 70½. After passage of the first SECURE Act in 2019, the age rose to 72 for those reaching age 70½ after December 31, 2019. Beginning in 2023, SECURE 2.0 raised the age to 73 for those reaching age 72 after December 31, 2022, and, in 2033, to 75 for those who reach age 73 after December 31, 2032.

2. A second important change is the penalty for taking less than the total RMD amount in any given year. Prior to passage of SECURE 2.0, the penalty was 50% of the difference between the amount that should have been distributed and the amount actually withdrawn. The tax is now 25% of the difference and may be reduced further to 10% if the mistake is corrected in a timely manner (as defined by the IRS).

3. A primary benefit of Roth IRAs is that account owners (and typically their spouses) are not required to take RMDs from those accounts during their lifetimes, which can enhance estate-planning strategies. A provision in SECURE 2.0 brings work-based Roth accounts in line with Roth IRAs. Beginning in 2024, employer-sponsored Roth 401(k) accounts will no longer be subject to RMDs during the original account owner’s lifetime. (Beneficiaries, however, must generally take RMDs after inheriting accounts.)

4. Similarly, a provision in SECURE 2.0 ensures that surviving spouses who are sole beneficiaries of a work-based account are treated the same as their IRA counterparts beginning in 2024. Specifically, surviving spouses who are sole beneficiaries and inherit a work-based account will be able to treat the account as their own. Spouses will then be able to use the favorable uniform lifetime table, rather than the single life table, to calculate RMDs. Spouses will also be able to delay taking distributions until they reach their RMD age or until the account owner would have reached RMD age.

How to Calculate RMDs

RMDs are calculated by dividing your account balance by a life expectancy factor specified in IRS tables (see IRS Publication 590-B). Generally, you would use the account balance as of the previous December 31 to determine the current year’s RMD.

For example, say you reach age 73 in 2024 and have $300,000 in a traditional IRA on December 31, 2023. Using the IRS’s Uniform Lifetime Table, your RMD for 2024 would be $11,321 ($300,000 ÷ 26.5).

The IRS allows you to delay your first RMD until April 1 of the year following the year in which it is required. So in the above example, you would be able to delay the $11,321 distribution until as late as April 1, 2025. However, you will not be allowed to delay your second RMD beyond December 31 of that same year — which means you would have to take two RMDs in 2025. This could have significant implications for your income tax obligation, so beware.

An RMD is calculated separately for each IRA you have; however, you can withdraw the total from any one or more IRAs. Similar rules apply to 403(b) accounts. With other work-based plans, an RMD is calculated for and paid from each plan separately.

For more information about RMDs, contact your tax or financial professional. There is no assurance that working with a financial professional will improve investment results.

Enriching a Teen with a Roth IRA

Teenagers with part-time or seasonal jobs earn some spending money while gaining valuable work experience. They also have the chance to contribute to a Roth IRA — a tax-advantaged account that can be used to save for retirement or other financial goals.

Minors can contribute to a Roth IRA provided they have earned income and a parent (or other adult) opens a custodial account in the child’s name. Contributions to a Roth IRA are made on an after-tax basis, which means they can be withdrawn at any time, for any reason, free of taxes and penalties. Earnings grow tax-free, although nonqualified withdrawals of earnings are generally taxed as ordinary income and may incur a 10% early-withdrawal penalty, unless an exception applies.

A withdrawal of earnings is considered qualified if the account is held for at least five years and the distribution is made after age 59½. However, there are two penalty exceptions that may be of special interest to young savers. Penalty-free early withdrawals can be used to pay for qualified higher-education expenses or to purchase a first home, up to a $10,000 lifetime limit. (Ordinary income taxes will apply.)

Flexible College Fund

A Roth IRA may have some advantages over savings accounts and dedicated college savings plans. Colleges determine need-based financial aid based on the “expected family contribution” (EFC) calculated in the Free Application for Federal Student Aid (FAFSA).

Most assets belonging to parents and the student count toward the EFC, but retirement accounts, including a Roth IRA, do not. Thus, savings in a Roth IRA should not affect the amount of aid your student receives. (Withdrawals from a Roth IRA and other retirement plans do count toward income for financial aid purposes.)

Financial Head Start

Opening a Roth IRA for a child offers the opportunity to teach fundamental financial concepts, such as different types of investments, the importance of saving for the future, and the power of compounding over time. You might encourage your children to set aside a certain percentage of their paychecks, or offer to match their contributions, as an incentive.

In 2023, the Roth IRA contribution limit for those under age 50 is the lesser of $6,500 or 100% of earned income. In other words, if a teenager earns $1,500 this year, his or her annual contribution limit would be $1,500. Parents and other individuals may also contribute directly to a teen’s Roth IRA, subject to the same limits.

IRS Circular 230 disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any tax advice contained in this communication (including any attachments) was not intended or written to be used, and cannot be used, for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any matter addressed herein.

Securities offered through Emerson Equity LLC. Member FINRA/SIPC. Advisory Services offered through EagleStone Tax & Wealth Advisors. EagleStone Tax & Wealth Advisors is not affiliated with Emerson Equity LLC. Financial Planning, Investment and Wealth Management services provided through EagleStone Wealth Advisors, Inc. Tax and Accounting services provided through EagleStone Tax & Accounting Services.

For more information on Emerson Equity, visit FINRA’s BrokerCheck website or download a copy of Emerson Equity’s Customer Relationship Summary.